Wells Fargo Closes My Account After $32,000 Fraud, Allows Bogus Payment To Go Through On New Account

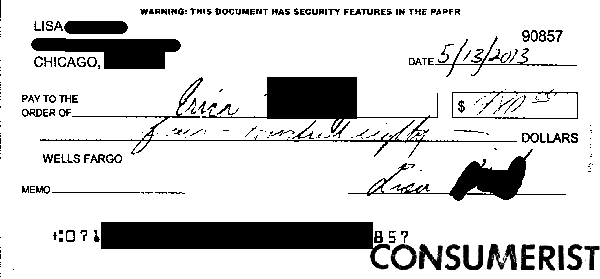

One of 30 fake checks written to Lisa’s account.

This is what happened to Consumerist reader Lisa, who recently received a call from a Chase bank because someone there believed a newly deposited check was a fake.

It was. Then Lisa looked at her Wells Fargo bank statement and found that in a matter of a couple days, a total of $32,526.27 had been drained from her account, putting her more than $30,000 into overdraft.

The Wells website had scans of the 30 scammy checks, which Lisa had obviously not written. The checks were fakes that had been created using her name and account number, but Lisa knew these weren’t stolen out of her checkbook because her partner’s name was not on the address information.

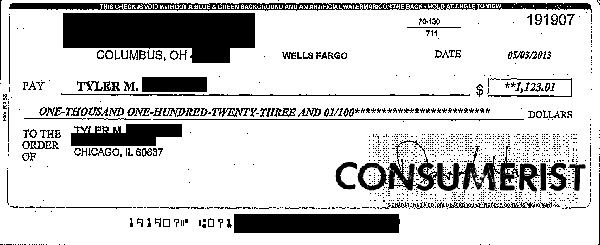

Even more curious were several checks that were written on her account number, but had the name of a home healthcare company in Ohio (Lisa is in Illinois) and appeared to be paychecks from that company, written to the same people in Chicago that cashed the other fraudulent checks:

So obviously Lisa called Wells Fargo to see what in the world was going on.

“They suggested that I close that account and open a new one, and that they could simply transfer the balance over,” she tells Consumerist. “Which seemed pretty nice of them. Until I found out that at Wells, once they close an account, you can never again have access to that account’s history. They forgot to mention that.”

After a few days, the bank did credit Lisa’s account for all 30 of the bogus checks, and it looked like everything would be okay. But that same day that she finally had access to her money, she looked online at her new checking account and found a $180.33 e-check payment to Sprint for a customer who is not her.

“I don’t have an account with Sprint,” writes Lisa, saying she’s never even heard of the person whose name was on that payment. “Once again, they debited my account without noticing, somehow, that the debit request was coming from a totally different name than the one on the account.

“What do these people do?” she asks. “I mean, if I have the date wrong, they make me correct it and initial the correction, but if someone puts in a clearly forged check, they just pass it through like nothing happened? Some of them aren’t even endorsed. Some of them have scratched and fixed dates with no initialing.”

And so we got in touch with Wells Fargo to find out what was going on. How could someone continue making bogus charges on a completely new account?

“We make every effort to investigate each claim and make right by our customers,” a rep for the bank tells Consumerist. “It is general practice to close accounts which have fraud committed against them and set up new accounts. Unfortunately, from time to time, an undetected fraudulent check may post against a new account if it was already going through processing. We try to avoid returning checks to ensure customers have a positive experience. We apologize if that was not the case.”

In the end, Wells got rid of the $180 charge to Sprint and Lisa has not noticed any subsequent questionable activity on her account. She says the bank is also providing free ID-theft monitoring for her account to help prevent this kind of huge error from happening in the future.

As for the Ohio company whose name was on the fake paychecks, it claims to be just as much a victim as Lisa. A rep for the company tells Consumerist that it also had bad checks written on its account by scammers in Chicago and that it is working with authorities.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.