The Good, The Bleh & The Ugly Of State Payroll Cards

Using payroll cards to pay employees is an increasingly popular replacement for traditional checks. In fact, 19 states now use these cards to pay state workers who don’t use direct deposit. And while some of these cards provide employees with easy and affordable access to their funds, most are merely adequate, and some exorbitant fees that can eat into users’ finances.

Using payroll cards to pay employees is an increasingly popular replacement for traditional checks. In fact, 19 states now use these cards to pay state workers who don’t use direct deposit. And while some of these cards provide employees with easy and affordable access to their funds, most are merely adequate, and some exorbitant fees that can eat into users’ finances.

This is according to a survey [PDF] of the different state payroll cards by the National Consumer Law Center.

Unlike some employers who force employees to accept their pay on payroll cards, none of the states currently require that workers receive their pay in this method. In fact, the large majority of state employees are paid through direct deposit to their bank accounts. At the same time, employees who do use payroll cards are often among the lowest-paid workers who are most vulnerable to hefty fees.

The good news is that all of the cards used by these states can — if used wisely — be used for free without incurring fees. They all allow cardholders to withdraw their entire wages at least once per pay period at a bank teller window, give the worker at least one free ATM withdrawal per deposit, charge no fees for purchases, and permits some free customer service calls.

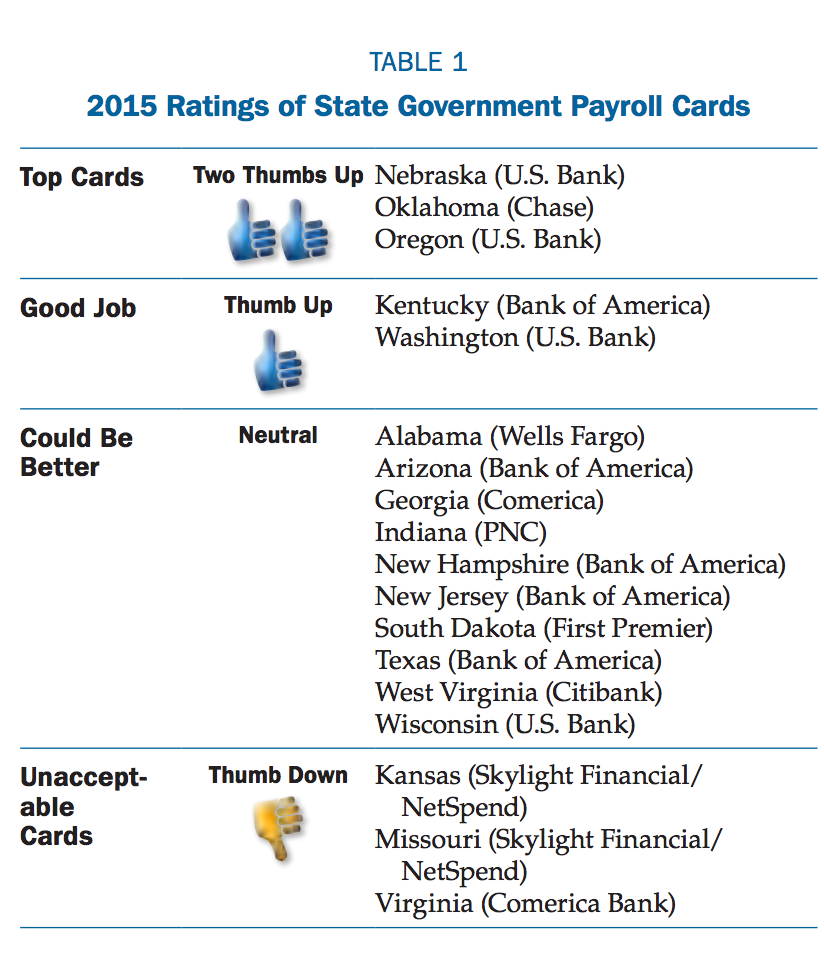

And a number of states have cards that go beyond these minimal standards for acceptable payroll cards. The NCLC report rated cards from three states — Nebraska, Oklahoma, and Oregon — the highest for using cards that charge virtually no fees for cash access, purchases, account information or penalties.

Each of these cards also included at least one free out-of-network ATM withdrawal.

Two additional states, Kentucky and Washington, also earned higher than average marks but fell short of the top rating because they charged fees ($1.25 and $1.75, respectively) for out-of-network ATM access.

A majority of cards fall into a neutral category for offering payroll cards that provided the general benefits of easy access to funds, but with some fees that make them hard to recommend.

Like the Alabama card from Wells Fargo. It offers one free in-network ATM withdrawal and one free call to a live customer service rep per deposit period, but after that you’re going to pay $1.50 and $2.00, respectively, for these. Or the Bank of America payroll cards used by New Jersey, New Hampshire, and Arizona. These cards are relatively fee-free, until the cardholder gets hit with a wage-garnishment order. In which case, BofA charges a $100 “legal process” fee to the employee for something that most of the other card issuers charge nothing.

Which leads us to the bottom of the payroll card barrel — the NetSpend cards issued by Kansas and Missouri, and Virginia’s Comerica payroll card.

For workers who opt in to the NetSpend overdraft protection plan, they face $25 fees for each overdraft, up to $125 a month, and $450 per year.

“Overdraft fees are completely unacceptable on payroll cards,” reads the NCLC report, “and Kansas and Missouri should both be ashamed of paying employee wages on a card that promotes this predatory feature.”

Even though both Kansas and Missouri cards are from the same issuer, the Kansas payroll card hits the user with more fees, like $1.50 charges for every in-network ATM withdrawal after the first one, and $1.00 for every balance inquiry at an ATM (in- or out-of-network).

Virginia earned its thumbs-down from the NCLC for having a wide variety of fees that most cards don’t, like the $50 legal process fee, and $2.50 for bank teller visits (after two free).

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.