Beverage Industry Takes Philadelphia To Court Over Soda Tax Image courtesy of Mike Mozart

A few months back, the city of Philadelphia became just the second city in the U.S. to successfully pass a tax specifically on soft drinks, adding $.015/ounce to the price a distributor pays for sodas — including diet drinks — and other sweetened beverages. As expected, the beverage industry has fired back with a lawsuit challenging this tax, alleging that it illegally duplicates a state tax and diminishes the purchasing power of low-income Philadelphia residents.

In a complaint [PDF] filed this morning in a Court of Common Pleas in Philly, the American Beverage Association — along with two city residents, a couple of restaurants, two distributors, and other state and city industry organizations — says the city tax is effectively a duplicate of the 6% sales tax placed on these beverages by the state.

The plaintiff’s claim this is a violation of the Sterling Act, a Pennsylvania state law declaring that cities and local governments “shall not have authority to levy, assess and collect… any tax on a privilege, transaction, subject or occupation, or on personal property, which is now or may hereafter become subject to a State tax.”

They contend that Philadelphia knew that simply taxing these drinks at the retail level would violate this law, and so the city “attempted to skirt the preemptive effect of the Pennsylvania Soft Drink Tax by imposing the Philadelphia Soft Drink Tax on ‘the distribution’ of soft drinks… one step up the chain from the actual retail sale of these beverages to consumers.”

Moving the point at which a tax is imposed doesn’t change the fact that it’s a duplicative tax, argue the plaintiffs.

“[T]he relevant question is whether the City’s Tax is imposed on the same subject matter, personal property, and/or transaction as a preexisting Commonwealth tax,” explains the complaint, which contends that the target of the state sales tax on soft drinks is “precisely the same subject and property” as that targeted by the city tax.

Another issue, note the plaintiffs, is the Supplemental Nutrition Assistance Program — otherwise known as SNAP and more commonly referred to as “food stamps.”

Federal law currently prohibits states from collecting a tax on any SNAP-eligible grocery items. So even though Pennsylvania’s 6% sales tax does include soft drinks, state law says taxes can’t be charged on the “sale at retail or use of tangible personal property purchased in accordance with the Food Stamp Act of 1977, as amended.”

By shifting the soda tax to the distributors, who are allowed to pass that cost on to retailers through higher prices, the plaintiffs argue that the city is diminishing the purchasing power of SNAP funds.

One of the resident plaintiffs in the case says in a declaration that she currently purchases 2-liter bottles of soda, using her SNAP benefits, at a price of anywhere from $.79 to $1.29 each. The soda tax would add $1 to the distributor’s cost for each bottle. If that cost gets passed on to the customer, that would have the effect of doubling the price she pays. The lawsuit argues that she would have to make the choice between making that purchase or having less to spend on other items.

“Due to the Tax, a low-income Philadelphia resident making the same purchases he or she had made prior to enactment of the Tax will be able to purchase fewer groceries for the same amount of money than prior to the imposition of the Tax,” explains the lawsuit. “The grocery bill increase will be dramatic for a SNAP recipient, who bears the entire cost of the Tax on the purchase of a soft drink.”

Additionally, claims the complaint, “the Tax shifts federal money that is supposed to be used to increase the grocery-buying power of low-income residents to the City treasury.”

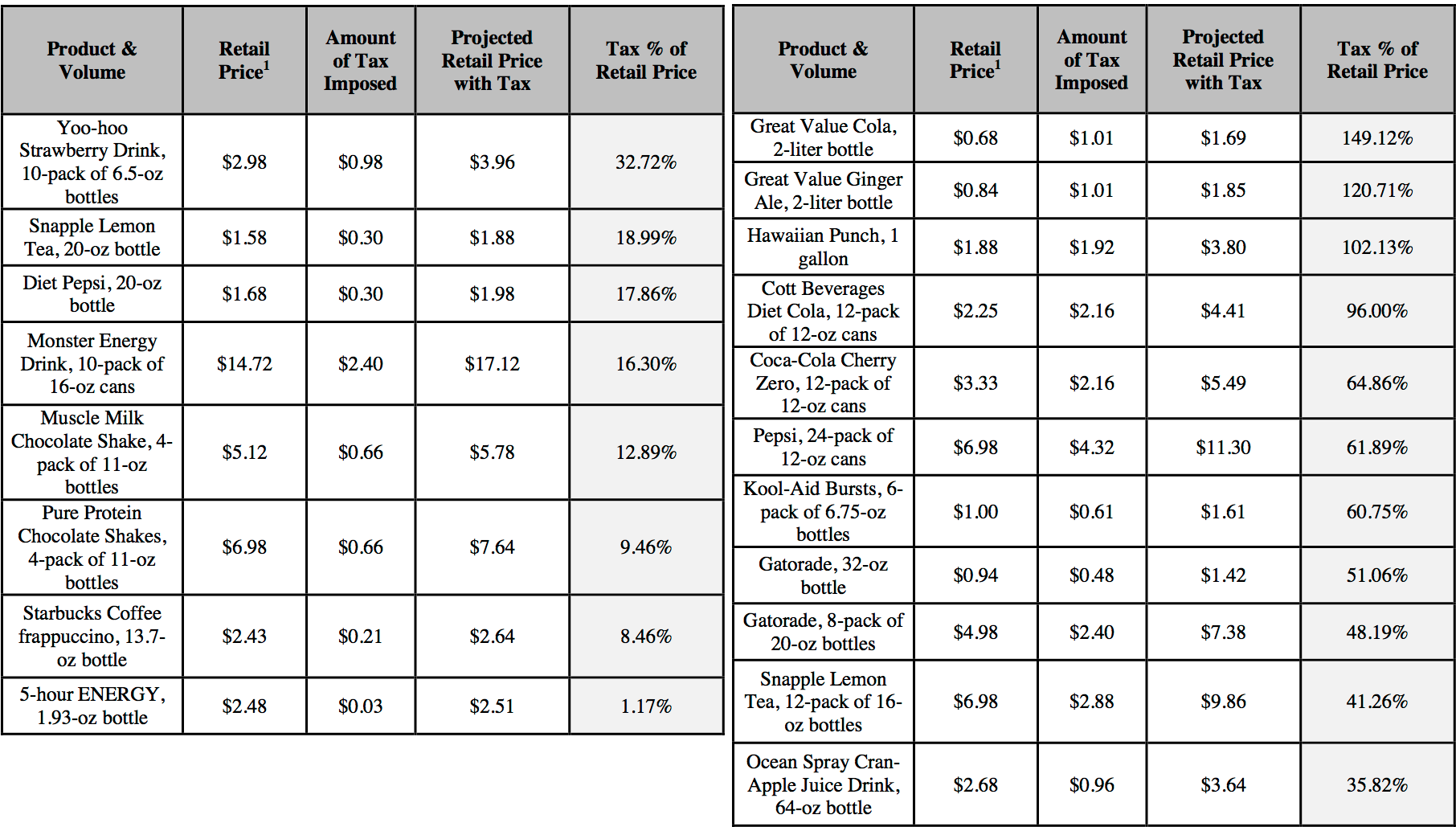

According to the lawsuit, the per-ounce nature of the tax results in an unbalanced system. Unlike the state sales tax, which is based on the retail price of the beverage, basing this tax on volume alone would result in wildly varying price increases.

Using current retail prices from a Philadelphia Walmart, the plaintiffs broke down what a variety of affected drinks would cost, assuming 100% pass-through of the city’s soda tax:

A 2-oz. bottle of a $2.48 energy drink would only go up by $.03, a 1.17% increase. A 20-ounce, $1.68 bottle of diet soda jumps in price by $.30, a change of nearly 18%. A case of 12-oz. cans of soda would go from $6.98 to $11.30, a 62% jump.

The store-brand generic sodas would appear to be hit the largest. According to this chart, you can get a 2-liter of Walmart’s Great Value cola for $.68, but the tax would have the ultimate effect of raising the price by $149% to $1.69.

Again, this all assumes that the distributors would pass these costs on to retailers who would then pass it on to customers. All of the distributors and retailers involved in this lawsuit have declared that they plan to pass this cost on when the tax kicks in on Jan. 1, 2017. They also claim that they will be unfairly burdened with additional costs associated with new record-keeping and lost customers.

“Given how great the tax burden is relative to the market price at the retail level and wholesale price at the distribution level for many beverages, it would be economically infeasible for a distributor or retailer to absorb the Tax,” reads the complaint.

“Philadelphia has lots of ways to raise revenue,” says plaintiffs’ attorney Shanin Specter. “But this tax on beverages is plainly illegal.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.