NJ-Based Bank Must Pay $33M To Settle Discriminatory Lending Charges

“Redlining” is the act of denying services, either directly or through selectively raising prices, to residents of a certain area based on race or ethnicity. Federal law prohibits creditors from this type of discrimination, but New Jersey-based Hudson City Savings Bank is now on the hook for a total of nearly $33 million for allegedly providing unequal access to credit in parts of four states.

In what is being called the largest redlining settlement in history, the Consumer Financial Protection Bureau and Department of Justice announced today that New Jersey-based today that Hudson has agreed to the conditions of a proposed consent order which directs the bank to pay $27.5 million to increase mortgage credit access in affected areas, and a $5.5 million penalty for allegedly denying black and Hispanic neighborhoods fair access to mortgages.

According to the complaint [PDF], from 2009 to 2013, Hudson City Savings Bank violated the Equal Credit Opportunity Act by engaging in illegal redlining by offering unequal access to credit based on the race and ethnicity of prospective borrowers’ neighborhoods.

“Without access to affordable credit, neighborhoods deteriorate in the long shadow cast by unfair lending,” CFPB director Richard Cordray said on Thursday.

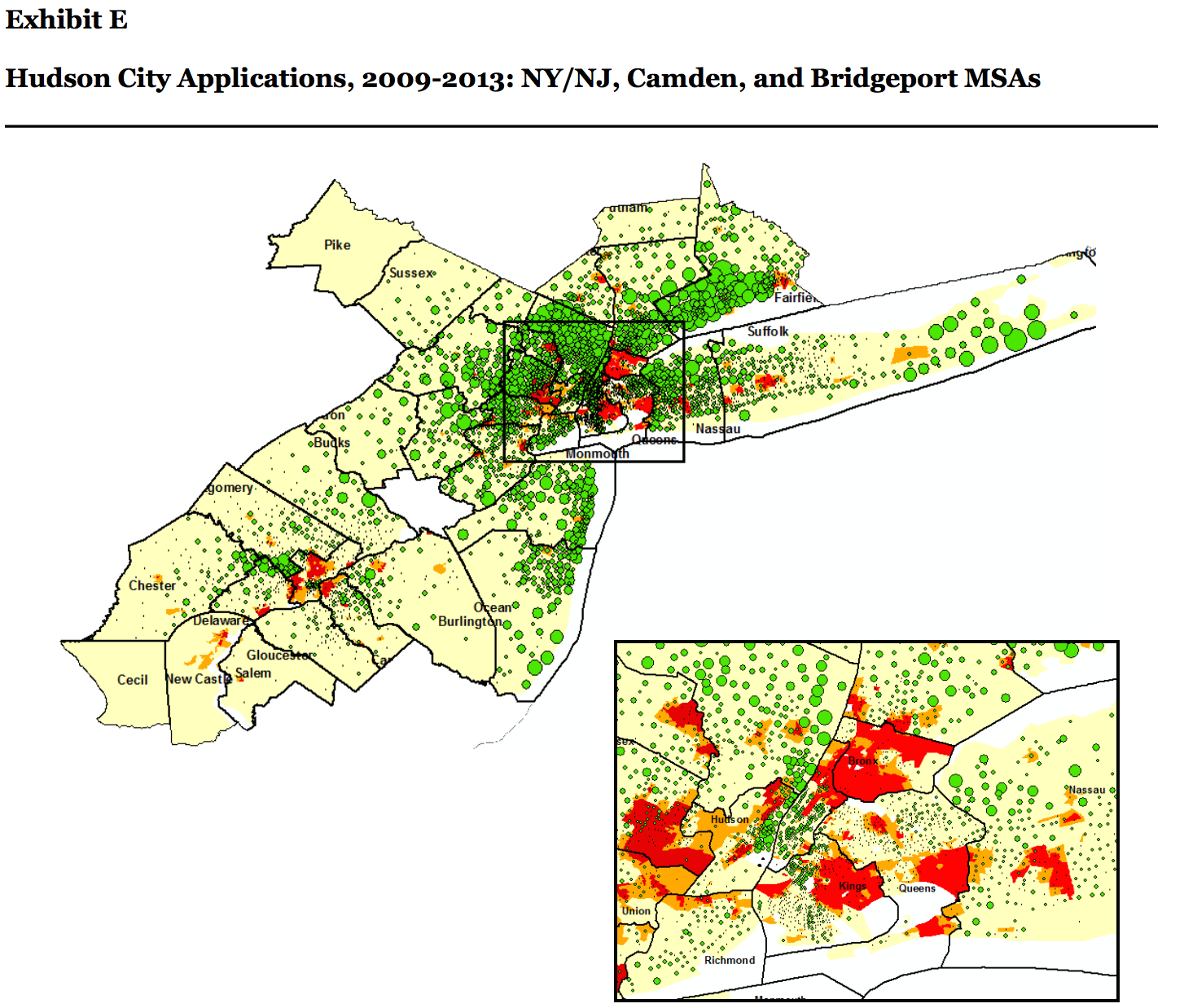

Specifically, Hudson located branches and loan officers, selected mortgage brokers, and marketed products to avoid and discourage prospective borrowers in predominantly black and Hispanic communities in three metropolitan areas [PDF]: New York-Northern New Jersey-Long Island; Philadelphia-Camden-Wilmington; and Bridgeport, Stamford, Norwalk in CT.

Hudson generates the vast majority of its mortgage loan applications for properties within these areas.

However, a joint investigation by the CFPB and DOJ found that from 2004 to 2010, the bank expanded branches in these areas in a way that created a semi-circle around four counties in New York with the highest proportions of majority black and Hispanic neighborhoods.

“Ninety-four percent of the branches opened or acquired as a result of this expansion effort were outside of majority-Black-and-Hispanic neighborhoods,” the complaint states. “Hudson City also placed all of its loan officers outside of majority-Black-and-Hispanic areas.”

By avoiding using mortgage brokers in these areas, the complaint alleges, Hudson generated 80% of its mortgage applications outside of minority areas.

This map shows that, in spite of Hudson’s popularity in the region, the bank was doing very little loan business in predominantly black and Hispanic neighborhoods (those areas marked in red and orange on the map).

In fact, in 2011 and 2012, 94.5% of the company’s top 50 brokers’ offices were not in majority black and Hispanic areas.

When marketing its services, Hudson supposedly limited promotions in neighborhoods in minority areas.

The complaint uses two marketing initiatives as evidence that the company knowingly tried to dissuade minorities from seeking its services.

In one campaign, the company chose Suffolk County, NY, as its base. The county has a lower proportion of majority black and Hispanic neighborhoods than any other county on Long Island.

A second initiative advertised and offered discounted home improvement loans only to residents of certain counties, excluding from eligibility the four New York State counties with the highest proportions of majority black and Hispanic neighborhoods.

Additionally, the complaint accuses the company of excluding such minority areas from its credit assessment areas.

Under the Community Reinvestment Act, Hudson is required to select an area and to meet the credit needs of residents in that area. However, the complaint alleges that in doing so, the bank excluded most or all majority black and Hispanic neighborhoods in the areas selected.

For example, Hudson’s assessment area near Philadelphia and Camden excluded all 337 neighborhoods with a majority of black and Hispanic residents.

Under a proposed consent order [PDF], Hudson must take remedial measures to provide access to credit to the black and Hispanic neighborhoods that it allegedly redlined.

The order, which is subject to court approval, requires the bank to pay $25 million to a loan subsidy program to increase access to affordable credit. The loan subsidy program will offer residents in majority black and Hispanic neighborhoods in New Jersey, New York, Connecticut, and Pennsylvania mortgage loans on a more affordable basis than otherwise available from Hudson.

Additionally, the company must spend $1 million on targeted advertising and outreach and $750,000 on local partnerships with community-based or governmental organizations that provide assistance to residents in the affected areas, as well as provide $500,000 on consumer education during the five-year term of the proposed order.

Hudson must also offer full-service banking, expand assessments, and assess credit needs in the affected areas.

Finally, the company will be required to pay a $5.5 million penalty to the CFPB’s Civil Penalty Fund.

“This case should send a message to lenders throughout the country that the Justice Department will not tolerate racial discrimination in the extension of credit,” Principal Deputy Assistant Attorney General Vanita Gupta, head of the Civil Rights Division said in a statement.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.