Small Business Credit Cards Come With Risks That Your Personal Card Doesn't

(WI-LO)

In spite of the “small business” name, there is nothing about most so-called small business credit cards that requires the cardholder to actually own or operate a business. In fact, over a five year period ending last December, credit card companies sent out more than 2.6 billion business card offers to regular Janes and Joes in the U.S. But while these cards are available to the everyday consumer, they do not come with all the protections associated with non-business credit cards.

Business cards have long been exempt from Truth in Lending Act protections because legislators felt that businesses were able to decide for themselves the best way to handle their credit card selection. But these cards are no longer being targeted to just big businesses with employee expense accounts.

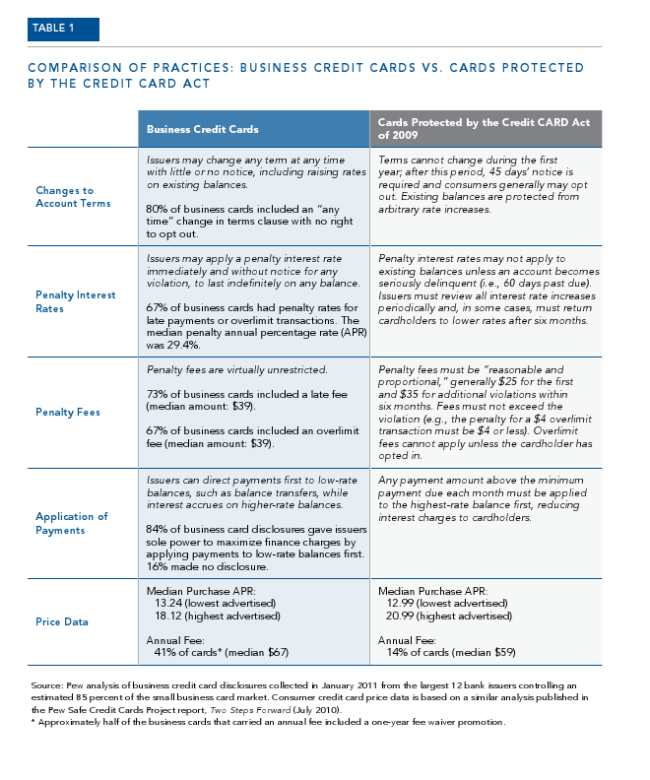

The Pew Trusts recently released a study comparing business cards versus personal credit cards. A chart of the discrepancies between the two types of cards is below, but here are some of the bigger ones:

* Per the CARD Act, banks can not change the terms on your credit card within your first year of having a card and are required to give 45 days advance notice of any changes after that. Meanwhile, the Pew study found that 80% of business cards retain the right to change those terms at any time.

* Penalty fees on personal credit cards are to be “reasonable and proportional,” and the fee can not be larger than the dollar amount of the violation. But the Pew study found that “penalty fees are virtually unrestricted” on business cards and 67% of them include an overlimit fee.

* For personal credit cards, any payment above the minimum amount due must be applied

to the highest-rate balance first, reducing interest charges to cardholders. Business cards have no such restrictions. The study found that 84% of business cards “gave issuers

sole power to maximize finance charges by applying payments to low-rate balances first.” That other 16% have nothing in their disclosure documents about this topic.

Concludes the Pew study:

Though issuers deserve fair compensation for the value they provide to business cardholders, this blanket exemption from consumer protection laws is no longer warranted. Individuals and small business owners have little bargaining power and receive inadequate information about the significant legal differences between consumer

and business credit cards. At the same time, they are personally exposed to risks that cards provided strictly for consumer purposes cannot legally contain.

The reports asks regulators to require credit card issuers to alert applicants whenever a credit card is not covered by the CARD Act, “specifically highlighting the risk of significant interest rate increases on existing balances and higher costs from penalties, payment processing and fees.”

Business Credit Cards Place U.S. Households at Risk [PewTrusts.org]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.