Everything You Need To Know To Get Started With Obamacare Open Enrollment Image courtesy of bikeoid

Despite repeated Congressional and Executive branch efforts, the full Affordable Care Act is still in place. That means insurance-shopping season is nearly upon us: Open Enrollment begins Nov. 1 (and ends Dec. 15). But there’s less money being spent on advertising and outreach this year, which means even the basics can be hard to get solid information about. So here’s our when-and-where of getting yourself covered for 2018.

When does Open Enrollment start?

You can begin enrolling in plans for 2018 on November 1, 2017.

When does Open Enrollment end?

If you’re using the federal exchange at healthcare.gov, the deadline to get enrolled in a plan is December 15, 2017.

This is several weeks earlier than in previous years, when the open enrollment period ran to the end of January, so anyone planning to shop for coverage should plan to move quickly. You have 45 days, tops.

Deadlines in the dozen or so states that have their own state exchanges vary, however, and some carry through into 2018 — scroll down and keep reading for details on those.

Do I use healthcare.gov, or what?

That depends on where you live.

Residents of 39 states looking for individual coverage use the federal exchange to buy marketplace health plans. However, 11 states and D.C. have their own exchanges and their own open enrollment deadlines. Those are:

- California — Jan. 31, 2018

- Colorado — Jan. 12, 2018

- Connecticut — Dec. 22, 2017

- Idaho — Dec. 15, 2017

- Maryland — Dec. 15, 2017

- Massachusetts — Jan. 23, 2018

- Minnesota — Jan. 14, 2018

- New York — Jan. 31, 2018

- Rhode Island — Dec. 31, 2017

- Vermont — Dec. 15, 2017

- Washington (state) — Jan. 15, 2018

- Washington, D.C. — Jan. 31, 2018

A heads-up about the states’ open enrollment deadlines: Some states have different (earlier, December) deadlines to obtain coverage starting Jan. 1, but have open enrollment periods that extend through the middle or end of that month, with coverage then beginning in February or March. If you live in one of the states that maintains its own exchange, and it has an open enrollment deadline in 2018, you’ll want to check the terms carefully.

If your state isn’t on the list above, then go to healthcare.gov. (For those who prefer, the Spanish language version is at CuidadoDeSalud.gov.)

Can I enroll whenever I want during the period?

No, at least not if you’re one of the 39 states using Healthcare.gov.

This federally operated insurance exchange will be shut down from midnight until noon on most Sundays during the enrollment period.

The only Sunday where Healthcare.gov will be operating for the full 24 hours is Dec. 10. You will not be able to access the federal exchange for several hours on any of these Sundays: Nov. 5, Nov. 12, Nov. 19, Nov. 26, or Dec. 5.

State exchanges keep their own hours and maintenance schedules, so if you’re in one of the 12 jurisdictions that has its own site you’ll need to check it for more information.

If I miss open enrollment, am I stuck for the whole year?

Yes, but…

There are certain qualifying life events that can allow you to buy a policy outside of the regular enrollment cycle.

Changes that affect your income, your current coverage, or your household composition are those that are most likely to qualify you to change your coverage outside of the open enrollment window. Those include things like gaining or losing a job that provides insurance, having a child, getting married, divorcing the partner under whose policy you were covered, a death in the family that affects your coverage status, or other significant life events.

On the federal exchange, these changes can qualify you for what’s called a Special Enrollment Period. The full list of events is available on healthcare.gov, along with a questionnaire to help you determine if you qualify.

If you live in one of the states that maintains its own site, you’ll need to check your state’s site for more information about special enrollment periods.

What information will I need handy to apply?

First, the basics: Name; Date of Birth; Gender; Street Address; Social Security Number. You’ll need this information for each member of your household.

After that, it starts to get more complicated. You’ll need to provide employment and income information for anyone seeking coverage — so yourself, plus potentially also a spouse or children.

Healthcare.gov has a full checklist [PDF] available to help you make sure you’re gathering all the information you need to; it’s a good idea to check that over before you sit down to apply. State exchanges will require pretty much the same information, so you’ll need to gather it regardless of where you live.

What are all these plans?

Available plans are loosely grouped into four tiers: Bronze, silver, gold, and platinum.

All plans must cover the essential health benefits, and none may discriminate against buyers based on medical history (pre-existing conditions).

Beyond that, however, they do provide different levels of coverage at different price points. A bronze plan will be cheaper than a platinum one, but have significantly higher deductibles, co-insurance payments, and out-of-pocket costs. Some plans may also include other benefits, like vision or dental care.

As a general rule of thumb, the fancier the “metal,” the better the plan — but that coverage comes with a financial cost.

What’s the deal with subsidies? Credits? Financial help? These are expensive!

The majority of Americans who purchase coverage through the marketplace are eligible for some kind of subsidy or credit to offset the costs.

There are two kinds of financial help available: the premium tax credit, and subsidies.

The amount of the tax credit varies widely and depends on your household income level and what kind of plan you want to buy. The Kaiser Family Foundation has a full breakdown of the credit, using 2017 numbers, but it can still be overwhelming; to better understand if or how the credit specifically applies to your situation, you may want to consult expert help.

The cost-sharing subsidies, meanwhile, apply to a narrower range of cases. In order to be eligible for one, your household income must be between 100% and 250% of the federal poverty level, and you must be buying a “silver” plan.

Prices have gone up this year, largely in response to the White House’s decision to stop reimbursing insurers for those subsidies. However, that is already taken into account in the 2018 pricing, and won’t change.

If you are eligible for a subsidy, you will still get one. It’s automatically applied at the time you enroll, and so your initial costs already account for it.

This is super confusing. Help!

It can indeed be really, really confusing — luckily, help is available.

The federal exchange, healthcare.gov, has a call center you can call for help 24/7, with the exception of Memorial Day, July 4th, Labor Day, Thanksgiving Day, and Christmas Day.

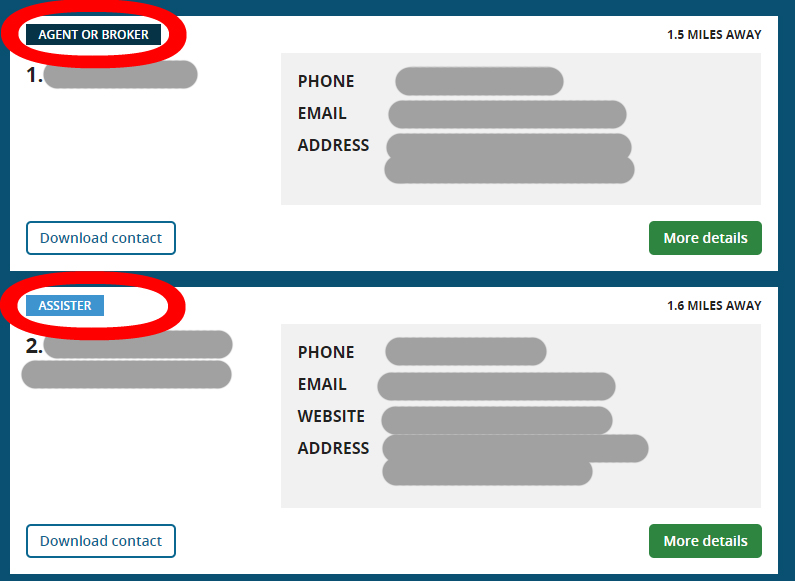

You can also use the search for local help page on healthcare.gov to find in-person assistance near you. That page will ask for your city or ZIP code, and then return a list of assisters and agents/brokers nearby.

Assisters are specifically trained, certified individuals and organizations that help you work your way through your needs and select a plan. Agents and brokers may be required in your area to serve your best interest first, but they are fundamentally there to sell you something — so choose your help accordingly.

When you run a search, the returns will indicate whether someone is an assister or a broker up in the top left-hand corner, like this:

A screenshot from healthcare.gov, highlighting assister vs agent/broker.

If you live in one of the states that maintains its own marketplace, entering your ZIP code into the local help search field at healthcare.gov will return a link to your state’s marketplace page, or you can just go there directly and head for pages that say, “get help” or “find help.”

Several non-profit organizations also provide open enrollment guidance, sometimes broadly and sometimes to specific populations:

- Get America Covered aims to connect anyone looking for coverage with resources.

- Young Invincibles helps young adults ages 18 – 34 understand healthcare resources through its #HealthyAdulting toolkit.

- Out2Enroll helps connect members of the LGBTQ community with ACA enrollment resources.

- Unidos US (formerly the NCLR) has community and advocacy resources for the Hispanic and Latino communities, including a Spanish-language guide to open enrollment.

The Get Covered Connector tool, originally launched by Enroll America and now maintained by Young Invincibles, can also help you find resources near you. It also lets you sort and filter results by more languages than the federal tool does, which can be very helpful if you’re looking for assistance in a language other than English.

You may also be able to find other help in your local community: Public libraries are a great resource. Many have landing pages with local tips, and there may be classes, drop-in sessions, or experts available at yours. A search for [your city, state] library open enrollment can get you started, or you call your library, or go to it, and ask if they have any educational resources available.

I already have a plan for 2017. Do I need to do anything for 2018?

If you’re already enrolled in a marketplace plan this year, you should receive communication from your current insurer and from healthcare.gov before Nov. 1.

Those letters should include details about what will happen in 2018 if you take no action. You may be automatically enrolled in some plan, or you may not; circumstances will vary from person to person.

Basically, if you already have a plan, you need to carefully read communication your insurer and the marketplace send to you, personally, to learn what will happen to you, personally, if you don’t do anything.

However, both healthcare.gov and experts strongly recommend that even if you already have a plan, you should hit the exchange during open enrollment in order to update your personal and household information and to comparison shop: Just because something was the best plan available for you a year ago doesn’t mean that’s still true now.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.