Frequent Overdrafters Spend $450 More In Fees Each Year, More Disclosures Could Help Image courtesy of Steven Depolo

Under federal law, depository institutions are prohibited from charging overdraft fees on ATM and one-time debit card transactions unless consumers affirmatively opted in. But a new report suggests that those who do opt-in might not know the cost of such a decision, with opted-in frequent overdrafters spending about $450 more in fees each year than non-opted-in frequent overdrafters.

The Consumer Financial Protection Bureau released a report today detailing the cost of overdrafting for those who opt in to the coverage, and debuting four prototype disclosure forms explaining the coverage to consumers.

Overdraft

For those unfamiliar, an overdraft occurs when consumers lack the funds in their account to cover a transaction, but the bank pays anyway. If a customer opts-in to overdraft protection, a financial institution may charge a fee for this service, typically around $34 per transaction, and require that the account deficit be repaid with subsequent deposits.

While a recent report from the Pew Charitable Trusts suggested that some banks have improved overdraft policies, they continue to charge high, sometimes exorbitant overdraft fees.

These findings were echoed by the CFBP today in a report highlighting the costs that opted-in frequent overdrafters face. Frequent overdraft users are characterized as those who overdrew their accounts more than 10 times in a 12-month period.

According to the CFPB’s report, of the 40 million checking accounts analyzed, nearly 9% were considered frequent overdrafters, who incur 79% of overdraft fees.

This translates to the typical frequent overdrafter having 22 overdrafts compared to 18 for those who are not opted into protection.

Related: Typical Overdraft Situation Is Comparable To Small-Dollar Loan With 17,000% Interest Rate

These additional overdraft attempts are likely tied to the frequency in which overdrafters use their debit cards. The report found that frequent overdrafters use their debit cards at least 25 times per month; that’s six times more than typical non-overdrafters.

Those who are opted-in typically spend $450 more per year on overdraft fees than those who aren’t opted-in.

Who’s Most Likely To Overdraft?

Most of these frequent overdrafters are financially vulnerable, the study found, with lower daily balances and lower credit scores than people who do not overdraft as often.

For instance, the typical frequent overdrafter has an average end-of-day balance of less than $350, while the typical non-overdrafter has an average end-of-day balance of more than $1,550.

This means that the added costs of overdrafts, which average about $34, can put an additional strain on their finances.

Additionally, those who frequently overdraft have a median credit score of less than 600, well below what is considered to be a subprime score, the report states.

Sen. Cory Booker Concerned Over Hefty Overdraft Fees, Seeks Info From Top Banks

“Our study shows that financially vulnerable consumers who opt in to overdraft risk incurring a rash of fees when using their debit card or an ATM,” CFPB Director Richard Cordray, said.

Know Before You Overdraft

While federal regulations require financial institutions to give customers information about overdrafts and their fees, the CFPB believes more could be done.

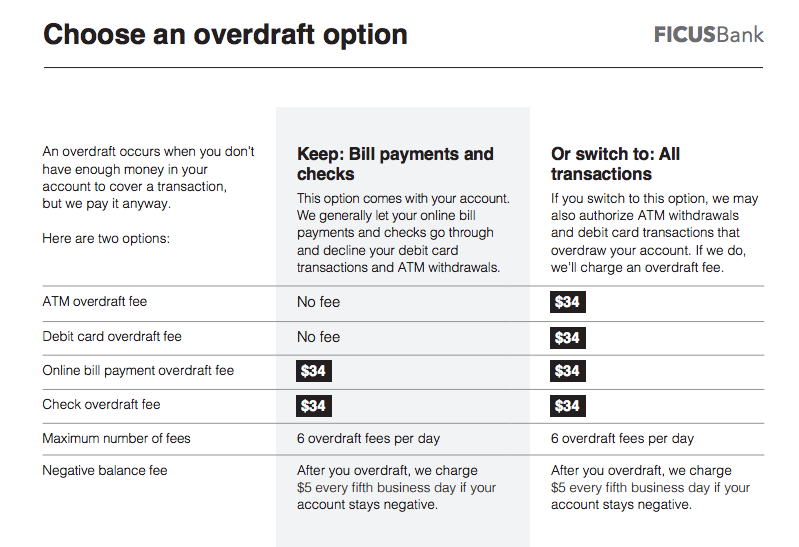

In an attempt to prevent some of these overdrafts, the CFPB has created four prototypes of disclosures [PDF] intended to make the costs and risks of opting in to overdraft coverage easier to understand and evaluate.

The four one-page prototype model forms unveiled today mirror the Bureau’s Know Before You Owe disclosures for mortgages and prepaid accounts, and are designed to give consumers more clarity about a key financial decision.

An example of the prototype disclosures being tested by the CFPB.

The CFPB developed the prototypes through interviews with account holders, and is now testing them more widely.

The prototypes allow banks to plug their specific program information into an online form and then quickly download it for free.

The form would then highlight the fees charged by the bank and would also explain that the opt-in decision applies only to one-time debt and ATM transactions.

In the end, the CFPB believes the prototypes would assist customers in making their own choice about whether they want overdraft service for debt card transactions. The forms would include specific language noting that overdraft protection is optional, and that customers are not required to opt in.

While the CFPB made it clear that it is not currently in the rulemaking process that could require banks to use the prototypes, the agency is considering overdraft regulations and amending them.

“This new approach could make it seamless for banks and credit unions to use a new model form within their existing compliance systems, and easier to update their disclosures following future overdraft program changes,” the agency said.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.