71% Of Recent College Grads Owe Average Of $29K In Student Loans, Are Scared Pantsless About Paying It Off

(afagen)

According to the new study [PDF] by the Project on Student Debt at The Institute for College Access & Success, the graduating class of 2012 has a higher percentage of graduates leaving school with debt hanging on their backs, 71%, up from 68% in 2008. And during that same time period, the average amount of debt has increased an average of 6% per year, now standing at $29,400.

Recent college grads currently face relatively high levels of unemployment or underemployment, with 18.3% of young college graduates claiming to be unemployed, working fewer hours than they wanted, or that they had given up looking for a job. That said, the odds of finding employment are still higher for those with a college degree than for those with only a high school diploma.

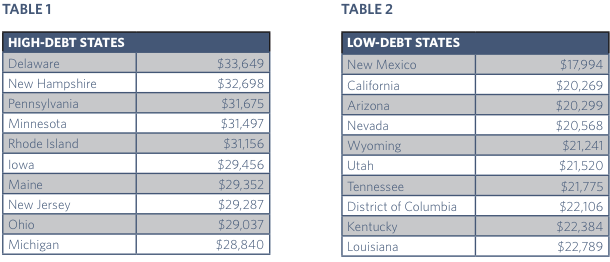

STATES WITH HIGHEST AND LOWEST LEVELS OF DEBT

According to the survey, students graduating from colleges in Delaware had the highest average debt in 2012, at $33,649. In fact, six of the ten states with the highest average student loan debt amounts were in the Mid-Atlantic and Northeast, while the remaining four are Midwestern and Great Lakes states.

On the other side of the rainbow and country is New Mexico, with the lowest average debt amount ($17,994). Again, there is some geographic clustering with Southwestern and Rocky Mountain states accounting for about half of the states on this second list. Washington, D.C., with its average debt of $22,106, is the only East Coast representative on the lower end of the debt scale.

In terms of which states have the highest percentage of graduates with student loan debt, South Dakota tops the list at 78%, followed by New Hampshire (74%), Iowa (71%), and Pennsylvania (70%).

VARIATIONS FROM SCHOOL TO SCHOOL

While the state-to-state averages cover a pretty wide spread of $18K to $34K, the school-to-school comparisons are even more stark, ranging from averages of around $4,500 to nearly $50,000.

And though there is often some correlation between a school’s cost and the average amount of student debt, there are plenty of examples where that isn’t the case.

For example, Princeton University makes the list of low-debt schools because, in spite of the total annual cost of $53,934 to 2012 graduates, the average student loan debt held by the Ivy League school’s graduates was only $5,096. Of course, only about 24% of Princeton graduates took out student loans, as the school tends to attract both those who can afford to pay the steep tuition and those whose academic work earns them grants and scholarships.

Meanwhile, not far away at Rowan University, 34% of the graduates are leaving with an average of $35,027 in student loan debt at a school where the total annual cost to attend is half that of Princeton’s ($26,071).

TICAS has this pretty awesome interactive map that not only shows info for each state, but more granular information about costs and student loan debt averages for all the schools that reported this information in 2012.

THE LOOMING TERROR OF STUDENT LOAN DEBT

Up at Harvard, where 1-in-4 grads leaves with an average of $13,098 in student loan debt, the school’s Institute of Politics has released the results of a new survey showing the mood of “millennials” that vaguely defined group of people between 18-29 that older folks tend to blame all the world’s ills on, what with their texting and rock music.

Among the questions posed by the IOP were a few about student loan debt, and the answers show that young whippersnappers are worried about this problem, regardless of their political affiliation.

First, 42% of respondents said they, or someone in their household, currently has student loan debt, and that 58% of college graduates responding to the survey said they still had debt to pay off.

More importantly, 78% of respondents said the issue of student loan debt is a problem for young people with 57% declaring it a “major” problem.

70% of millennials also say that their ability to pay for school was an important factor in choosing whether or not to attend college. This number is significantly higher (87%) for those in community colleges or 2-year programs.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.