Banks Luring You Into Signing Back Up For High Overdraft Fees

Banks are mad they can’t just automatically charge you a $35 overdraft anymore if you happen to try to buy a candy bar without enough cash in your account. Newly enacted legislation says they have to get you to opt-in to such overdraft programs. So, what they’re doing is renaming the overdraft programs something else, making them sound awesome, and then blitzing your mailbox and inbox with up-sells. Some banks are even calling people up!

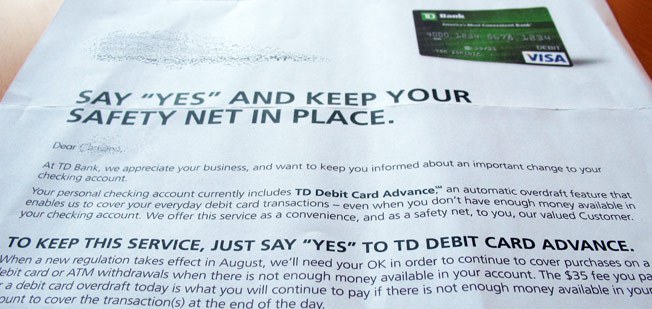

“Debit Card Advance” is what TD Bank is calling the favor of charging you $35 for an over-drafted can of soda.

“Debit Card Advance” is what TD Bank is calling the favor of charging you $35 for an over-drafted can of soda.

“We offer this service as a convenience, and as a safety net, to you, our valued customer,” reads the letter.

The bank sent out new debit cards to customers and said that if they wanted to keep this “service” that they needed to call in or visit a bank.

“Respond today! You’ll lose this important feature on your personal checking account if we don’t hear from you before August 14, 2010.”

For some mysterious reason, these new TD Bank debit cards are also totally flat with no raised numbers. Maybe now that they’ve lost some of their bullshit fee streams they can’t afford raised numbers anymore?

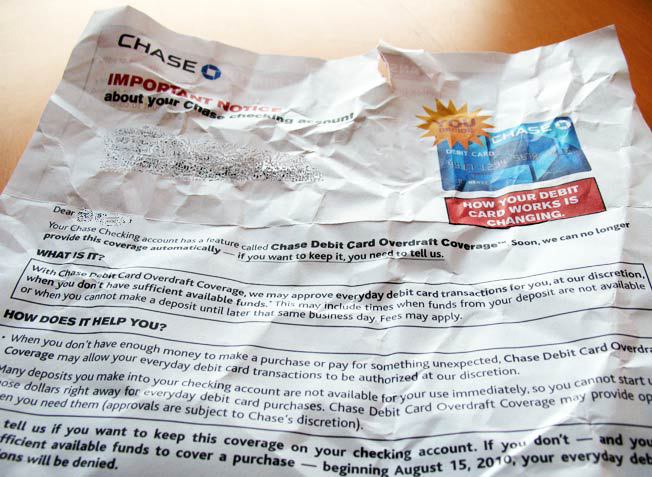

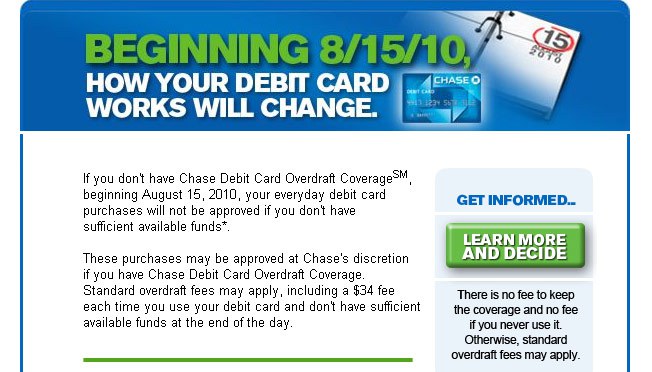

Instead of couching it like some kind of cool exclusive program, Chase has taken an “empowered consumer” approach.

Instead of couching it like some kind of cool exclusive program, Chase has taken an “empowered consumer” approach.

“YOU DECIDE,” yells the starburst. “Is Chase Debit Card Overdraft Coverage (sm) right for you? Our bankers can help you make an informed decision.”

The letter and flyer encourage customers to call the bank, visit the bank, or read the banks’ website to learn about the coverage program. So that you understand its monumental importance, the letter makes liberal use of bolding, underlining, and capital letters.

It reeks of desperation.

“It seems like they are trying to trick clients into thinking that there is a serious problem unless they get the chase overdraft protection,” writes Consumerist reader Cody after getting an email from Chase. “Just the way they word the email isn’t right as they are trying to up-sell that we need to purchase this protection that will inevitably cause more harm than good.”

“It seems like they are trying to trick clients into thinking that there is a serious problem unless they get the chase overdraft protection,” writes Consumerist reader Cody after getting an email from Chase. “Just the way they word the email isn’t right as they are trying to up-sell that we need to purchase this protection that will inevitably cause more harm than good.”

Commenter evnmorlo says that every time they go to their bank’s website, “they force a pop-up to try to get you to sign up for the $35 overdraft fee.” Annath says that he’s seen signs saying “Have YOU opted in yet?” “As though it’s something everyone NEEDS to do,” he writes.

Helix Queen says that her bank called her up and tried to pitch it as a “perk.” However, she has a friend who actually likes overdraft protection. Talking to her recently, Helix Queen’s friend, “got sooo defensive, even expressing her gratitude to the bank for letting her know about having to opt-in… She said something like “They’re always looking out for me.” She couldn’t wait to opt-in…and seemed pissed at the government for taking automatic ODP away.”

They didn’t take it away, honey child, they took away being forced to automatically be signed up for it. If you still want the beatings, call them up and they’ll only be too happy to oblige.

RELATED:

Consent-Only Overdraft Protection: Maybe Not So Great

How Card Issuers Sneak Around New Laws

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.