Report: Most Consumers Don’t Care If The Post Office Offers Financial Services

(Liz West)

At first glance it wouldn’t appear that the United States Postal Service and banks have much in common. But that might soon come to an end if an idea to expand banking services to local post office branches in an attempt to meet the needs of the underbanked.

But would consumers really be open to banking at the same place they send off letters to grandma? According to a new survey report from Pew Charitable Trusts a majority of consumers don’t really care.

The Postal Banking Consumer Survey [PDF] asked more than 1,600 consumers, many of whom do not have access to traditional banking services, whether or not USPS should enter the banking arena.

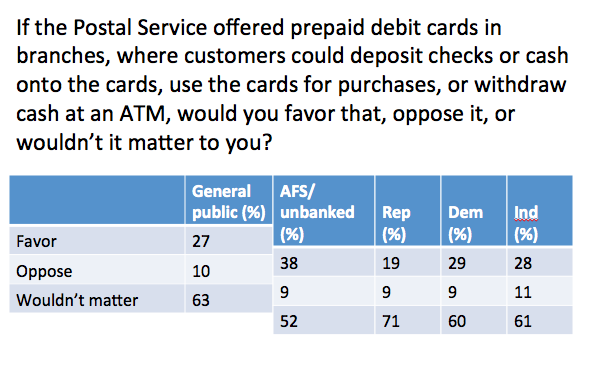

Most consumers surveyed by Pew did not have an opinion on whether USPS should offer banking services.

Most consumers, about 63%, reported that the addition of services, such as bill paying, check cashing, and small-dollar loans, would not matter to them.

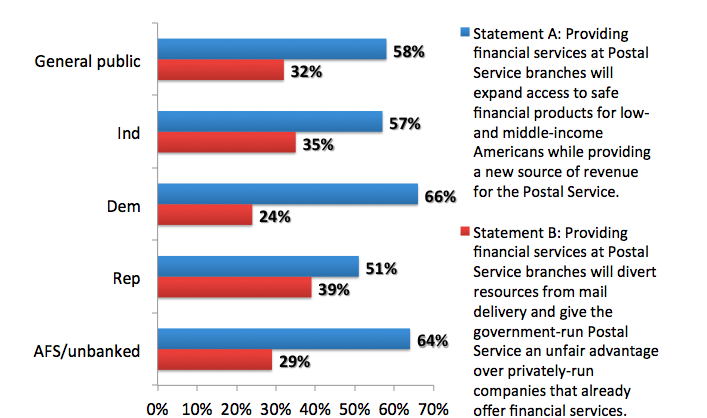

However, a majority, about 58%, of consumers support the argument that providing financial services at USPS branches would expand access to safe financial products for low- and middle-income Americans while providing a new sources of revenue for the Postal Service.

Nearly 64% of consumers who identify as using alternative financial services believe the expansion of safe financial services would be beneficial to both consumers and the postal service.

Conversely, only 32% of those surveyed said they believe that providing financial services at Postal Service branches would divert resources from mail delivery and give the government-run Postal Service an unfair advantage over privately-run companies that already offer financial services.

“There is a market here but it’s limited,” Alex Horowitz, research officer for Pew Charitable Trusts, says. “When we look at people who already are using alternative services it changes. There is quite a bit of interest for lower-cost services among those who already use alternative services.”

Nearly 78% of consumers said they would be unlikely to go to the post office to deposit a check on a prepaid card, 74% said they were unlikely to pay a bill through an expanded postal service. Likewise, 78% were unlikely to purchase prepaid cards and 83% were unlikely to take out small-dollar loans from the post office.

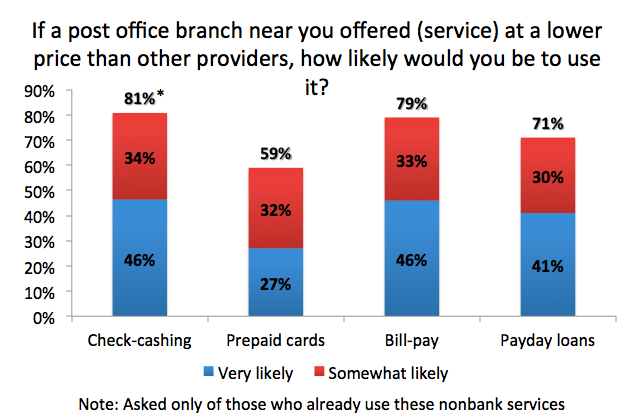

Consumers who use alternative banking services say they would be likely to use low-cost services though USPS.

Consumers who currently use alternative financial services were more likely to use lower-cost services though their local post office branch.

Nearly 46% would use check-cashing, 27% would purchase prepaid cards, 46% would use bill-pay services and 41% would consider payday loans through the postal service.

While it appears the majority of consumers don’t feel they would be impacted by expanded financial services through the postal service, those who did have an opinion were mostly supportive.

The idea of expanding the postal service’s offerings began in January after the Post Office Inspector General released a white paper suggesting the additional offerings could boost the revenue of the organization while meeting the needs of the underbanked.

“Millions of Americans do not have a bank account, or use costly services like payday loans and check cashing exchanges just to make ends meet,” reads the report. “The entire underserved population comprises more than a quarter of all U.S. households — some 68 million adults. They are an economically diverse mix of working and middle class families, poor and unemployed people hurt by the recent economic crisis, young people, immigrants, and others who are trying to make it paycheck to paycheck. Together, they represent a huge market. In 2012, they spent about $89 billion just on interest and fees for alternative financial services.”

Soon after the report was released, Sen. Elizabeth Warren voice her support for the idea that the USPS could use its infrastructure to extend basic banking needs, such as debit cards and small-dollar loans, to those who are ignored by the banking industry.

“With post offices and postal workers already on the ground, USPS could partner with banks to make a critical difference for millions of Americans who don’t have basic banking services because there are almost no banks or bank branches in their neighborhoods,” she wrote at the time.

Although consumers’ feelings on expanding financial service through the USPS were only lukewarm, a recent survey from Accenture found that people were interested in banking outside of traditional banks. Granted a majority of their first choices included banking with Google, Amazon, Apple, Costco and other companies they have frequent interactions with.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.