Regulators Sue To Shut Down Illegal Offshore Payday Loan Network Image courtesy of (scurzuzu)

(scurzuzu)

While most of us think of payday lenders as small-time storefront operations, there is also a complicated web of interconnected payday businesses operating outside the U.S. borders, but illegally issuing costly short-term loans to American borrowers. A newly filed lawsuit hopes to put an end to one such network.

The Consumer Financial Protection Bureau filed a lawsuit [PDF] in federal court against NDG Enterprises – an operation consisting of 11 companies – for purportedly issuing illegal payday loans and then using aggressive means to collect those debts.

The companies named in the complaint include Canadian corporations NDG Financial Corp., Ltd., E-Care Contact Centers, Ltd., Blizzard Interactive Corp., Sagewood Holdings, Ltd., New World Consolidated Lending Corp., New World Lenders Corp., Payroll Loans First Lenders Corp., and New World RRSP Lenders Corp. Two other companies, Northway Financial Corp., and Northway Broker, Ltd., are incorporated in Malta.

According to the CFPB complaint, since at least July 2011, the companies in the syndicate have issued short-term loans in all 50 states, including those where laws impose interest rate caps and licensing requirements that essentially outlaw such costly financial products.

Each of the companies under the Enterprise umbrella served a specific purpose in the overall operation.

For example, Blizzard identifies customers for Northway’s loans by purchasing leads from lead generators, some of which are websites operated by Northway Broker.

One of the criteria that Blizzard uses to identify customers is the consumer’s state of residency. According to the complaint, in June 2013, the company focused on consumers residing in the United States, with the exception of Georgia, Pennsylvania, Puerto Rico, West Virginia, American Samoa, Guam, Mariana Islands, and North Dakota.

States targeted by the company included New York which has laws prohibiting high interest short-term loans.

Once the leads were purchased, consumers were directed to Northway-managed websites where they were required to create a user account that included their checking account number, social security number, date of birth, and home address.

The companies then used this information to disburse loans and collect on owed debts.

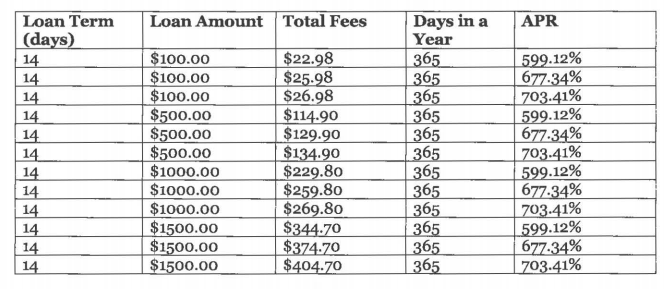

Loans offered by the operation were generally short-term (14 days), ranging from $100-$1500 with finance charges between $19.98 and $26.98 per $100 borrowed.

The complaint includes examples of the enterprise’s payday loan costs. In this case from the CashTaxi.com website managed by Northway.

Once loans have been issued to the consumer, collection activities are taken over by E-Care on behalf of the Enterprise.

The CFPB alleges that E-Care used a host of deceptive and illegal debt collection tactics to obtain payments from consumers.

In many cases, the company initiated contact by phone, e-mail, and letter with a restatement of the consumer’s obligation to repay the principal and interest in full, along with a $39 non-sufficient funds fee, and a $20 late payment fee.

According to the complaint, many of the loan agreements made between the issuer and the consumer included a wage assignment clause, that states if a consumer defaults on the loan for more than seven days from the date that payment is due, the consumer authorizes NDG Enterprise to instruct the consumer’s employer to pay the outstanding amount directly to NDG Enterprise from consumer’s wages.

When a wage-assignment agreement wasn’t available, the CFPB alleges E-Care falsely told consumers that non-payment of debt would result in lawsuit, arrest, imprisonment, or wage garnishment, despite lacking the intention or legal authority to take such actions.

In addition to using threatening tactics to recoup loan costs, between July 21, 2011 and 2014, the Enterprise furnished information to credit reporting agencies on trade lines belonging to consumers residing in all fifty states, including approximately at least 15,000 trade lines belonging to New York residents.

According to the CFPB, loans issues to residents of several states, which have usury laws in place, are void because of their illegal nature. These states include Alabama, Arizona, Arkansas, Illinois, Indiana, Kentucky, Massachusetts, Minnesota, Montana, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Ohio, and Utah.

Despite this, the companies often claimed to consumers that because they were incorporated outside of the U.S. they did not have to abide by such state laws.

For example, the companies – in most cases Northway and Northway Broker – would send a letter to consumers stating:

If you take a moment to review the attached loan agreement, you will see that Northway Financial Corporation Ltd. is a Financial Institution licensed and regulated in accordance with the European Union (EU) Directives. As such, the laws of the Republic of Malta (member State of the European Union), not the state of [consumer’s state of residence] applies to its terms. We provided you with this notice so that you would understand the terms of your loan.

In response to hundreds of complaints against Northway, several states issued cease and desist orders, directing the company to stop issuing loans that don’t comply with lending law protections. However, the companies continued to originate, service and collect loans in those states, the CFPB complaint alleges.

In all, the CFPB alleges that the Enterprise violated the Dodd-Frank Wall Street Reform and Consumer Protection Act’s prohibition on unfair, deceptive, and abusive acts and practices.

Specifically, the companies made false threats to consumers, deceived borrowers about their debts and used illegal means such as wage-assignment clauses to collect on void debts.

With its lawsuit, the CFPB seeks to refund the money the companies took from consumers where the loan amounts were void or the consumer otherwise was not obligated to repay the loan.

Additionally, the Bureau seeks to prohibit the companies from any further violations of federal consumer laws related to unfair, deceptive, and abusive acts and practices.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.