1-In-3 Americans Still Feeling The Sting Of Recession

While many Americans are now doing better than they were during the Great Recession, those dark days took such a toll on many consumers’ savings that some people who are currently doing well enough to pay the bills and enjoy a decent living aren’t able to make necessary longterm investments, like buying a new home or saving for retirement.

While many Americans are now doing better than they were during the Great Recession, those dark days took such a toll on many consumers’ savings that some people who are currently doing well enough to pay the bills and enjoy a decent living aren’t able to make necessary longterm investments, like buying a new home or saving for retirement.

This is according to newly released survey results [PDF] from the Federal Reserve.

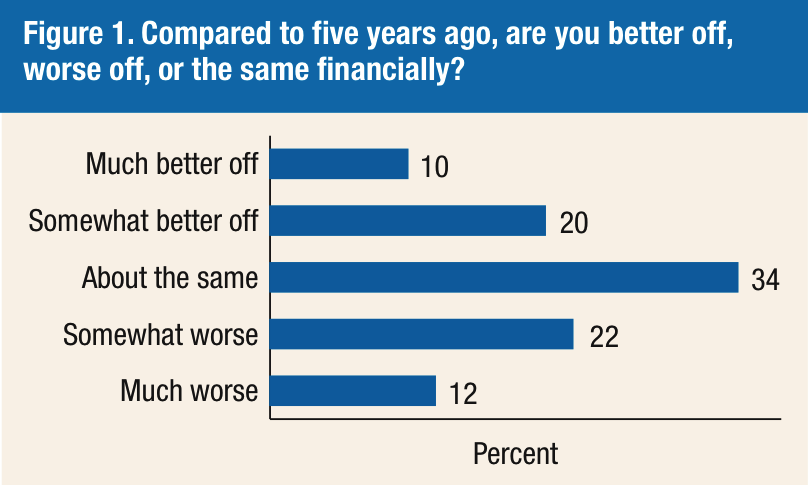

As you can see from the above chart, 34% of those surveyed said they are in the same financial situation as they were five years earlier. Another 30% are at least somewhat better than they were, but then there is the 34% who claim to be worse off now.

These numbers seem to match up with another question asked by Fed surveyors, with 23% of respondents saying they were “living comfortably,” and 37% reporting they were “doing okay,” adding up to 60% of Americans feeling they were in a stable place. But 25% say they are “just getting by” financially, and 13% admit they are “finding it difficult to get by.”

Even with the majority of Americans feeling they are in an okay place with their finances, a large number of them now lack savings or are unable to make necessary investments.

According to the survey, 42% of Americans delayed a major purchase or expense directly due to the recession, and 18% put off what they considered to be a major life decision.

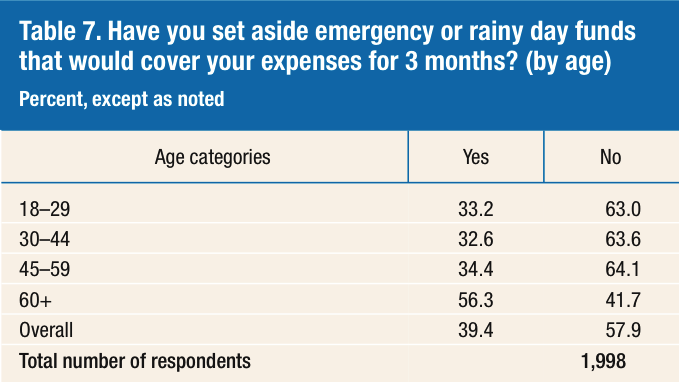

Nearly 60% of all respondents lack a “rainy day” fund that could cover three months of expenses if needed. The percentage of unprepared consumers actually increases with age (up until age 60 and above).

Additionally, only about half of the people surveyed by the Fed can cover a hypothetical emergency expense costing $400 without selling something or borrowing money.

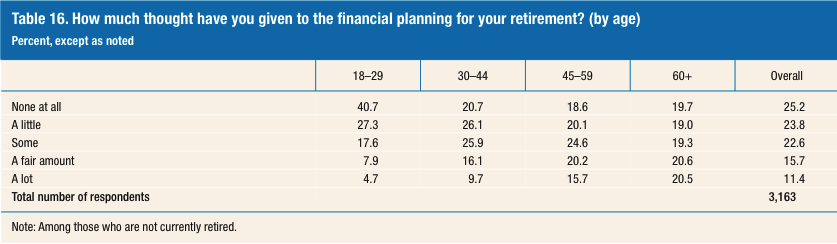

It’s probably not a shock that 41% of people between 18-29 aren’t thinking about planning their retirement finances, but nearly 1-in-5 people between the ages of 45-59 are giving no thought at all to saving for retirement. When you add in the 20% who are only giving it a little thought, that means that 40% of people approaching retirement age are, at best, giving it only cursory consideration.

In terms of the housing market, there is tempered optimism among consumers, with most current homeowners believing that the value of their property will increase in the coming year. However, 45% of homeowners still believe their house is worth less than it was in 2008 when the housing market collapsed, so for these consumers the hoped-for value increase is more about getting back to a previous level.

The longterm implications of the recession on the housing market can be seen in renters’ response to the survey questions.

Most renters would rather own a home, especially in the younger age groups of 18-29 and 30-44, where only 14% of respondents say they prefer renting to owning a home.

However, these same groups say they can’t buy a home. In fact, nearly half of all renters say the biggest roadblock to buying a home is the inability to pay the hefty down-payment. Given that many markets only require 5-10% of a home’s value (plus mortgage insurance), this seems to indicate a serious lack of savings.

Interestingly, the age group that most frequently cited an inability to qualify for a mortgage as an impediment to homeownership are those renters between 45-59, perhaps indicating that this group includes a number of people whose creditworthiness was damaged during the recession.

“In general, it appears that the majority of the population is making progress in recovering from any effects the financial crisis had on their personal finances and household’s financial well-being,” concludes the survey. “However, despite these overall reasons for optimism about the economic conditions of U.S. households, the findings in this survey highlight that economic challenges remain for a significant portion of the population.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.