GE’s CareCredit To Refund $34.1 Million To Misled Consumers

CareCredit is a medical financing service operated by the folks at GE Capital. For almost all of its 4 million customers, CareCredit is a deferred interest loan, meaning cardholders who don’t pay off their balances in full by the end of the initial promotional period are hit with all of the interest that had been accruing during those months. That would be fine (and is quite common in retail credit cards), if the company hadn’t misled consumers into thinking CareCredit was an entirely interest-free product.

CareCredit is a medical financing service operated by the folks at GE Capital. For almost all of its 4 million customers, CareCredit is a deferred interest loan, meaning cardholders who don’t pay off their balances in full by the end of the initial promotional period are hit with all of the interest that had been accruing during those months. That would be fine (and is quite common in retail credit cards), if the company hadn’t misled consumers into thinking CareCredit was an entirely interest-free product.

Yesterday, the Consumer Financial Protection Bureau ordered [PDF] GE Capital and CareCredit to refund up to $34.1 million to customers who were not given the full story about the cost of the program.

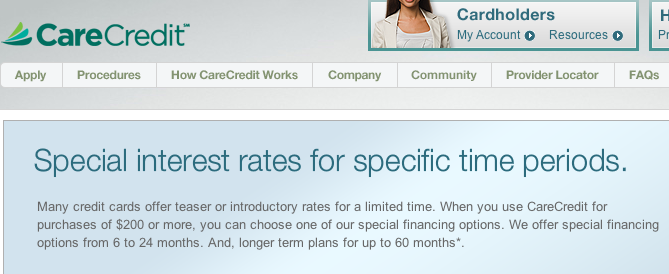

In thousands of medical and dental offices around the country, CareCredit advertised its “no interest if paid in full” plan, offering promotional 0% interest periods of anywhere from 6 to 24 months. But if the bill isn’t paid in full by the end of that period, the cardholder is slammed with an interest rate of around 26%, about twice what most people pay on regular credit cards.

The CFPB’s problem isn’t with the interest rate, but with how CareCredit marketed itself to consumers. The agency alleges that since 2009, the company has been providing consumers inadequate explanations of its credit terms, leading many CareCredit customers to become buried until mountains of unexpected interest charges, penalties, and fees.

NON-EXPERT ADVICE

Through its investigation into CareCredit, the CFPB found that some of the medical and dental service providers who pushed the program for GE were complicit in the deception by failing to provide adequate explanation of the terms of the deferred-interest loan. The agency says that CareCredit took a hands-off approach to enrollment process, leaving it up to the service providers who may have been ill-prepared to clarify the program.

“CareCredit’s limited involvement during the enrollment process and lack of oversight and monitoring allowed this deception to continue,” writes the CFPB. “Many staff members… who were responsible for explaining the CareCredit agreement to borrowers, had received little or no training by CareCredit, and relied only on pamphlets. In interviews with CFPB investigators, some providers admitted that they were themselves confused by the deferred-interest card.”

AN ORAL TRADITION

So first you have a situation where the people selling the product don’t necessarily know what it is they’re selling. Then you make it worse by failing to provide these customers with written copies of CareCredit agreement. Thus, these borrowers have only on the oral explanations from the person who was not trained to explain the product to begin with.

PAYING THE PENALTY

And so the CFPB has hit GE and CareCredit with an enforcement action that requires the companies to create a $34.1 million reimbursement fund, that will allow CareCredit customers to make claims that will then be reviewed independently.

The order also requires that CareCredit enhance its disclosures provided during the application process and on billing statements. These new and improved disclosures will include clearer descriptions of the deferred-interest loan. In addition to the explanation given at the point of signing the agreement, all borrowers will get a call from an actual CareCredit employee within 72 hours, and all loans of $1,000 or more will require the involvement of a CareCredit rep, rather than through the doctor or dentist’s office.

Furthermore, borrowers will subsequently receive a warning notification to alert them when the end of the promotional period approaches.

“Medical debt is already a big problem for many Americans. Poor credit card transparency should not be making the problem even worse,” said CFPB Director Richard Cordray. “Deferred-interest products can be risky for consumers in the best of circumstances, and today’s action ensures that CareCredit will no longer profit from consumer confusion. The Bureau will not tolerate financial companies that take advantage of patients and their loved ones.”

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.