Senator Calls On Regulators To Take Closer Look At Rent-To-Own Stores

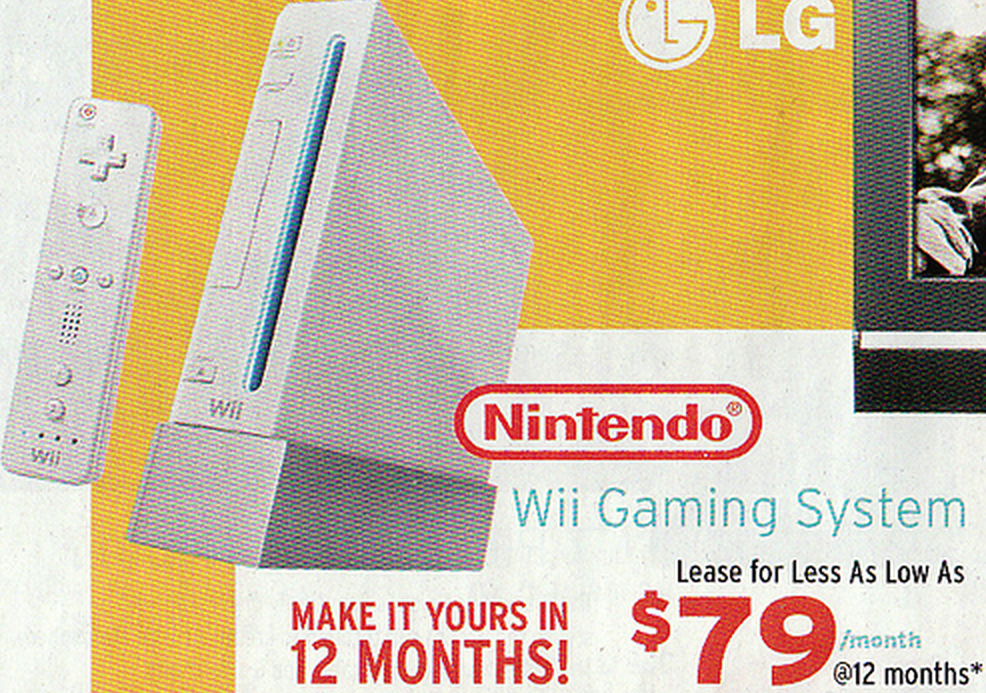

From a classic Consumerist post about a rent-to-own store selling a $250 Nintendo Wii for just $79/month… for 12 months, meaning you’d pay $948 by the time you’re done. (Photo: Blitzcat)

Earlier today, in a letter shown to Consumerist, Sen. Bob Casey of Pennsylvania wrote to Federal Trade Commission Chair Edith Ramirez and Consumer Financial Protection Bureau Director Richard Cordray to explain his concerns about rent-to-own operations.

The Senator points to the industry’s own stats that claim a growth in RTO customers of 2.7 million in 2004 to 4.8 million in 2012, with more than 75% of these consumers having annual household incomes below $36,000.

The letter also cites a 2013 FDIC survey which found that unbanked and underbanked Americans are three times more likely than others to shop at RTO stores.

“RTO deals can be financially sensible for short-term rentals of certain items,” acknowledges Casey. “However, if customers make the full number of payments required to own an item, the total expense is far higher than if they had financed the purchase through a consumer loan.”

In 2011, our colleagues at Consumer Reports looked at financing plans at RTO stores and found that customers were paying in excess of 300% interest for certain items.

Casey points out that these interest rates are several times those of even high-interest credit cards, and notes that if these RTO deals were classified as loans, “they would also violate most states’ usury laws.”

Some RTO operations have also been caught marking up the retail price of items they sell so as to make the financing more attractive. For example, in the Consumer Reports survey, one Ohio RTO store listed a TV with a $349 MSRP at $599.

RTO stores can also use this method of financing to get around caps on interest rates for loans made to active-duty servicemembers. Like the Virginia-based chain of stores that actively markets its financing to servicemembers, and where a $650 laptop could ultimately cost the customer thousands of dollars.

“I am concerned about the threat that the continued growth of the RTO market poses to the financial stability of millions of Americans,” writes Casey. “It is essential that customers entering into RTO deals are aware of the risks involved.”

The Senator acknowledges that the RTO market straddles the line between offering a financial product and selling retail goods, making it difficult to put it under one regulatory umbrella, but believes that the FTC and CFPB together are “well-placed to provide consumers with adequate information” about the risks associated with RTO, and to decide whether the industry merits further scrutiny.

“What can each of your agencies do to better inform consumers about the risks posed by RTOs?” Casey asks Ramirez and Cordray. “What, if any, additional tools or authorities would your agencies need in order to adequately protect consumers from these risks?”

Casey also wants to know if there are any legislative actions that could help to ensure that users of all alternative financial products — not just RTOs — receive the same level of consumer protection afforded to borrowers of bank loans.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.