The Fair Isaac Corporation – better known to consumers as FICO – is on the verge of turning the credit score game on its head with the release of a new credit-scoring approach that would consider consumers’ monthly bills, such as those for utilities and wireless plans, when determining creditworthiness. The change is purportedly intended to help consumers on the low end of the credit spectrum, but some consumer advocates are concerned that lower-income Americans could be the ones most adversely affected. [More]

credit history

Potential FICO Credit Score Changes Could Hurt, Rather Than Help Some Consumers’ Creditworthiness

By 4.2.15

Will My Deadbeat Roommate Trash My Credit?

By 4.30.12

A terrible roommate can make your life unhappy in a lot of ways. But let’s say you have a financially irresponsible roommate who never pays their bills. Do their bad habits affect you … other than constantly having to chase down the rent? [More]

"Help, Equifax Won't Give Me My Credit Report!"

By 4.14.10

A reader just had his credit limit lowered on a credit card due to some bad credit history that he says isn’t his. He’d like to see what’s going on with his credit report, but Equifax says he’ll have to pay for the privilege, because they have no record of any inquiries in the past 60 days. The reader asks, “Has this happened to anyone else, where a credit card company waited over 60 days to notify them of credit limit reductions? Also, does this violate the FCRA?” [More]

Are Credit Monitoring Sites Really Worth The Money?

By 4.12.10

Now that everyone is so obsessed with their credit reports and FICO scores, credit monitoring services have popped up everywhere. For a modest recurring fee–one that easily adds up to over $100 a year–you can have a company constantly watch your credit report and alert you of any changes in it, so you can always be on top of your creditworthiness. But should you bother? The consumer director of the U.S. Public Interest Research Groups federation (U.S. PIRG) tells BusinessWeek that credit monitoring is a “protection racket” that turns people into “financial hypochondriacs… who are scared of their own financial shadows.” [More]

Why People Stop Using Credit Cards

By 2.9.10

In yesterday’s Money section, USA Today talked to some consumers who refuse to carry credit cards, and looked at the hidden costs. One 24-year-old says they make her uncomfortable; a guy working at a gas station to pay for college says he doesn’t want to get accosted by endless junk mailings once his name enters the pool of potential customers. Then there’s the bankruptcy lawyer who canceled his cards on principle 8 years ago, after seeing how lenders behaved when their customers suffered financial setbacks: [More]

Experts Answer Credit Questions From Average Americans

By 1.20.10

Henry Unger at the Atlanta Journal-Constitution has put together a multi-part series of questions and answers from readers. The detailed answers are provided by Consumer Credit Counseling Service of Greater Atlanta, and the questions–which I’ve listed below–cover a broad spectrum of personal finance issues, including credit cards, mortgages, and credit reports. [More]

Your Credit Report Isn't The Only Report You Should Monitor

By 11.11.09

When an insurer decides whether to offer you a new policy, or whether to raise rates on a current one, he most likely pulls a CLUE report that lists any homeowner or automobile insurance loss claims (or sometimes even just inquiries) that you’ve made over the past 3-7 years. Hopefully you monitor your consumer credit report for errors, but as you can see, that’s not the only one you should keep an eye on.

FTC Wants Your Input On How To Improve AnnualCreditReport.com

By 10.12.09

The problem with annualcreditreport.com—other than its name—is that getting your reports from the site is a little like dealing with GoDaddy: you have to deal with upsells and side-sells at every step. You can indeed get your free credit reports from the site, but you’ll also have to keep turning down other offers from the three participating bureaus. Hell, there are even ads (sorry, “sponsor” links) on the home page, the one place where you’d hope for the least consumer confusion.

You Paid Your Bill 3 Hours Early? Then It's 30 Days Late

By 10.2.09

John’s fiancee bought an Apple computer earlier this year, financing it with a Juniper Visa account, then paying the account off early. That’s the responsible thing to do, right? Not according to Juniper, which branded her as a filthy, filthy deadbeat. The bank marked the payment she sent in as “late” for arriving three hours before the end of the billing cycle.

Homeowners With Good Credit Are More Likely To Strategically Default

By 9.25.09

Here’s an interesting discovery about mortgage defaults from the LA Times:

Why Credit History Employment Inquiries Matter

By 6.15.09

Last week, we covered a story in which a job seeker was denied a job because of his credit report.

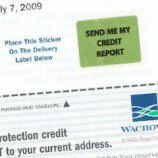

Wachovia Sends Out Its Own "Free Credit Report!" Offer To Customers

By 5.27.09

Tom just received a great offer from his bank. He can receive a free credit report just by peeling off this sticker and affixing it to another part of the same page. That’s right, a free motherloving credit report! Who doesn’t want one of those? Free, you say? Sign me up!

How Credit Bureaus Correct, Or Fail To Correct, Errors On Your Report

By 2.3.09

SmartMoney’s Anne Kadet looked into the process by which the three major credit bureaus—Experian, TransUnion, and Equifax—investigate and correct errors on credit reports. What she found was that the process is “almost entirely automated,” and that “many lenders respond by simply rereporting the erroneous data.” Here’s how it works, and your meager options when something goes wrong.

NewCreditRules Asks, Which Of These Stores Will Get Your AMEX Card Reduced?

By 1.29.09

Last month we posted about Kevin Johnson, a 29-year-old self-employed businessman with excellent credit and an established history with American Express, who had his credit limit cut by 65% because AMEX said he was shopping at the wrong sorts of stores. Johnson has created a website called NewCreditRules.com to try to uncover what, exactly, he did wrong to fall under AMEX’s high risk category.

Can Businesses Really Check My Credit Report Before Offering Me A Job?

By 1.14.09

Reader Brandon wants to know if those freecreditreport.com commercials are being misleading when they tell you that your credit report can affect where you get a job.

DIY ID Theft Protection

By 12.14.08

Do you want to be one of over eight million identity theft victims? No, but most of the services sold by “identity theft protection” companies you can get for free. Here’s how.

Bad FICO? Here's Three Other Credit Scores That Can Help

By 12.7.08

FICO score isn’t the only credit score game in town. That’s good news for people who have low scores thanks to being an immigrant, divorcee, or don’t have the means to acquire the credit in the first place. It’s one of those quirks of the system. To get credit, you have to have a credit history. To get a credit history, you need to be able to get credit. Thusly, some people find themselves a bit stuck. To meet the needs of these these “thin credit file borrowers”, some alternatives to the standard FICO score are out there. Let’s look at three.

What's The Point Of Credit Repair Companies? (Not Much)

By 12.7.08

If you have bad credit and have been thinking about working with a credit repair firm, think again. Credit repair services aren’t doing anything that you can’t otherwise do for yourself. They review your credit history, lodge disputes, follow up, rinse and repeat. The appeal of a credit repair service is that they spend all that time resolving issues so that you don’t have to. They can’t take legitimately negative things off your record and they can’t work magic. Any firm that promises or guarantees to improve your score isn’t telling you the whole truth and you should watch out.