Banks Continue To Improve Consumer Safeguards, But Progress Isn’t Coming Fast Enough

Opening a checking account with a bank is a rite of passage of sorts for many consumers, but the plethora of small-print disclosures, fees and other services are enough to confuse even the most seasoned account holder. While banks attempted to simplify their practices over the years, a new Pew Charitable Trusts report shows that some banks – and regulators – have a long way to go before they’re truly doing everything they can to protect consumers.

The new report [PDF], the third in the organization’s Checks & Balances series, analyzes 45 of the 50 largest banks in the U.S. – 32 of which have been examined in all three of Pew Charitable Trust’s reports since 2013.

Banks are evaluated for their “best” and “good” practices across three categories: disclosure, overdraft, and dispute resolution.

According to Pew, best practices are defined as those that are most effective in providing checking account holders with clear and concise disclosures about fees and terms; reducing the incidence of overdrafts; eliminating practices that maximize overdraft fees; and allowing consumers to choose the method by which they resolve a problem with their bank, rather than requiring pre-dispute binding arbitration.

In all, the report found just one bank that received best practices across all three categories.

While most banks continued to improve regarding disclosures, the prevalence of harmful overdraft fees and account terms changed very little, or in some cases got worse during the past 12 months.

DISCLOSURE PRACTICES

When it comes to disclosure practices – how a bank informs consumers about services, fees and other account details – Pew found continued progress in making this information clear and concise for consumers.

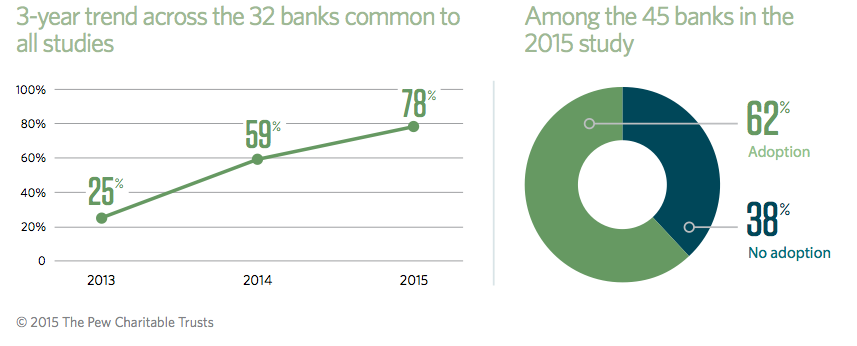

More banks than ever have adopted comprehensive disclosure forms for consumers.

Of the 45 banks analyzed this year, nearly 62% had adopted complete disclosure boxes.

Still, the study finds that the average length of a financial institution’s disclosure form is 40 pages, too long to be helpful or easily digestible for consumers, Pew says.

OVERDRAFT PRACTICES

Overdrafts and their resulting high fees have long been a point of immense scrutiny for consumer advocates.

Since 2010, financial institutions have been required to obtain an opt-in confirmation from consumers before enrolling them in overdraft penalty plans. These plans involve the bank making a short-term advance to cover the transaction and charging a fee for the service.

Despite federal regulations, a June 2014 Pew report found that more than 50% of people who incurred such penalty fees in the previous 12 months didn’t believe they had opted into any such plans.

Those figures are likely to change in 2015, if Pew’s latest study is any indication. That’s because all 45 banks studied for the most recent report provided clear disclosures regarding the fee for incurring an overdraft penalty, if they enrolled in the program.

The report found that many banks have also improved their default disclosures for account holders. The default allows ATM and point-of-sale transactions to be declined at no cost if the account holder if the transaction would cause the account to be overdrawn.

In fact, 84% of the banks that have been studied since 2013 have made the default option clear to consumers, an improvement of 37% since the first report.

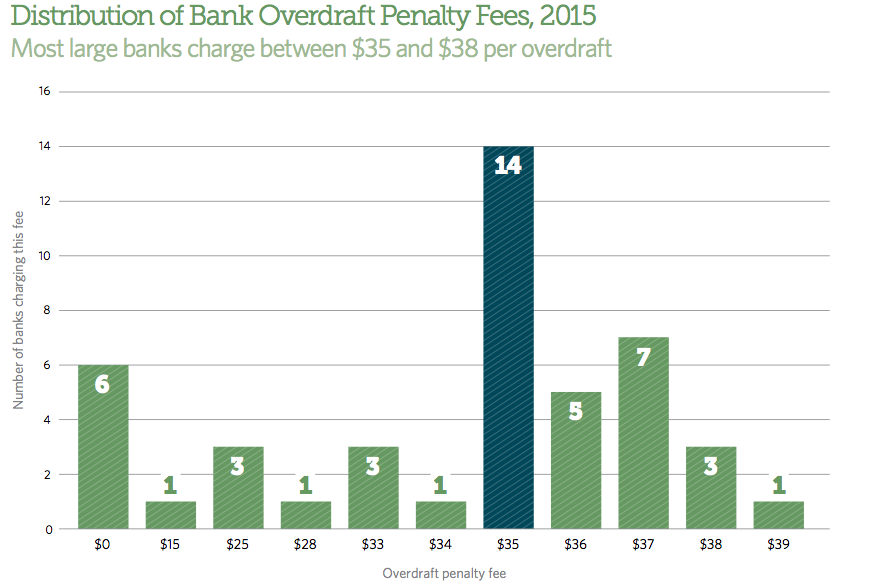

Once again, the average overdraft fee clocks in at $35.

Pew also looked specifically at the practices of the country’s largest three banks – Wells Fargo, Bank of America and JPMorgan Chase – and found an array of policies regarding overdrafts.

For instance, Bank of America doesn’t allow customers to overdraw at the point of sale but does allow them to withdraw “emergency cash” at an ATM in excess of the available balance for an overdraft fee; a practice Pew describes as an ATM overdraft.

On the other hand, Chase doesn’t allow ATM overdrafts, but does allow point-of-sale overdrafts, while Wells Fargo allows both types of overdrafts.

Pew found that some banks continue the hazardous practice of processing transactions from largest to smallest, an act that can maximize the number of overdrafts charged.

Of the banks surveyed all three years of the study, Pew found that 91% no longer reorder transactions, up from 88% last year. When all 45 banks are considered, 84% have no or limited high-to-low reordering of transactions.

In all, four of the 45 banks surveyed this year recorded best practices for all of Pew’s overdraft categories.

DISPUTE RESOLUTION

For years now, companies have been taking away consumers’ right to sue them when they screw up through the use of small, hidden clauses to require mandatory binding arbitration instead

Earlier this year, the Consumer Financial Protection Bureau found that 75% of consumers surveyed did not know if they were subject to an arbitration clause in their credit card contract.

More banks are ensuring that customers have full access to all available legal remedies.

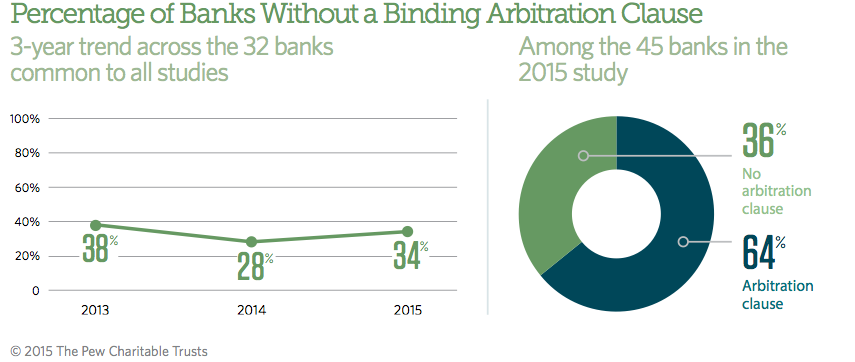

Overall, the study finds that the percentage of banks requiring customers to waive their rights to a jury trial have declined, with 34% requiring the clauses in 2015, compared to 38% in 2013.

Additionally, some banks with arbitration clauses include an opt-out provision that gives customers the opportunity to retain their legal rights, typically by writing to the bank within a certain number of days after either the account is opened or the arbitration clause is added to the agreement. The median number of days prior to the opt-out expiring is 45.

Nearly 59% of banks surveyed during the three-year period offered the opt-out provision, while 62% surveyed in 2015 offered the option.

In all, four banks analyzed in 2015 met Pew’s best practices standards for dispute resolution.

RECOMMENDATIONS

While Pew maintains that many bank practices have improved since last year’s analysis, the study authors say the three-year results show that policymakers cannot wait for financial institutions to voluntarily adopt comprehensive practices ensuring that checking accounts are safe and transparent.

Pew provided the following policy recommendations to make checking accounts safer for consumers:

• Summarize key information about terms and fees in a concise, uniform format.

• Provide account holders with clear, comprehensive terms and pricing information for all available overdraft options.

• Make overdraft penalty fees reasonable and proportional to the financial institution’s costs in providing the overdraft loan.

• Post deposits and withdrawals in a fully disclosed, objective, and neutral manner that does not maximize overdraft fees.

• Prohibit, in checking account agreements, pre-dispute mandatory binding arbitration clauses, which keep account holders from accessing courts to challenge unfair and deceptive practices or other legal violations.

Pew Releases Latest Ratings of Banks on Key Consumer Protections [Pew Charitable Trusts]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.