Amazon & Wells Fargo Hope That A Partnership And Discounts Will Entice You Into A Private Student Loan Image courtesy of thisisbossi

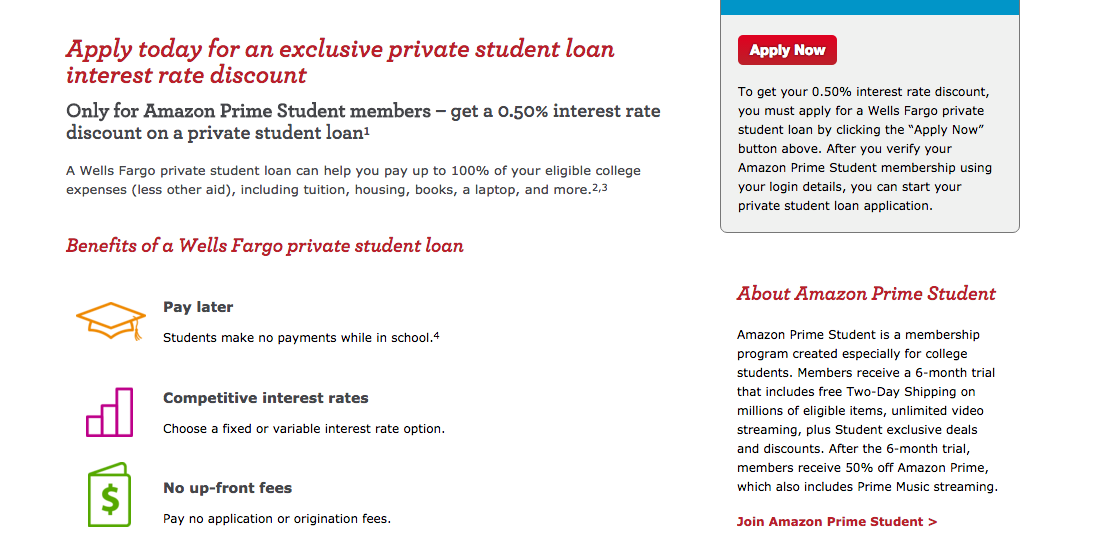

Pay $99/year — or $10/month — for an Amazon Prime membership and you’ll get a slew of benefits like free two-day shipping on thousands of items, free streaming Prime video access, and more. Soon, college-aged members will also be eligible for a 0.50% interest rate discount on new loans.

Amazon unveiled the new loan option on Wednesday in partnership with Wells Fargo, the nation’s largest private student lender amongst U.S. commercial banks.

In addition to receiving a 0.50% discount on new loans, eligible Prime members can receive an additional 0.25% interest rate discount offered when borrowers enroll in an automatic monthly loan repayment plan.

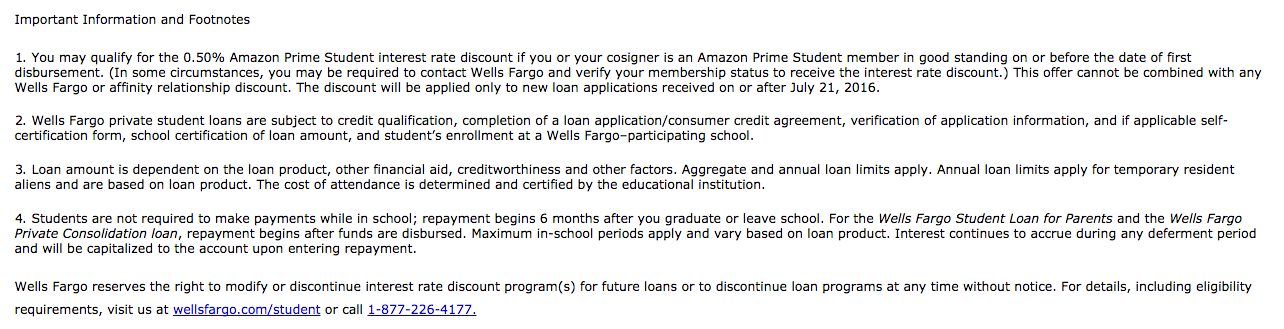

The discounts are available only for new student loan applications received on or after July 21, 2016. That means borrowers who have current Wells Fargo student loans are not eligible for the discount.

“We are focused on innovation and meeting our customers where they are – and increasingly that is in the digital space,” John Rasmussen, Wells Fargo’s head of Personal Lending Group, said in a statement. “This is a tremendous opportunity to bring together two great brands. At Amazon and Wells Fargo, delivering exceptional customer service and helping customers are at the center of everything we do.”

While saving 0.75% on your student loans might seem like a great deal, many advocates say it really isn’t when you consider most students headed for college are eligible for less costly federal student loans.

“The perks of an Amazon Prime membership can’t make up for the fact that private education loans still have fewer consumer protections [than federal loans],” Suzanne Martindale, policy counsel for our colleagues at Consumers Union, tells Consumerist.

Unlike private students loans — like the one being touted by Amazon/Wells Fargo — federal loans always come with flexible repayment and discharge options by law. Those options include protections if you lose your job or experience other hardships that make it tough to afford your payments.

Other advocates say the Wells Fargo/Amazon offer could mislead consumers into thinking they’re getting a good deal when they might not be.

For example, federal student loans currently have a fixed interest rate of 3.76%, while private loans can reach as high as 13.74%.

“This is the kind of misleading private loan marketing that was rampant before the financial crisis,” Pauline Abernathy, executive vice president of The Institute for College Access & Success (TICAS), said in a statement. “Private loans are one of the riskiest ways to finance a college education. Like credit cards, they have the highest rates for those who can least afford them, but they are much more difficult to discharge in bankruptcy than credit cards and other consumer debts.”

Abernathy warns potential borrowers to be on the look out for the fine print of the loans.

“Amazon and Wells Fargo are trumpeting a 0.5% discount while burying the sky-high rates on these private loans and without noting that they lack the consumer protections and flexible repayment options that come with federal student loans,” she says.

Additionally, the fine print for the loans includes a notice that Wells Fargo “reserves the right to modify or discontinue interest rate discount program(s) for future loans or to discontinue loan programs at any time without notice.”

That means that while you might receive a discount when taking out the loan, it isn’t guaranteed to stick.

While Wells Fargo and Amazon contend their new partnership is a way to provide options to college-bound students, advocates say the offer is a new twist on an old scheme.

“Private lenders entering into business partnerships to entice students is nothing new,” Martindale says. “In the previous decade, these lenders partnered directly with college campuses to market their loans – and the schools got kickbacks every time students signed up. Those revenue-sharing agreements between schools and lenders are now banned.”

Financing one’s higher education can be a difficult and information-packed endeavor. And with nearly two-thirds of students who take out student loans unprepared for the financial obligations associated with the debt, advocates advise that they should look at all options available to them.

“If you’re trying to figure out how to pay for college, start with federal aid options first,” Martindale said. “Take out any available grant money, then consider federal loans.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.