Most State Laws Can’t Protect Borrowers From Predatory Installment Loans, Open-End Lines Of Credit

As regulators continue to craft rules meant to crackdown on costly and harmful short-term payday lending, companies are offering alternative products like installment loans and open lines of credit to consumers. But, as it turns out, these cash infusions can be just as devastating to those in need, and few states offer sufficient protections for borrowers.

That’s according to a new report [PDF] from the National Consumer Law Center that analyzes laws regulating installment loans and open-end lines of credit in all 50 states and the District of Columbia.

Caps on interest rates and loan fees are the primary way state laws protect borrowers. However, as with payday loans, the report finds that while some states do pretty well in protecting residents from unscrupulous lenders, others leave consumers ripe for the taking, either through lax regulations or loophole-filled laws.

“In theory, installment loans can be safer and more affordable than balloon payment payday loans. But states need to be vigilant to prevent the growth of larger and longer predatory loans that can create a debt trap that is impossible to escape,” said Carolyn Carter, director of advocacy at the National Consumer Law Center and co-author of the report.

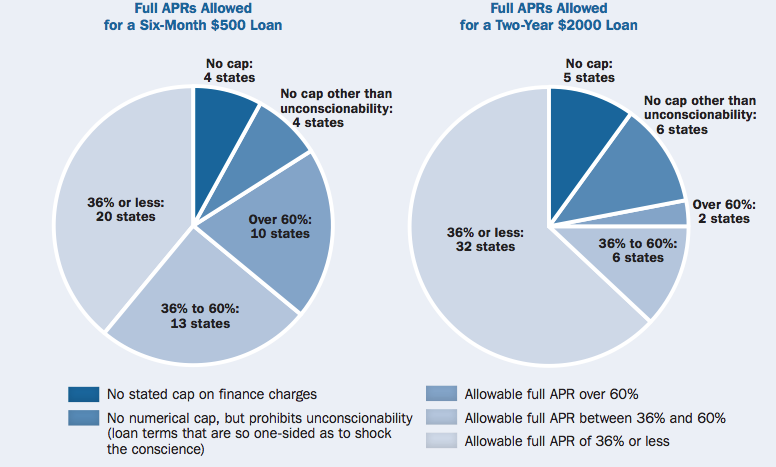

Fewer than half the states cap interest rates on 6-month, $500 loans at 36% or less. For 2-year, higher-value loans, there are 11 states that don’t even specify a cap on interest rates.

In all, NCLC found that 19 states and the District of Columbia have the most stringent, consumer-friendly restrictions, limiting the full APR of closed-end installment loans to between 16% and 36%.

Some other states place reasonable limits on interest rates, but allow lenders to charge fees – for things like loan-origination – which increase the full annual percentage rate.

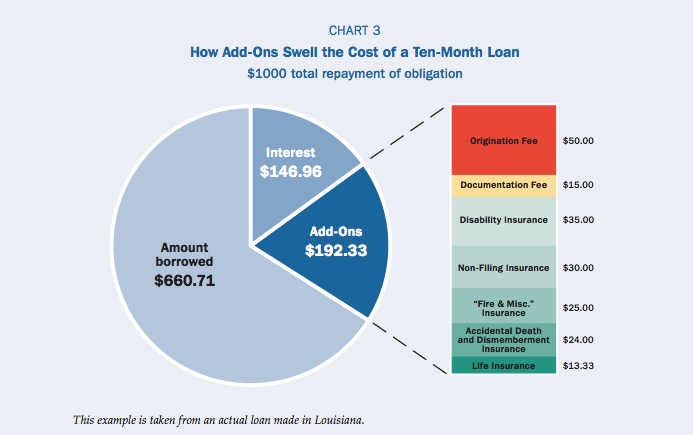

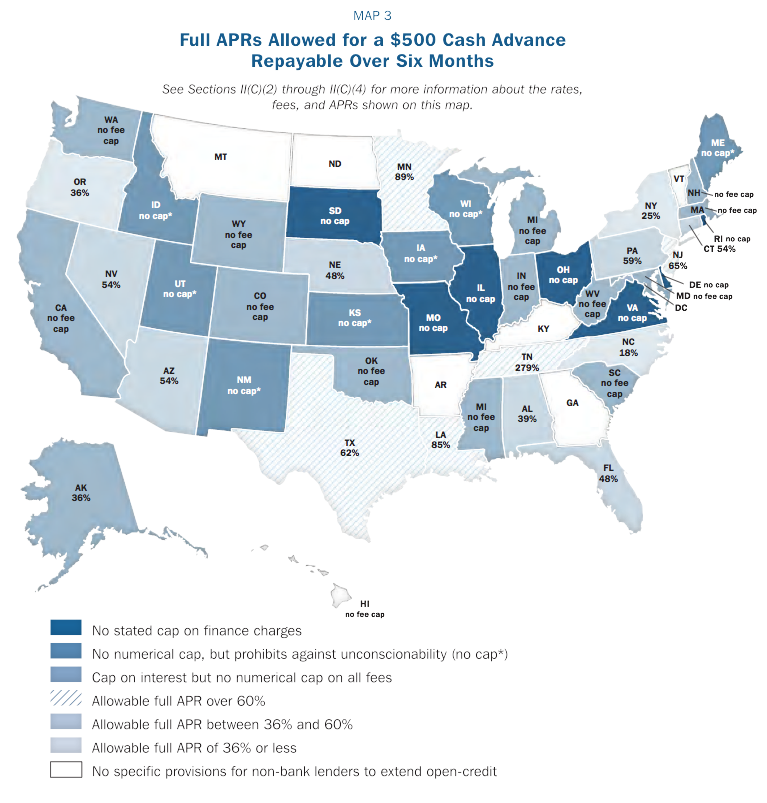

Such is the case in Louisiana, where laws cap the interest rate for a $500 loan at 36%. But because the state allows additional fees to be tacked on – like $20 for documentation and $50 for origination – the actual full APR of the loan becomes 85%.

Add-ons allowed in states like Louisiana defeat the purpose of initial interest rate caps.

The report found that 13 states allow interest and fees that can bring the full APR of a loan to as high as 545%, while 10 allow fees and interest that can bring the full APR for a $500 loan up to between 61% and 116%.

Worse yet are the four states that place no cap on the interest rate except that it cannot be “unconscionable,” while another four have no such rate caps or restrictions.

Still, NCLC points out that most states do impose lower rate caps for larger loans. Take for example, Iowa’s Regulated Loan Act which caps interest at 36% on the first $1,000, 24% on the next $1,800, and 18% on the remainder. The resulting APR, which blends these rates, is 31% on a $2,000 loan.

On the other end of the alternative loan spectrum are open-ended lines of credit – like credit card cash advances – which are often loosely regulated by states.

In fact, 44 states have non-banking lending statutes that allow open-end credit, and many of those do not cap interest rates or have ambiguous limits, NCLC reports.

For example, Tennessee recently enacted an open-end credit law that purports to limit interest to 24%, but allows a daily charge that brings the full APR up to 279%.

According to NCLC, provisions like the one in Tennessee give lenders incentive to structure loans as open-end credit in order to skirt rate caps.

Of the 44 states whose non-bank lending statutes specifically allow open-end credit:

• 14 states fail to cap rates for a $500 cash advance and 16 fail to cap rates for a $2000 advance.

• 14 states have rate caps but do not have unambiguous, airtight caps on the fees that lenders can impose for a $500 cash advance, and 13 fall into this category for a $2000 advance.

• For a $500 cash advance, seven states cap it between 39% and 54%, four cap it AT 59% to 89%, and Tennessee caps it at 279%.

• For a $2,000 cash advance, 11 states cap the full APR at 36% or less, three states cap it between 39% and 42%, and Tennessee caps it at 279%.

As federal regulators like the Consumer Financial Protection Bureau move to create laws governing the single-payment payday loan industry, NCLC suggests that the loopholes and lax restrictions currently governing installment loans could prove to be fertile ground for unscrupulous lenders.

“This should be a concern in all states that do not cap interest rates, or have high or ineffective caps, for installment loans or open-end credit,” the report states. “In payday loan states, lenders may simply move to high-cost installment loans or credit lines. As high-cost installment loans or credit lines take root, they may also migrate to non-payday states that do not have sufficient protections.”

The NCLC report makes several recommendations for states looking to protect consumers from these potentially predatory practices, including:

• Place clear, loophole-free caps on interest rates for both installment loans and open-end credit. A maximum APR of 36% is appropriate for smaller loans, such as those of $1000 or less, with a lower rate for larger loans. Prohibit or strictly limit loan fees, which undermine interest rate caps and provide incentives for loan flipping.

• Ban the sale of credit insurance and other add-on products, which primarily benefit the lender and increase the cost of credit.

• Require lenders to ensure that the borrower has the ability to repay the loan according to its terms, in light of the consumer’s other expenses, without having to borrow again or refinance the loan.

• Minimize differences between state installment loan laws and state open-end credit laws, so that high-cost lenders do not simply transform their products into open-end credit.

• Make unlicensed or unlawful loans void and uncollectible, and allow both borrowers and regulators to enforce these remedies.

By pointing out the weaknesses in state laws regarding these alternative payday products, NCLC hopes states will examine their regulations to better protect consumers when it comes to the changing loan industry.

“Reasonable interest rates align the interests of the lender and the borrower and provide an incentive to make loans that a borrower can afford to repay,” Lauren Saunders, co-author and attorney at the National Consumer Law Center, said in a statement. “We hope this report will prompt states to examine their laws to eliminate loopholes or weaknesses that can be exploited and to be on the lookout for seemingly minor proposals to make changes that could gut consumer protections.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.