CFPB: ACE Cash Express Must Pay $10M For Pushing Borrowers Into Payday Loan Cycle Of Debt

The Consumer Financial Protection Bureau announced Thursday that it was seeking an enforcement action against ACE Cash Express, one of the largest payday lenders in the United States, for allegedly engaging in illegal debt collection practices in order to push consumers into taking out additional loans they could not afford.

Texas-based ACE will provide $5 million in refunds to consumers on top of paying a $5 million penalty for the alleged violations.

ACE, which currently operates online and through 1,500 retail storefronts in 36 states, offers payday loans, check-cashing services, title loans, installment loans and other financial products.

Regulators say they found that ACE and its third-party collection operators used illegal tactics such as harassment and false threats of lawsuits and criminal prosecution to pressure consumers to take out additional loans.

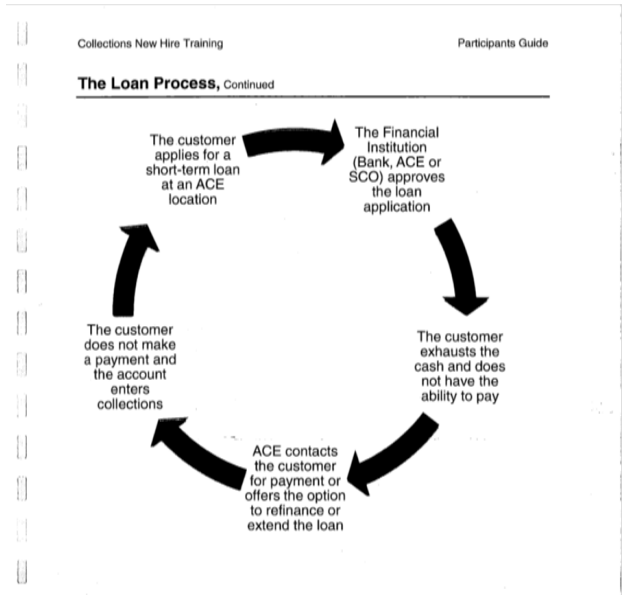

A diagram from ACE’s 2011 training manual illustrates the cycle of debt for payday borrowers.

According to the above graphic, consumers begin by applying to ACE for a loan, which ACE approves. Next, if the consumer “exhausts the case and does not have the ability to pay,” ACE “contacts the customer for payment or offers the option to refinance or extend the loan.” Then, when the consumer “does not make a payment and the account enters collectors,” the cycle starts all over again – with the formerly overdue borrower applying for another payday loan.

While the illustration provides a disturbing picture of practices used in the payday lending industry, officials with ACE say in a news release [PDF] Thursday that the company has policies in place to prevent delinquent borrowers from taking out new loans:

“A customer with a delinquent account is not allowed to take out another loan with ACE until the previous loan is paid off. Furthermore, ACE does not charge any additional fees or interest on accounts in collections and offers a payment plan option where, once a year, customers may elect a four-payment interest-free payment plan to pay off an outstanding loan balance.”

Payday loans are meant to get consumers out of emergency financial situations, but more and more consumers use the loans to make ends meet on a regular basis. This trend has become worrisome for regulators and consumer advocacy groups.

Back in March, the CFPB released a study that uncovered four out of five payday loans were rolled over or renewed every 14 days by borrowers who end up paying more in fees than the amount of their original loan.

The CFPB found that by renewing or rolling over loans the average monthly borrower is likely to stay in debt for 11 months or longer. More than 80% of payday loans are rolled over or renewed within two weeks regardless of state restrictions.

In addition to providing refunds and paying a penalty, ACE’s collectors are banned from using illegal debt collection tactics and refrain from pressuring consumers into cycles of debt.

Following the CFPB announcement Thursday, officials with ACE say in a news release that an outside, independent expert reviewed a “statistically significant, random sample of ACE collection calls.”

According to ACE, the review “indicated that more than 96 percent of ACE’s calls during the review period met relevant collections standards.”

The company also states that over the past two years it has cooperated fully with the CFPB to implement compliance changes and enhancements and responding for documents and information.

CFPB Takes Action Against ACE Cash Express for Pushing Payday Borrowers Into Cycle of Debt [Consumer Financial Protection Bureau]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.