Not Everyone Has $100,000 In Student Loan Debt, But That Doesn’t Mean There’s Not A Problem Image courtesy of Larry Troy

Horror stories about student loan debt have dominated the headlines in recent years. Many feature consumers with hefty loan tabs of more than $100,000, however, those experiences aren’t necessarily representative of the student loan landscape as a whole. But, just because you’re not bleeding to death, doesn’t mean you’re not bleeding. And just because most borrowers have $10,000 or less in debt doesn’t mean they aren’t hurting.

A new report by the Brookings Institute [PDF] finds that what is often viewed as a looming student loan debt crisis, isn’t much more than a scrape on the knee and that the stories of students with six-digit debts are a minority in the grand scheme of things.

But that might not be a fair assumption given the selective data set used to reach these conclusions and the omission of several factors influencing the current student debt outlook including default and dropout rates for students.

The authors examined households of consumers — aged 20 to 40 — to track how the education debt levels and incomes of young households evolved between 1989 and 2010 by using data from Federal Reserve’s Survey of Consumer Finances.

There are always limitations to drawing conclusions from surveyed data, but this particular study is hampered by some of its own self-imposed restrictions.

First, is the fact that the most recent data in the study is four years old. Students entering college this fall were barely in high school when the data was collected. And the student debt landscape has a way of changing rather quickly, meaning their experience could be drastically different from students who graduated just five years ago.

So, essentially the report is cluing us in to what the student loan debt environment looked like back in 2010, not necessarily how it looks today or what it will look like next year.

Additionally, the age range considered in the story, 20 to 40, represents groups of consumers that are likely in very different placed in their lives. The income and debt load of a 22-year-old recent college graduate living at home or with roommates is likely very different than that of a 28-year-old with a steady job and perhaps a family, and incredibly different from a 39-year-old with an established career and an eye toward middle age.

“The data are a snapshot of consumers that may have been paying off their debt for a while,” Lauren Asher, president of The Institute for College Access & Success tells Consumerist. “It is not fully reflecting the growing share of Americans with loans.”

The sum of the report is only equal to its parts, and unfortunately the Brookings report is missing several crucial pieces. Even the study’s touted “noteworthy” findings don’t take into consideration the most current issues plaguing borrowers.

For instance, the report found that monthly payment burdens faced by student loan borrowers has stayed about the same or decreased between 1989 and 2010:

“The average repayment term for student loans increased over this period, allowing borrowers to shoulder increased debt loads without larger monthly payments.”

The report notes that in 1992 the mean term of repayment was 7.5 years, which increased to 13.4 years in 2010.

While having an additional five years to repay a loan may take some pressure off borrowers, the report fails to consider the long-term cost of lengthier repayment periods.

“There’s a significant increased cost to borrowers in both how much debt they are needing to take on and what it costs to pay it off over a longer period of time,” Asher explains.

Every student loan comes with an interest rate – whether that rate is fixed or variable depends on a borrower’s contract with their lender. However, if a borrower has more time to pay their loan back, that interest rate doesn’t just disappear, it will continue to be tacked on to the bill each month. And eventually that 4% interest rate turns into thousands of dollars more being spent.

In another “noteworthy” finding the authors attribute one-quarter of the increase in student debt since 1989 to more Americans obtaining education, specifically graduate degrees. The report briefly recognized that increases in tuition contribute to more debt, as well:

“The share of households with no college experience fell from 41% to 31%, the share with at least one person with a bachelor’s degree increased from 20% to 24%, and the share with at least one person with a graduate degree increased from 9% to 13%.”

Because attending graduate school increases overall tuition costs and means more time in class and less time working, it’s fair to assume that taking on more schooling would mean taking on more debt.

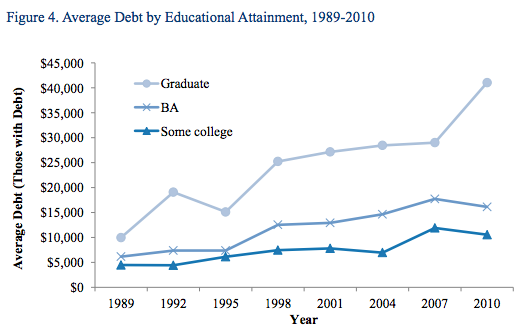

As a result, the average debt levels of borrowers with a graduate degree more than quadrupled, from just under $10,000 to more than $40,000. By comparison, the report found that debt loads of those with only a bachelor’s degree increased by a smaller margin, from $6,000 to $16,000.

However, there is no way to guarantee obtaining a graduate degree will translate into more income in the future. In fact, someone who obtains a degree in a niche field may have to take on a low-paying job while he waits for a rare opening in his particular career path.

This finding can be loosely tied to the author’s final “noteworthy” conclusion that increases in earning over the past two decades have kept pace with increases in total debt; meaning that paying back debt shouldn’t be an issue for most graduates:

“Between 1992 and 2010, the average household with student debt saw an increase of about $7,400 in annual income and $18,000 in total debt. In other words, the increase in earnings received over the course of 2.4 years would pay for the increase in debt incurred.”

While a consumer could probably take the increase in earnings to pay down their debt, the Brookings report doesn’t take into account a borrower’s other debt obligations. And as a Pew Research report earlier this spring found, college graduates with student loan debt are more likely to carry other debt from mortgages, credit cards and car loans.

The report’s findings on the longterm value of college degrees is in line with most recent research on the importance of obtaining higher education, but it is also in contrast to reports that income has not increased for some time.

An Economic Policy Institute study in 2012 found the average inflation-adjured wage for male college graduates declined 11% in the last 10 years; for females the decrease was slightly smaller at 7.6%.

“Although it’s true that lifetime earnings still go up with a college education, we still need to take a look at the larger impacts of system where 7 out of every 10 students graduates with student debt,” Suzanne Martindale, staff attorney for Consumers Union says. “The job market is still tough for younger graduates, and household formation among consumers under 30 has stalled.”

And it’s a different story altogether for students who attended college but left before obtaining a degree. The Brookings report does little to address this issue, but we know that those students are more likely to default on their loans.

“Other data sources have shown that it’s not necessarily how much you owe, but the kinds of loans you have and your financial circumstances that determine how you can pay off,” Asher says. “Borrowers who don’t complete college are in tougher situations than those that do complete overall. Even a small amount of debt can be burdensome.”

The Brookings report authors conclude that typical borrowers, those with $10,000 or less in student loan debt, are no worse off than they were a generation ago.

All of which could very well be true. However, just because the authors paint a rosy picture saying the student loan debt issues aren’t as bad as we’ve been led to believe, doesn’t mean it’s not bad or that the landscape of student loan debt in 2014 is any less devastating to borrowers.

“You can slice and dice the numbers in different ways,” says Martindale, “but there does seem to be some agreement on the following: college costs are going up; average household incomes are relatively flat compared with the previous decade; and more students and families are borrowing loans to pay for college.”

Is a Student Loan Crisis on the Horizon? [Brookings Institute]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.