Student Loan Default Rates Decline, But A Record Number Of Borrowers Are In Default Image courtesy of (D. Michelson)

While the number of borrowers defaulting on their federal student loans didn’t increase this year, the number of consumers who remain in default hasn’t really change either, creating a stand-still of sorts.

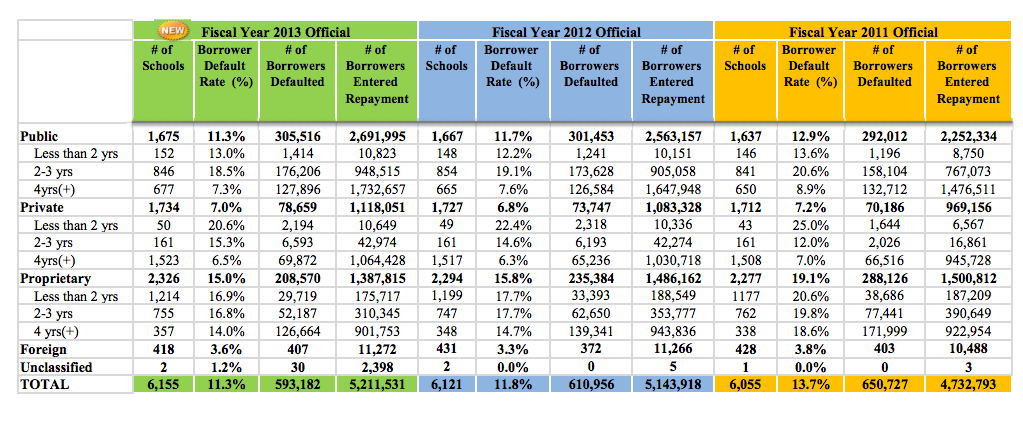

A new report from the Department of Education found that for the third consecutive year, there was a drop in the percentage of borrowers who are defaulting on their student loans within three years of entering repayment. This is known as the cohort default rate.

According to the report, among the 5.2 million borrowers who entered repayment in 2013, 11.3% (or 593,182) had defaulted on their loans by 2015.

That figure is down slightly from the 11.8% of borrowers who entered repayment in 2012 and subsequently defaulted in 2014. In 2013, 13.7% of borrowers who began repaying their debts in 2011 had defaulted.

In all, the default rate dropped for two of the main college sectors. The default rate was 11.3% for students at public schools; 15% for students at for-profit colleges. Conversely, defaults actually increased slightly at private institutions, with 7% of student defaulting on their 2013 loans. Previously, the rate for private schools was 6.8%.

While the continued decrease in defaults is likely good news for borrowers and the government, there’s also some not so stellar news in the report: there are a record 8.1 million borrowers currently in default, according to The Institute for College Access & Success.

“It’s great that recent borrowers are entering default at a slower rate,” Lauren Asher, president of The Institute for College Access & Success (TICAS). “Yet the escalating number of people in default demonstrates that more must be done to help students avoid and get out of default.”

While the Dept. of Education offers repayment plans to assist students in making monthly payments, it also has in place rules that would penalize schools that graduate students unable to meet their debt obligations.

The Dept. of Education uses the cohort default to determine a school’s eligibility to receive federal financial aid funds. If a school’s CDR is too high, then students of that school are not allowed to participate in the programs.

Any school with a default rate of 30% or more for three consecutive years, or a 40% rate for one year, faces the loss of access to those federal programs.

This year, the Department identified 10 schools that had default rates high enough to lose eligibility for federal aid programs. Of those schools, nine were from the for-profit sector. Each school will have an opportunity to appeal the loss of funds.

Affected schools are:

• Cr’u Institute of Cosmetology and Barbering in Garden Grove, CA

• Capstone College in Pasadena, CA

• Florida Barber Academy in Plantation, FL

• Total Look School of Cosmetology and Massage Therapy in Cresco, IA

• Larry’s Barber College in Chicago

• Crescent City School of Gaming & Bartending in New Orleans

• Aaron’s Academy of Beauty in Waldorf, MD

• United Tribes Technical College in Bismarck, ND

• New Life Business Institute in Jamaica, NY

• Jay’s Technical Institute in Houston, TX

These schools, of course, do not represent the entire 8.1 millions student currently in default, but TICAS suggests that many of those borrowers have attended for-profit schools that are either in operation or have recently closed.

“While the Department does not release school-level default rates for closed schools, the 8.1 million borrowers currently in default include students who attended schools that have now closed,” TICAS said in a statement. “Many of the schools that closed recently, such as Corinthian-owned Everest, Wyotech, and Heald College campuses and Marinello Schools of Beauty, are known to have committed widespread fraud, putting their former students at greater risk of default.”

TICAS, along with The Association of Community College Trustees – which reported a decrease in default rates among community colleges — called on the Dept. of Education to increase transparency and accountability for loan servicing as a way to better provide relief for burgeoned student loan borrowers.

“The reality is that default penalizes not only students, but our communities,” J. Noah Brown, president and CEO of ACCT, said in a statement. “It is incumbent upon the Education Department to likewise make adjustments to existing policies so that students who do falter won’t continue to suffer undue consequences.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.