Courey Gouker’s recent experience with American Express encapsulates every trick the company has pulled in the past few months to drive away their customers, including dropping the credit limit, hiking the rate, and even offering him a cash bonus to pay off his balance in full. In addition, the company’s CSRs made promises to him that they didn’t keep, and notes on his account have gone missing. About the only thing they haven’t done is email a photo of the CEO flipping him the bird.

credit scores

FICO Confirms: Reduced Credit Lines For Good Borrowers

By 3.29.09

A study from Fair Isaac confirms that even the best borrowers are seeing their credit lines slashed as banks move to boost profitability during the recession. 16% of Americans have seen their credit lines reduced by an average of $2,200, and of them, 11% had no late payments or negative marks on their credit report.

How To Be A Sexy Borrower

By 3.17.09

and a plunging debt-to-income ratio that reveals a nice plump credit score. Here’s the new rules of credit-worthiness game:

FTC Launches Own Singing Credit Report Commercials

By 3.10.09

As we’ve said repeatedly, AnnualCreditReport.com is the good website to go to when you need to pull a credit report, because it’s actually free. The others, including freecreditreport.com, use the promise of free the way an angler fish uses its forehead-worm-thing to trap dumb little fish. The FTC has decided to fight fire with fire by releasing its own jingles. To be honest, we’re not 100% sold on them—they have kind of a squaresville, PBS vibe, which is gonna really hamper their viral power. Check them out below.

Experian Stoppped Selling FICO b/c Contract Dispute (FICO '08 Related?)

By 2.17.09

Just like I figured, the reason Experian won’t sell you your FICO score anymore is because of a contract dispute with the Fair Issac corporation, and I’m guessing it has to do with the rollout of FICO ’08

Four Unexpected Situations Where Bad Credit Hurts

By 2.15.09

If you aren’t planning on getting a big loan in the next couple of years, you probably shouldn’t be worried about your credit score right? Wrong.

Don't Fall For The Job Hunting Credit Report Scam

By 2.11.09

Christine is looking for a new job, and she found this neat little credit report scam. The scam is pretty transparent in this case, but we thought we’d put it out there as a reminder anyway. Remember, if you want a truly free credit report, only use annualcreditreport.com. Everything else comes with a hidden cost or enrollment in a billed membership—and if a potential employer inists on a specific “free” service that isn’t free when you read the fine print, you can be pretty sure it’s a scam.

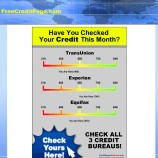

VantageScore And PlusScore Are Garbage Credit Scores

By 2.9.09

Would you buy a credit score that lenders don’t even use? Check it, when Consumer Reports went over the the fine print, Experian’s “VantageScore” says that it’s “for educational purposes only.” And their “PLUSscore” is “not currently sold to lenders.” What good does that do you? None. It’s just something for them to market and make money money off people who don’t know any better.

Experian Yanks FICO Score Away From Consumers

By 2.6.09

Soon consumers will only be able to see two out of the three credit scores lenders use to judge their credit worthiness. Out of nowhere, Experian announced it will no longer be selling its version of the FICO score through myFICO.com.

6 Ways Your Credit Score Changes Thursday

By 2.4.09

A new system for determining your credit-worthiness, FICO ’08, rolls out this Thursday, and there’s nothing you can to do stop it. By these 6 changes, ye shall be judged:

AmEx Denies Existence Of A Store Blacklist, Will Slash Your Credit Whenever They Want

By 1.31.09 — Updated: 11.1.12

Despite sending customers letter saying otherwise, American Express now insists that it never blacklisted cardholders based on where they shopped. Those notes explaining that “other customers who have used their card at establishments where you recently shopped have a poor repayment history with American Express?” Whoops! Just a big misunderstanding! Not unlike the comment they gave to ABC explaining that “shopping patterns” were used as a “contributing factor” in slashing credit lines, a statement AmEx later retracted. So what’s really going on? Let’s explore…

Debunking Five Credit Score Myths

By 1.24.09

Your credit score. It’s amazing how one little score can have such an impact on our finances and how misunderstood that number can be. We’ll debunk five common myths about it right here, right now.

No More Free FICO Scores For WaMu Customers After March 9

By 1.16.09

It looks like after March 1, 2009 quondam Washington Mutual cum Chase customers won’t be able to get their FICO scores for free anymore through their bank. Those people in the picture look pretty excited about yet another WaMu feature being taken away. Woohoo, indeed. [Chase] (Thanks to Luke!)

What's Your FICO?

By 12.16.08

FICO: I’ll show you mine if you show me yours. Take our poll and see how you measure up.

DIY ID Theft Protection

By 12.14.08

Do you want to be one of over eight million identity theft victims? No, but most of the services sold by “identity theft protection” companies you can get for free. Here’s how.

Bad FICO? Here's Three Other Credit Scores That Can Help

By 12.7.08

FICO score isn’t the only credit score game in town. That’s good news for people who have low scores thanks to being an immigrant, divorcee, or don’t have the means to acquire the credit in the first place. It’s one of those quirks of the system. To get credit, you have to have a credit history. To get a credit history, you need to be able to get credit. Thusly, some people find themselves a bit stuck. To meet the needs of these these “thin credit file borrowers”, some alternatives to the standard FICO score are out there. Let’s look at three.

Check Your Credit History Year-Round, For Free

By 12.7.08

Statistics show that 80% of credit histories have at least one error. Most of them are minor and inconsequential but some can have an adverse effect on your credit score, often costing your thousands on mortgages and car loans. I believe credit bureaus were so lackadaisical about accuracy because it forced consumers to buy their credit reporting services. You wouldn’t know there’s an error unless you paid Equifax for a copy of your report. Fortunately, federal law now makes it possible for us to police our own records and force bureaus to correct them, all on their dime. Here’s how:

Hard And Soft Credit Inquiries, And How One Hurts Your Credit Score

By 12.6.08

Did you know that when a company checks out your credit report, it can damage your credit score temporarily? It depends on if the inquiry is “hard” or “soft.” Hard inquiries ding your score, soft don’t. If you’re going to get a mortgage or a car loan, a few points difference translates into a big chunk of change. So how do you know when an inquiry is going to be “soft” or “hard?”