Feds Accuse NetSpend Of Misleading Customers About Prepaid Debit Cards

NetSpend, one of the nation’s largest providers of prepaid debit cards, has been accused of violating federal law for allegedly misleading users into believing that funds loaded onto these cards will be available immediately, while some users say they had to wait weeks or were never able to access their funds.

Earlier today, the Federal Trade Commission filed a complaint [PDF] in a U.S. District Court in Georgia against NetSpend.

According to the FTC, NetSpend misleading markets its cards as ready-to-use, with guaranteed approval. Additionally, the complaint says company tells customers that when a transaction has been disputed, cardholders will be eligible for a provisional credit until the matter is resolved. The government alleges that NetSpend is not being honest about any of these marketing claims.

The following is one of multiple NetSpend ads included in the FTC complaint. You’ll see where we’ve circled that the company is marketing “Immediate access to your funds”:

NetSpend marketing made this sort of pledge in both English and Spanish:

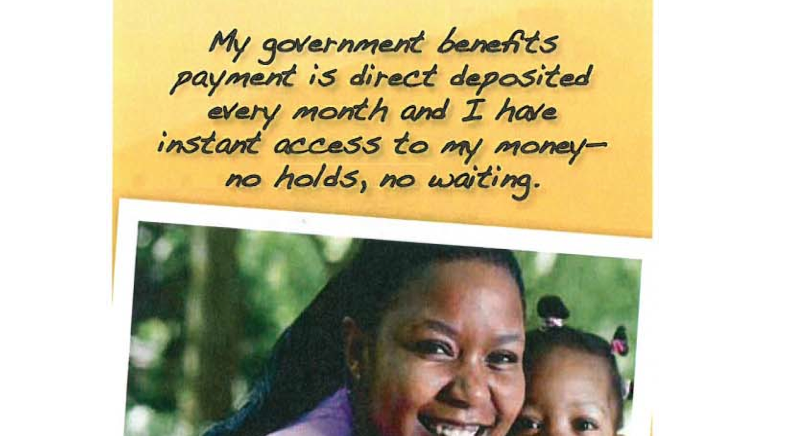

Likewise, this ad promises customers they can get their government benefits on the card with “no holds, no waiting”:

But the reality, claims the FTC, is very different:

“Many consumers have not been able to use their NetSpend cards immediately and have been subjected to delays in accessing their funds when attempting to activate their cards, lift account blocks imposed by NetSpend, or access their payroll, government benefit, or other direct deposits,” reads the complaint. “NetSpend often is slow to resolve account errors, and fails to provide or significantly delays providing provisional credits for account errors. These delays in access to funds are especially harmful to consumers who have made the NetSpend card their primary means of financial management, leaving them without alternative means of accessing funds.”

The FTC notes that most NetSpend users can purchase a card at a retailer and load money into their account, but that’s not the same as actually having access to that money. Just like other debit cards, users must first contact the issuer — in this case NetSpend — to provide personal identification information before the card is fully activated and the user can gain full access to their funds.

In addition to readily available and easily communicated information like address, date of birth, and Social Security number, many NetSpend customers must also provide the company with identifying documents like utility bills, pay stubs, or driver’s licenses.

However, the FTC contends that cardholders are misled by NetSpend’s ready-to-use marketing claims and the fact that retail versions of the debit card are often sold alongside gift cards or pre-loaded debit cards that don’t require this level of ID confirmation to use.

Even when customers do provide NetSpend with the needed information, the FTC says the company doesn’t always activate the card, or the user must repeatedly send in the same documentation.

Exact figures on the number of complaints is redacted in the lawsuit, but the FTC does cite multiple instances of NetSpend taking weeks to activate accounts.

“Many such consumers found themselves without access to hundreds or thousands of dollars while trying to satisfy NetSpend’s requirements to activate their NetSpend cards,” claims the FTC.

NetSpend users also told the FTC that the company blocked access to their accounts after they had already been granted access.

“In many cases, consumers have complained that they were unable to access any of their funds on the cards for substantial periods of time,” says the FTC, “up to weeks or even months after consumers contacted NetSpend to resolve the blocks.”

While these blocks were going on, claims the government, NetSpend still charged account usage fees of between $5-$9.95/month to customers, even though these cardholders couldn’t actually use their accounts.

“Innovative financial products can offer many benefits to consumers. However, when companies promise consumers ‘immediate access’ to their funds, they need to honor those promises,” said Jessica Rich, Director of the FTC’s Bureau of Consumer Protection.

In a statement emailed to Consumerist, NetSpend denies the FTC’s allegations and say it intends to “vigorously contest” the lawsuit.

The company contends that the delays that customers are complaining about are due to ID-verification requirements set forth in the USA PATRIOCT Act.

“NetSpend takes seriously and carefully adheres to these legal mandates to fight identity theft, money laundering and terrorist financing and believes that no one was deceived or harmed by the company’s compliance with these legal obligations,” reads the statement.

Though we should point out that the FTC complaint isn’t taking issue with the fact that NetSpend is required to verify users; the complaint targets the company’s marketing of its cards as being readily available for use after purchase.

Regarding the blocked accounts, NetSpend points again at government regulation, including the FTC’s Red Flags Rule, which requires certain businesses to have written policies for preventing identity theft. NetSpend argues that its fraud prevention processes are “not deceptive, but instead comply with the law and protect consumers.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.