Report: Online Checking Accounts & Credit Unions Beat Traditional Banking

The merger madness of the ’90s and ’00s, followed by the collapses during the Great Recession, has left American consumers with a record-low number of federally insured banks to choose from. But that doesn’t mean there aren’t options, and a new report highlights the reasons you might want to consider moving your money.

The merger madness of the ’90s and ’00s, followed by the collapses during the Great Recession, has left American consumers with a record-low number of federally insured banks to choose from. But that doesn’t mean there aren’t options, and a new report highlights the reasons you might want to consider moving your money.

For its latest Banking Landscape Report, WalletHub researchers looked at the fees and features of around 2,000 different checking and savings accounts — both branch-based and online — and found that consumers looking for accounts with the lowest fees and the most features may benefit from going online or looking at a credit union.

ONLINE OR NOT ONLINE?

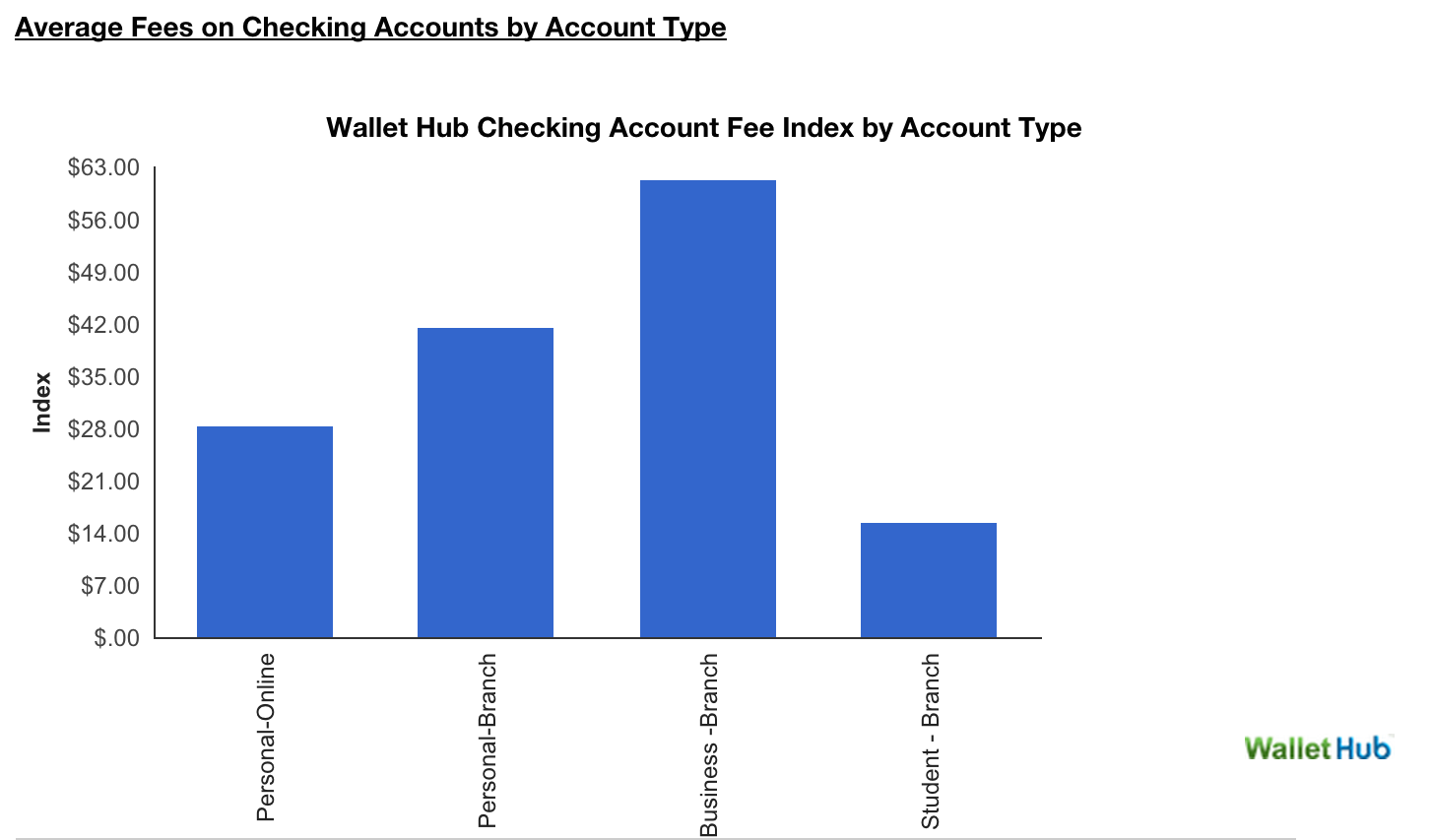

According to the study, the average monthly fee for an online checking account is $3.91, more than two dollars below the average of $5.96 for an account through a bank branch. Additionally, the average minimum balance required to waive these fees was lower online, $2,367 compared to $3,855.

Since many online banks have few or no bank-specific ATMs, it’s not surprising that the fee for non-bank ATM fees is also lower, averaging $1 while branch-based accounts average $1.75.

When it comes to savings accounts, online bank accounts have a higher average interest rate than other type of accounts. According to the report, an online savings account will earn an average of .61% on balances of $1,000. Compare that to the .12% average for branch bank savings accounts.

One hitch with an online savings account might come from the higher average balance to open one online. WalletHub figures an average of $2,837 is needed to open an online savings or money market account, compared with $967 for opening one of these accounts at a branch. You’ll also need to maintain a higher balance to avoid monthly fees, with averages of $2,333 for online and $1,640 for branch banks.

That said, nearly 1-in-4 (22.37%) of online accounts have a $0 minimum, while only 12.33% of branch banks offer savings accounts with no minimum to start. And 85% of online savings accounts have no monthly fee.

LOOK FOR THE (CREDIT) UNION LABEL?

With the disappearance of free checking, and their increased use of fees, many of the larger national banks seem to be doing everything they can to drive off most customers with their quaint little checking accounts. The WalletHub report shows that there may be better options out there.

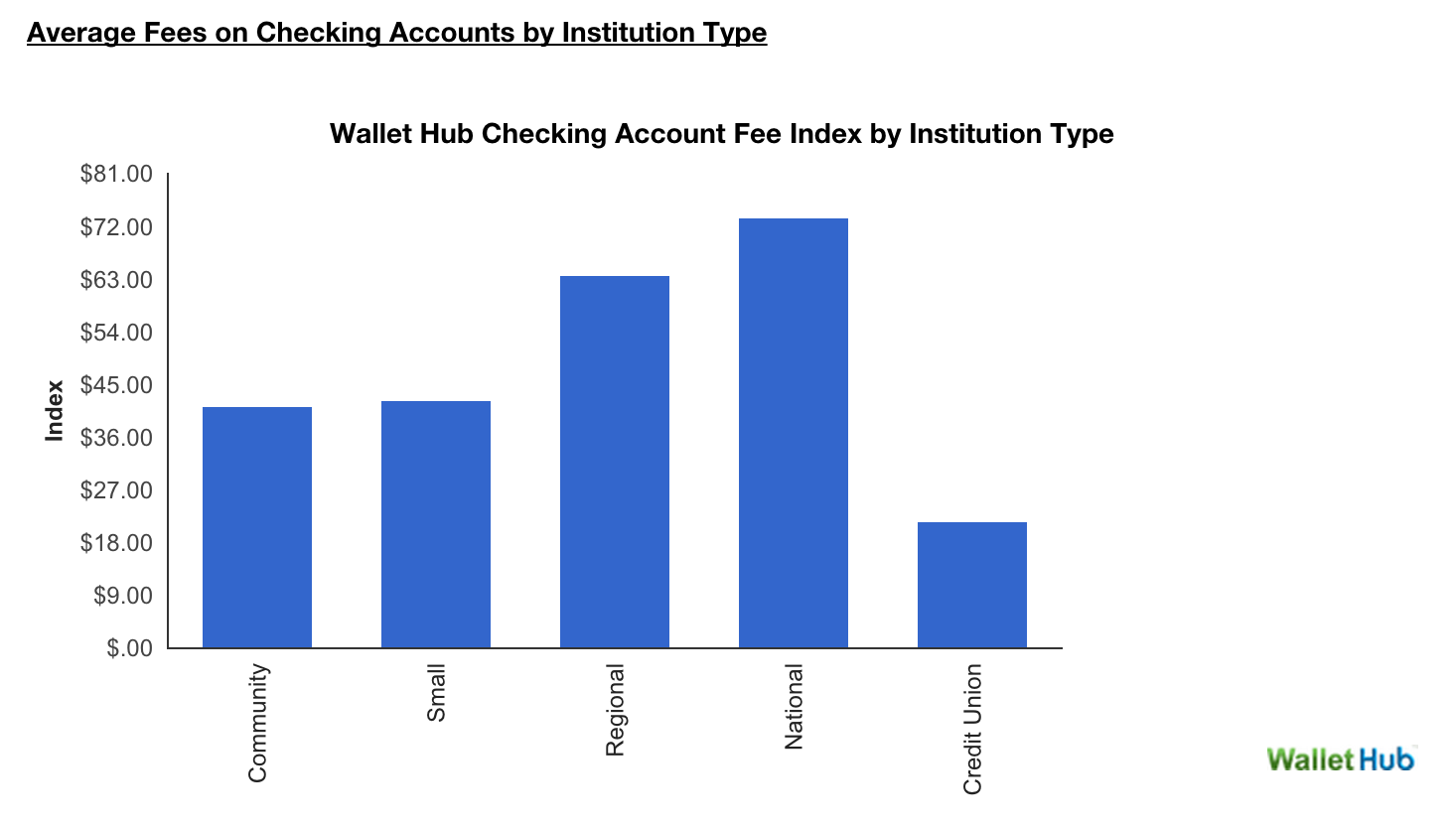

The average national bank charges $14.87 in monthly fees or requires you to have an average of $5,747 in your account to avoid that fee. Regional banks are slightly better at $10.38 in fees or a balance of $3,502. And things get manageable with small banks ($6.97 or $3,410) and community banks ($5.88 or $2,834) but nothing compares to the credit union average of $1.87 in fees.

Where the credit union might hit you is the average balance requirement of $11,500 (at credit unions with such a requirement); much higher than many consumers will have on hand at any given time. But if you’re not going to make your minimum balance requirement regardless, perhaps going with the lowest fee is the best option.

Additionally, 73% of credit union checking accounts have no minimum balance requirement and no monthly fee. Compare that to only 3.57% of accounts at national banks. You do stand a decent chance of finding a no-fee account at small and community banks (34.88% and 36.17%, respectfully), if a credit union isn’t for you.

Credit Unions, on average, also offer the best deals on interest-earning checking accounts. With a $1,000 minimum balance, the .51% interest rate you could get from a credit union is nearly double the next best average (.27% from community banks), and better than many savings accounts you’ll find at a traditional bank.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.