Online Payday Loans Cost More, Result In More Complaints Than Loans From Sketchy Storefronts Image courtesy of DCvision2006

We understand why someone might opt for getting a payday loan online instead of doing it in person. It’s easier, faster, doesn’t require going to a shady-looking storefront operation where some trained fast-talking huckster might try to upsell you unnecessary add-ons or tack on illegal insurance policies. But the truth is that people who get their payday loans online often end up in a worse situation than they would have if they’d applied in person.

This is according to a new study [PDF] from the Pew Charitable Trusts on the topic of online payday loans.

For those unfamiliar with payday lending, it generally works like this: A borrower needs a relatively small amount of cash — usually a few hundred dollars — and takes out a loan with a repayment window of usually around 10-14 days. At the end of that term, the borrower is supposed to pay back the amount borrowed plus a lump-sum fee that often equates to an annual percentage rate over 100%.

WHAT’S 650% INTEREST BETWEEN FRIENDS?

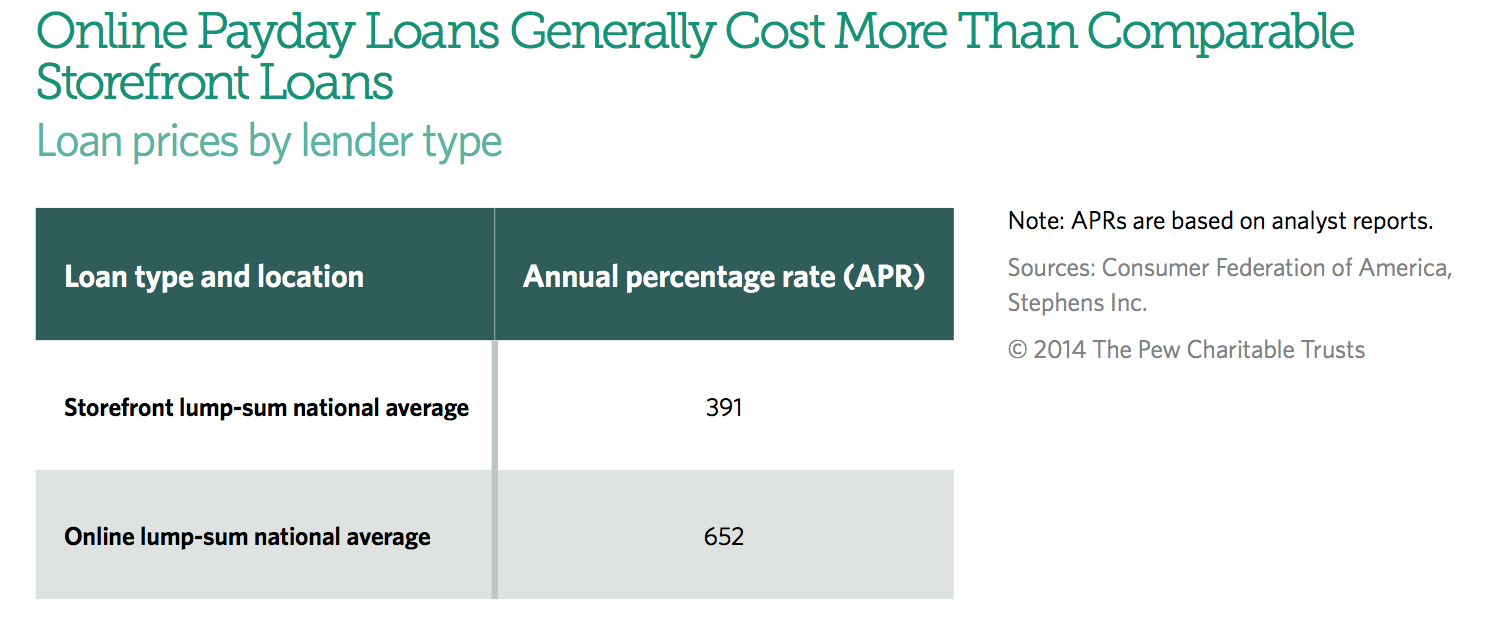

According to the report, the typical storefront payday loan would charge a fee of around $55 for a $375 loan. That’s an APR of around 390%. While that’s astounding, it’s nothing compared to the $95 lump-sum fee that you’d pay for the same loan from an online; that’s an APR of more than 650%.

Payday loans can also be taken out as installment loans, in which the borrower pays back the principal and fees in smaller amounts over a slightly longer time period. Even then, online loans cost significantly more than storefront offerings, according to the study.

Your typical storefront installment loan will hit borrowers with an APR of around 300%, while online lenders charge upwards of 700%.

BREAKING DOWN BOUNDARIES

Of course, this will vary by lender and by state, as a number of states put limits on the maximum APRs of loans. More than a dozen states either outlaw payday lending outright or have such strict lending limits so as to make it not worth the effort for lenders.

But state laws don’t always stop online payday lenders from offering their pricey loans where they shouldn’t. This past summer, a web of online payday operations were indicted for making loans with triple-digit APRs to residents of New York, in violation of the state’s usury laws.

New York also sent cease and desist orders to dozens of online payday lenders operating from Native American reservations, saying that tribal affiliation does not give a lender the authority to break other state’s laws.

There are several apparent reasons that online payday loans cost more than storefront options. The primary driving force of the higher APRs is the higher rate of defaults and losses for online lenders. The Pew study found that the typical storefront operation needs to use about 17% of its revenue to cover losses, while 44% of what an online lender takes in goes to cover its losses.

Additionally, while storefront operations generally spend minimal money on advertising, online payday lenders spend a significant amount of cash on buying online search terms and lead generation.

SOAK, RINSE, REPEAT

With this risk, it means that online lenders have a more pressing need for borrowers who need to take out repeat loans to cover previous loans.

Even charging a 650% APR, an online lender may need a borrower to re-up his loan three times before seeing a profit.

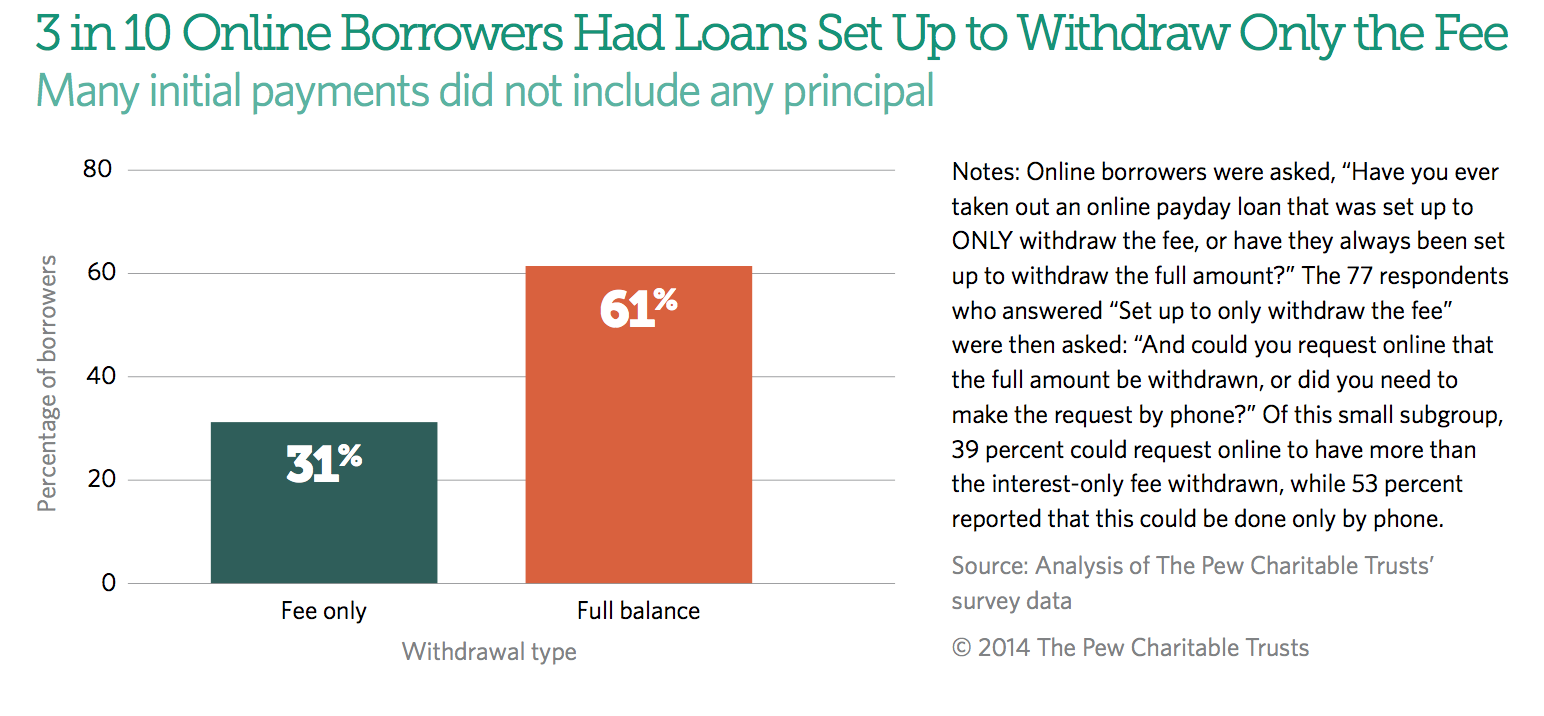

Thus, some online lenders are pushing borrowers into loans where the only amount deducted each payday is the lender’s fee. That means the principal of the loan does not go down, and the loan is just re-upped for another couple of weeks.

One-in-three online borrowers that Pew researchers surveyed were put into a plan of this sort. And of that group, more than half had to actually call the lender to request that more than the fee be deducted.

Websites for these lenders make this sound like a borrower-friendly idea, with statements like “Online customers are automatically renewed every pay period. Just let us know when you are ready to pay in full, and we will deduct your loan plus fees from your bank account.”

If you borrow $375 with a per-term fee of $95, this lender will keep taking that $95 every two weeks until you can repay the $375 PLUS the latest $95 fee. So repaying the loan after six weeks means you would have paid $660 for a $375 loan.

DUDE, WHERE’S MY MONEY?

The Pew report also found that online lenders were twice as likely to make withdrawals that result in overdrafts for borrowers. Only about 1/4 of borrowers say this had happened to them with storefront payday lenders, while nearly 1/2 of online borrowers had experienced this problem.

“I got in a situation where people were taking money out of my account without me knowing,” says one borrower quoted in the report, “and they were taking money out, just kept taking extra money out. … I didn’t know nothing about it, but my bank stopped them. … They were like, ‘You’re having all this money coming out, and you don’t have this money in your account, so what’s going on here?’ … I had to switch banks.”

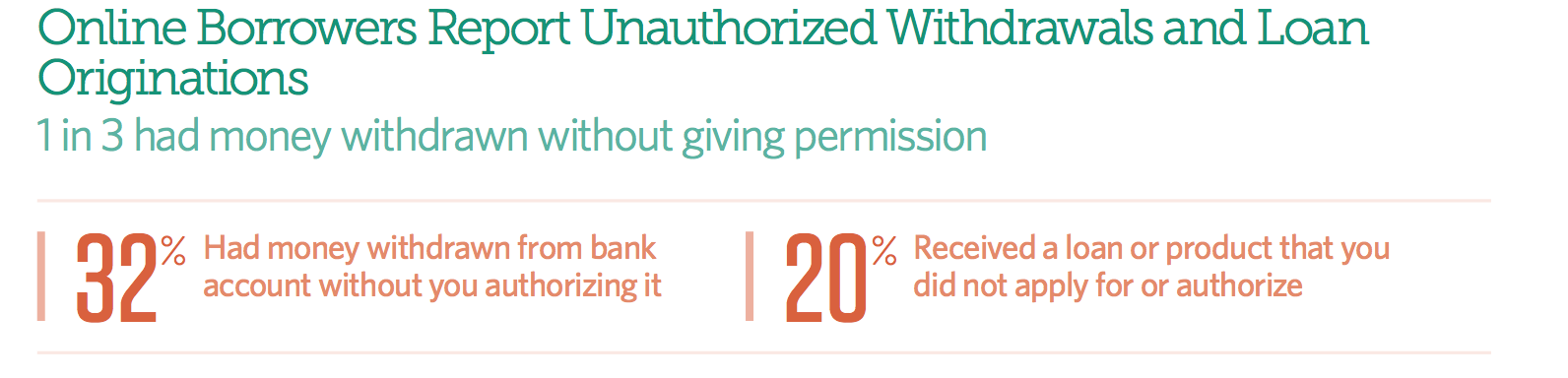

One-in-three online borrowers also reported unauthorized withdrawals from their bank accounts, while another 20% say they received a loan or payment that they did not apply for or authorize.

At the request of the Federal Trade Commission, a court recently shut down a network of payday lenders that was using info from payday lead generators to allegedly dole out unauthorized loans and then start helping themselves to fees from those same bank accounts.

30% of online payday borrowers say they had received at least one type of threat — whether it be the dangling sword of arrest, or claims that the borrower’s family or employer would be contacted about the debt:

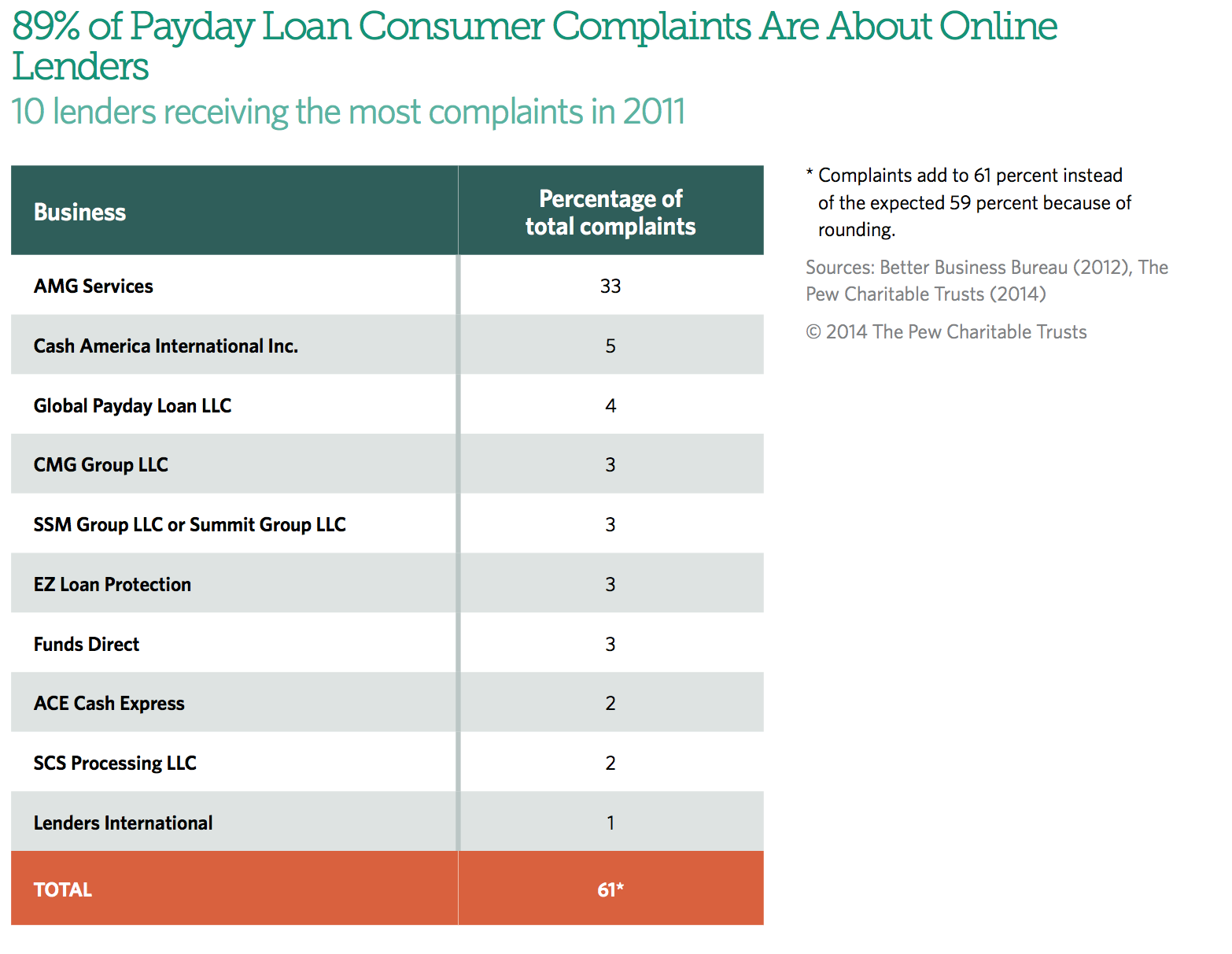

SO FEW LENDERS, SO MANY COMPLAINTS

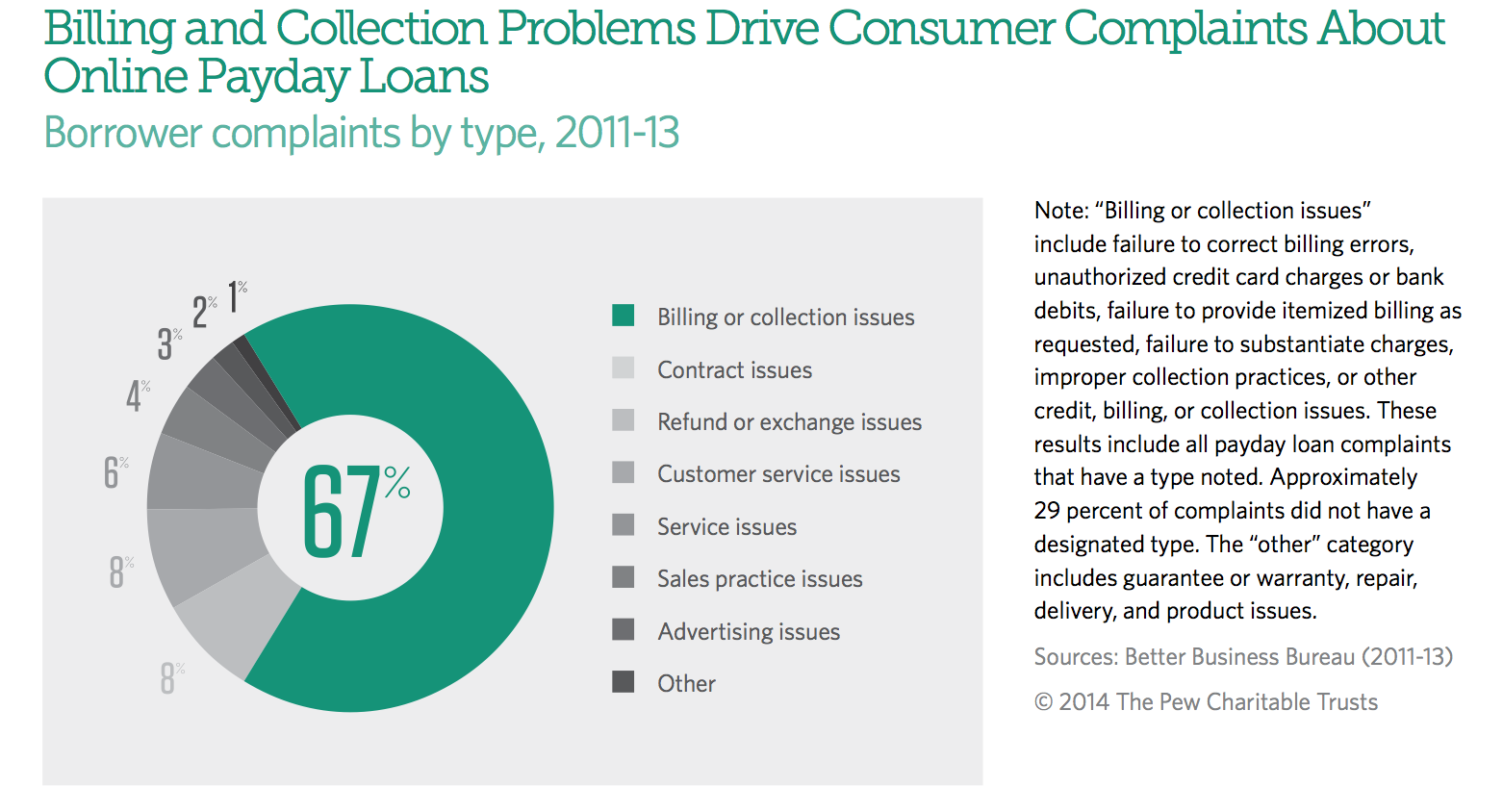

Looking at this info, it may not surprise you that while online payday lenders only account for about 30% of the market, they make up nearly 90% of the payday-related complaints filed with the Better Business Bureau.

And one single business — AMG Services — accounted for nearly 33% of all these complaints. You might remember AMG from its two-year-long legal battle with the FTC, or the fact that I dubbed it one of the scammiest payday lenders I’d ever come across.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.