Fed Survey Finds Most Consumers Are Happy With Their Finances, Despite Lack Of Retirement Savings

As the economy continues to bounce back from the Great Recession, consumers have adopted a more optimistic outlook when it comes to their finances despite the fact that a third of the country has no savings put away for the future, according to a new survey from the Federal Reserve.

The 2014 Survey of Household Economics and Decisionmaking [PDF] points out that over the past year individuals and families have experienced mild improvements in their overall well-being, leading to an increase in optimism for the long-term.

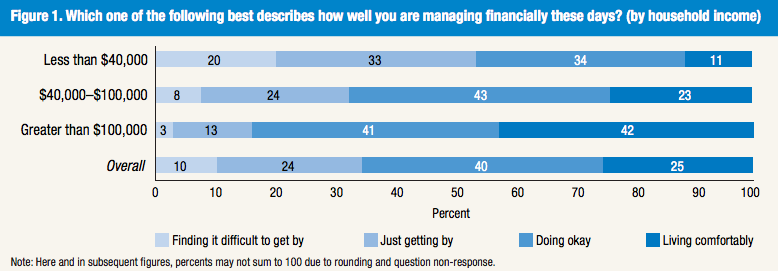

Over the past year, consumers’ feeling about their financial situation has improved.

According to the report, which surveyed 5,800 respondents in October 2014, a majority of Americans – about 65% – are either “doing okay” or “living comfortably” financially, representing a 3% increase from 2013.

The warm and fuzzy feelings continued when respondents were asked about their future income prospects.

Twenty-nine percent of Americans expect their income to be higher this year, up from 21% who expected an uptick in wages in 2013.

As with most surveys on finances, respondents’ views varied depending on their current economic situation.

Nearly 22% of American with less than $40,000 in annual income believe their salary will increase in the next year, while 36% of those with annual incomes of more than $100,000 expect the same situation.

It appears that most Americans aren’t afraid to work for those income increases. Forty-nine percent of part-time workers and 36% of all workers say they prefer to work more hours if they could.

Despite consumers’ rosy feelings about their current financial situation, the Fed survey found those emotion may be fleeting, as Americans aren’t truly prepared for the future.

Consumers have a variety of plans for their retirement.

About 39% of non-retirees have given little or no thought to financial planning for retirement, while 31% have no retirement savings or pension.

Nearly a quarter of those with no retirement savings are older than 45 years of age.

“Even among individuals who are saving, fewer than half of adults with self-directed retirement savings are mostly or very confident in their ability to make the right investment decisions when managing their retirement savings,” the Fed reports.

More than half of the non-retirees that do have retirement accounts are either “not confident” or only “slightly confident” in their ability to make the right investment decisions when investing their funds.

Additionally, 45% of non-retirees who plan to retire expect to keep working in some capacity during retirement to cover expenses.

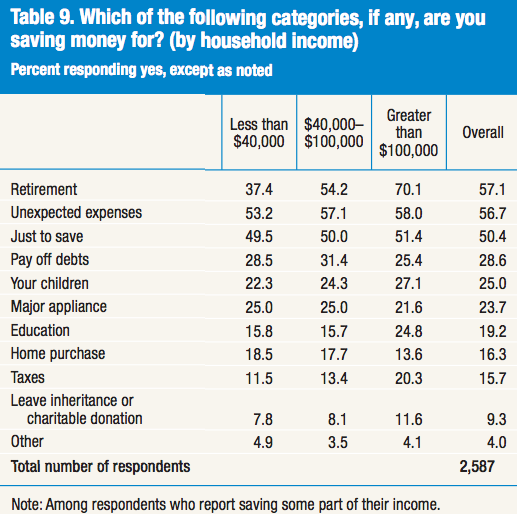

When it comes to income levels and savings, the survey found a stark difference in their habits.

When it comes to current savings habits, lower income consumers are saving for unexpected expenses not retirement.

Respondents with household income under $40,000 are most likely saving for unexpected expenses, while those with annual income of more than $100,000 are more likely to be saving for retirement.

The survey also uncovered other potentially unsettling financial issues for consumers including the fact that only 53% of respondents believe they could cover a hypothetical emergency costing $400 without selling something or borrowing money.

Another 31% of consumers have gone without some type of medical care in the past year because it was unaffordable, while a third of respondents who applied for credit in the last year have been turned down or received less then they requested.

According to the Fed, while most individuals appear to feel financially stable, the results of the survey point out that many segments of the population continue to struggle.

“These consumers remain vulnerable to economic hardships in the case of further financial disruption or are at risk of economic hardship in the future due to an inability to save for future needs such as retirement,” the report states. “The survey results highlight the need to continue to monitor these vulnerable populations and assess the extent to which they are, or are not, benefiting from broader economic recovery.”

Survey of Household Economics and Decisionmaking [Federal Reserve]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.