Discover Card Program Rewards Students Who Get Good Grades. Is That Legal?

Not so long ago, many college campuses regularly played host to credit card company shills, giving away T-shirts and pizzas to students in exchange for filling out account applications. Then the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009 put an end to most of these practices, leading card issuers to devise new ways to market directly to the under-21 crowd.

Not so long ago, many college campuses regularly played host to credit card company shills, giving away T-shirts and pizzas to students in exchange for filling out account applications. Then the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009 put an end to most of these practices, leading card issuers to devise new ways to market directly to the under-21 crowd.

That appears to be the case with Discover’s student-focused card program that offers a $20 cashback bonus for students who obtain good grades. But does this new program – and its planned marketing initiative – run afoul of the rules?

The answer is no, but many of the card’s features certainly seem to toe the line.

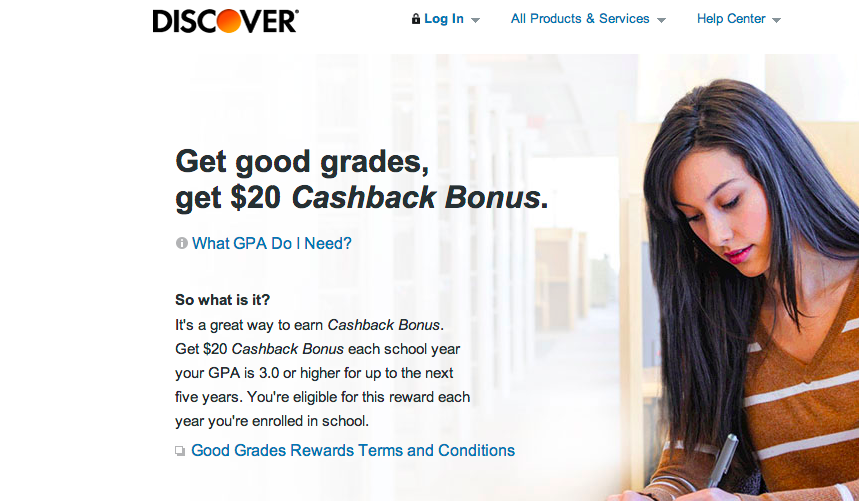

Discover’s Good Grades $20 Cashback Bonus promises to award students who sign up for the card if they achieve a grade point average of 3.0 or higher each year they’re enrolled in school, for the first five years the account is open.

Under the CARD Act, credit card companies can not offer “tangible inducements” to a student at an institution of higher education to apply for or participate in an open end consumer credit plan.

As Derek Cuculich, a spokesperson with Discover points out, card issuers are permitted to provide students with non-physical items, such as rewards points, which happens to be Discover’s incentive of choice for the new program.

“Because the Good Grades feature provides rewards points, it is permissible under the regulation,” he tells Consumerist.

Offering bonus points may be within the parameters of the CARD Act, but what about the way in which Discover promotes the program to students?

Card issuers are also prohibited from marketing credit cards near campus – specifically within 1,000 feet of the border of the campus of an institution of higher education.

Additionally, the restriction extends to “related events” such as concerts and sporting events that may be sponsored by the school.

The Act defines an event as related to the institution of higher education if the “marketing of such event uses the name, emblem, mascot, or logo of an institution of higher education, or other words, pictures, symbols identified with an institution of higher education in a way that implies that the institution of higher education endorses or otherwise sponsors the event.”

In the case of Discover’s student-focused card, Cuculich tells Consumerist that it will be marketed to students digitally, through the mail and over the radio.

So once again, Discover’s Good Grades program meets the CARD Act standards on marketing, as long as it provides clear disclosures in its advertisements.

While the CARD Act certainly makes it clear where card issuers can market their products, it also provides restriction on who they can market to.

“No credit card may be issued to, or open end consumer credit plan established by or on behalf of, a consumer who has not attained the age of 21, unless the consumer has submitted a written application to the card issuer that meets [certain] requirements,” the Act states.

Students under the age of 21 are required to obtain a co-signer before being issued a line of credit. They must also present financial information “indicating an independent means of repaying any obligation arising from the proposed extension of credit in connection with the account.”

What this means is that if a student can show proof of the ability to make minimum monthly payments – such as submitting salary, wages, tips, bonuses and commissions from full- or part-time jobs and self-employment as well as income from interest, dividends, child support, alimony payments, retirement benefits and public assistance – they could take out a credit card if they’re under 21 years of age.

Cuculich with Discover tells Consumerist that the student-focused card – and its rewards program – follow all of the CARD Act provisions related to students eligible for open-end lines of credit.

“If a consumer is under 21, they are still able to apply but they may require a co-signer,” he says. “Our existing processes cover all of these provisions, there are no changes to our process or policy based on this new Good Grades feature.”

The Good Grades program may meet the conditions put forth by the CARD Act, but but consumer advocates want to remind students – along with their parents, guardians or other co-signers – to be cautious about opening any new line of credit.

Suzanne Martindale, staff attorney with Consumers Union, notes that while the restrictions of the CARD Act protect students over 21 from being unfairly lured into taking out a credit card, it’s important for those who co-sign for students under 21 to remember their obligations.

“Parents who co-sign would be on the hook if their student can’t pay the bills, so it’s important to discuss as a family before signing up,” she says.

Additionally, being attentive to terms and conditions is especially important if a student’s college or university has an agreement with the card issuer to provide information about products to students.

These relationships, which have come under increased scrutiny by regulators in recent years, often include kickbacks for the schools based on the number of students who open cards.

Under such agreements credit card companies can issue debit or credit cards to students, while colleges and universities receive millions of dollars a year in royalties and bonuses by allowing said companies to use their logos and approach their students.

While schools required to made such agreements publicly available, a report from our colleagues at Consumers Union found many colleges make it difficult to obtain such information.

“We found it can be challenging, if not impossible, for a member of the public to get information about college credit card agreements,” Martindale said at the time. “It just adds to the confusion and secrecy surrounding these partnerships.”

In light of the investigation’s findings, CU urged the CFPB to continue to implement the CARD Act and actively promote compliance at all colleges and universities that hold agreements with credit card companies.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.