What Happens When You Pay Your $0.19 Amex Bill With 7 Origami Checks?

Bad Consumer Smith finally paid off her American Express Optima card after 14 years, but couldn’t believe that Amex tacked on a $0.19 finance charge to her last bill. Smith summoned her lesser angels to work out a fitting response. Here’s what she came up with:

I sent AmEx two checks for a penny each, one for two cents, two for three cents, one for four cents, and one for a nickel.

I didn’t want them to accidentally drop one, and I was still in a bad mood, so I folded the first check up. Then the second. Then I realized I could fold them all up… around each other.

Topped off with the billing slip, with “stupid bill” written in green marker on it.

Hit the jump for Amex’s response.

Smith writes:

Since at least 1994 I have had an American Express Optima card.

We finally paid the darn thing off.

I waited patiently for my final billing statement, and sent in the payment electronically the next day.

Except AmEx doesn’t believe in Grace Periods, only Average Daily Billing.

So, AmEx decided my final bill of 340 odd dollars was an average daily bill of $23. So they sent me a bill for $.19 interest.

Unfortunately for all involved they sent me that in the middle of a really BAD week.

I thought about this.

What is the most evil way I can pay this thing?

If I do 19 payments of one cent each through my bank it will just go to the AmEx computers. That’s too easy.

I started to send in $.19 from my desktop piggy bank.

Then I realized I wouldn’t know they received it, and I really don’t want a LATE bill for nineteen cents.

So I started to send a check for one center and 18 cents cash. (I have sent in $1.00 or similar checks before with paper forms to other billers— then I know they got the damn thing).

Decided I didn’t want to pay for the postage to mail a nickel.

Realized my bank gives me unlimited checks, unlimited check cashing for free.

So I tear out a chunk of checks.

Realize that if I’m the person processing the check, 19 checks for a penny each is pretty easy.

So I sent AmEx two checks for a penny each, one for two cents, two for three cents, one for four cents, and one for a nickel.

I didn’t want them to accidentally drop one, and I was still in a bad mood, so I folded the first check up. Then the second. Then I realized I could fold them all up… around each other.

Topped off with the billing slip, with “stupid bill” written in green marker on it.

It just might have taken less time to wait on hold and be transferred 17 times trying to get them to waive a bill for $.19, but I have my doubts. AmEx has call centers in India just like everyone else.

Am I a bad consumer, or just sick of bull hockey? How hard would it have been for the computers to be programmed to say, “bill amount is less than cost of mailing, cheaper to waiver bill?” I have one medical laboratory I deal with who doesn’t bill below a threshold — it’s cheaper to eat the bill than send out and process a bill for some minimum.

Stupid conglomeramegacorporation.

-Bad Consumer Smith

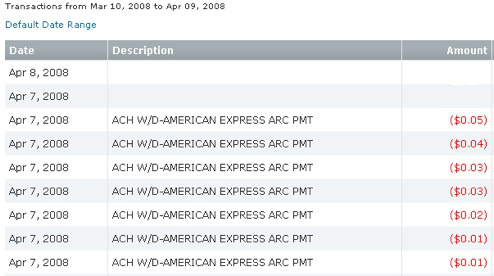

Amex cashed the checks. Each and every one of them. We can’t say we’re surprised, but we do commend Smith for her creativity.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.