No Surprise Here: Credit Reports Created With Your Online Information Are Mostly Inaccurate

(NCLC)

More than 64 million Americans are cut off from access to traditional banking because they lack credit history. To better serve these unbanked consumers financial institutions are relying on the promises of big data brokers to accurately determine the creditworthiness of consumers. But is the new method a reliable way to provide affordable access to credit? Not really, a new report by the National Consumer Law Center points out.

The NCLC’s new report “Big Data: A Big Disappointment for Scoring Consumer Creditworthiness” [PDF] investigates the inaccuracies in the information provided by data brokers and reviews the trustworthiness of products using big data analysis.

Big data is the use of information culled from Internet searches, social media and mobile apps to determine a consumers’ creditworthiness. Big data promises to make better predictive algorithms that in could in turn make better products available to the underbanked.

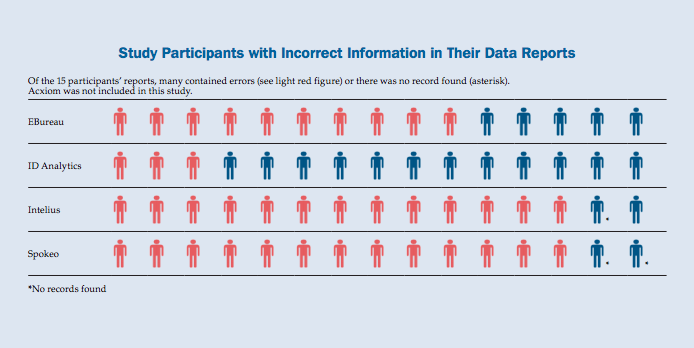

Fifteen volunteers, all NCLC employees, attempted to retrieve their information from four data brokers: eBureau, ID Analytics, Intelius, and Spokeo for the investigation.

Each volunteer found their reports to be filled with inaccuracies and incomplete information including wrong email addresses and poorly estimated income.

Seven of the 15 consumer reports generated by eBureau, a company that touts advanced models, contained errors in estimated income. The reports nearly doubled the salary of one participant and halved the salary of another. Additionally, 11 of the 15 reports incorrectly stated the consumer’s education level.

Reports purchased from Intelius and Spokeo had the most inaccuracies. The most common inaccuracies included wrong addresses, added or omitted family members and added or omitted social media accounts.

The reports from eBureau, and ID Analytics were found to contain very little information.

Big data reports were found to contain a number of inaccuracies.

“Proponents of big data underwriting argue that by using a constellation of factors to price credit, the cost of credit will be reduced for low-income borrowers, thus enabling lenders to provide lower-cost small loans as alternatives to payday loans,” the NCLC notes in the report.

The NCLC evaluated seven loan products that are based on big data underwriting. Six of the products are marketed as payday loan alternatives, including RISE Credit.

The evaluation found that while some of the features are “less bad” than those of traditional payday loans, the products fail to meet requirements to be considered genuine, better alternatives, the NCLC report concludes.

When the NCLC delved deeper into big data brokers they found the companies could be considered consumer reporting agencies and subject to the Fair Credit Reporting Act.

The FRCA imposes substantial duties on a CRA, most importantly dealing with accuracy, disclosure and the right to dispute items on reports. The NCLC concludes that it’s unlikely that big data brokers could meet FCRA requirements.

While big data does offer alternative methods to determine an unbanked consumers’ creditworthiness it falls apart when put to the test, NCLC reports.

“Unfortunately, our analysis concludes that big data does not live up to its big promises,” NCLC notes. “A review of the big data underwriting systems and the small consumer loans that use them leads us to believe that big data is a big disappointment. More and more, consumers are leading robust lives online. However, as data about consumers proliferates, so does bad data.”

To better ensure that big data is used correctly, the NCLC developed several federal policy recommendations:

- The Federal Trade Commission (FTC) should continue to study big data brokers and credit scores testing for potential discriminatory impact, compliance with dis- closure requirements, accuracy, and the predictiveness of the algorithms.

- The FTC and the Consumer Financial Protection Bureau (CFPB) should examine big data brokers for legal compliance with FCRA and Equal Credit Opportunity Act (ECOA).

- The CFPB should create a mandatory registry for consumer reporting agencies so that consumers can know who has their data.

- The CFPB, in coordination with the FTC, should create regulations based upon the FTC’s research that:

Define reasonable procedures for ensuring accuracy when using big data;

Specify a mechanism so that consumers can do a meaningful review of their files including all data points that can be linked to that consumer (not just those that identify the consumer explicitly); and

Define reasonable procedures for disputing the accuracy of information. - The CFPB should require all of the financial products it regulates to meet Regulation B’s requirements for credit scoring models.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.