Everything You Need To Know About Personal Finance Fits Onto 5 Business Cards

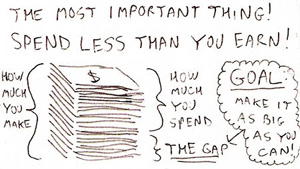

Trent has fit everything you ever needed to know about managing personal finance onto the backs of five business cards. Really! That’s it!

Everything You Ever Really Needed to Know About Personal Finance on the Back of Five Business Cards [The Simple Dollar]

Follow Ben’s posts by RSS.

Follow Ben on Twitter.

Email this reporter: ben@consumerist.com

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.