Report: Older Americans Facing Significant Increases In Mortgage Debt Load

A snapshot report [PDF] released by the Consumer Financial Protection Bureau highlights the mortgage debt challenges faced by older Americans, including an increase in debt, less affordable housing options and a greater risk of foreclosure.

While older Americans have the highest rate of homeownership of all consumers – 80 percent of the 41 million Americans 65 and older own their home – the percentage of those consumers carrying mortgage debt has grown steadily over the last decade.

Nearly 30% of seniors age 65 and older carry mortgage debt – representing an 8% increase in the last 10 years. Seniors aged 75 and older with mortgage debt nearly doubled during that same time period.

In the last 10 years, the median mortgage debt for seniors increased by 82% from $43,000 to $79,000, while many homeowners have accrued less home equity.

More than 4.4 million retired homeowners with mortgage debt spend 30% of or more of their household income on housing related costs, putting themselves at greater risk for financial harm, the CFPB reports.

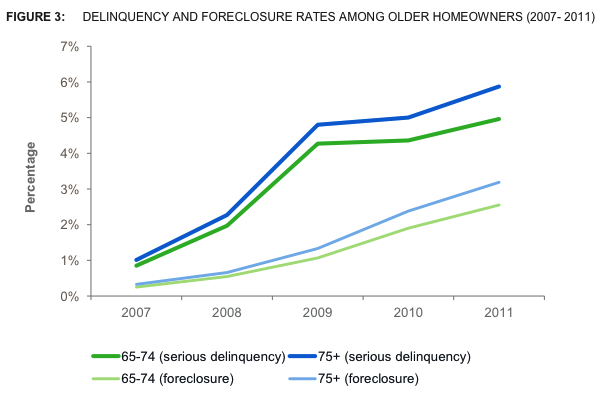

Because of these issues the number of seniors facing delinquency and foreclosure has increased. From 2007 to 2011, the number of homeowners ages 65 to 74 who were seriously delinquent in paying their mortgage – meaning they were more than 90 days late or in foreclosure – increased from 0.85% to 4.96%. For homeowners over 75, the increase was from 1.01% to 5.87%.

The CFPB reports older consumers have greater difficulty recovering from foreclosure than their younger counterparts due to their increased incidences of health problems, cognitive impairment, and difficulties returning to the work force.

The report attributes the increases to the refinancing boom of the 2000s and a general trends to buy homes later in life, provide smaller down payments and borrow against the equity of homes to cover other expenses.

To assist older consumers facing issues pertaining to mortgage debt the CFPB suggests they consider these issues while managing mortgage debt in retirement:

Mortgage pay-off date: Because mortgage debt can be a consumer’s most costly monthly expense, consumers should carefully consider the burden of mortgage payments while living on a fixed, retirement income.

Home equity: Dipping into the equity already built-in a home can carry risks. The money put into a home can be an important asset and security, especially considering Americans are living longer and often face large health expenses in later life. Older consumers should carefully consider their options before taking out a home equity loan or refinancing.

Retirement income and expenses: Generally, people have less income when they retire. Consumers should know their retirement income and expenses, especially if they are retiring with a mortgage.

“A home can be a place of security for older Americans in their retirement years – a roof over their heads as well as a valuable asset,” CFPB Director Richard Cordray said in a news release. “But as more seniors carry significant mortgages into retirement, they put themselves at risk of losing their nest eggs and their homes.”

Consumer Financial Protection Bureau Spotlights Mortgage Debt Challenges Faced By Older Americans [Consumer Financial Protection Bureau]

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.