Bank Of America Accused Of Neglecting Foreclosures In Non-White Neighborhoods

Two BofA-owned properties in the Oakland area. The one on the left is in a predominantly African-American and Hispanic neighborhood, while the one on the right is from a predominantly white area.

The NFHA recently amended its complaint [PDF] to the Dept. of Housing and Urban Development, by adding additional cities, along with photographic and diagrammatic evidence to bolster its case.

The complaint now claims bad behavior on the bank’s part in 20 different cities — Oakland; Grand Rapids, MI; Atlanta; Dayton, OH; Miami; Dallas; Phoenix; Washington, DC; Orlando; Charleston, SC; Chicago; Milwaukee; Indianapolis; Denver; Memphis; Las Vegas; Tucson; Philadelphia; Toledo, OH; and Baltimore.

In evaluating whether or not a bank-owned property is being properly maintained, the NFHA looked at seven things:

1. Curb Appeal — Is there mail piling up, overgrown or dead grass/shrubbery, trash?

2. Structure — Are the doors and locks broken or removed? Is there damage or rot to the roof, walls, steps, or floors?

3. Signage & Occupancy — Is the “for sale” sign intact? Are there warnings against trespassers? Are people living in the property without authorization?

4. Painting & Siding — Is it damaged, chipped, covered in graffiti?

5. Gutters — Are they intact, damaged, hanging, clogged?

6. Water Damage — Has this resulted in any mold build-up?

7. Utilities — Have these connections been tampered with?

“In each of the metropolitan areas where Complainants evaluated a number of Bank of America REOs [real-estate owned properties] in communities of color and White communities, the properties in White communities were far more likely to have a small number of maintenance deficiencies or problems than REO properties in communities of color, while REO properties in communities of color were far more likely to have large numbers of such deficiencies or problems than those in

White communities,” reads the complaint.

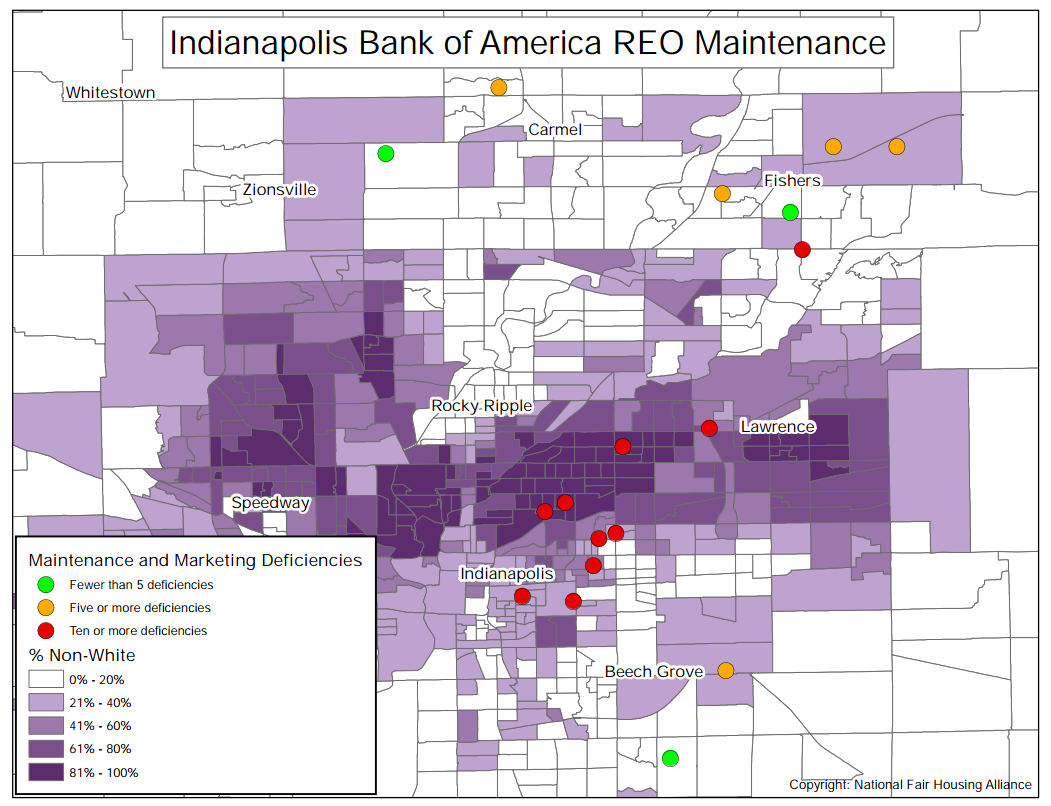

For example, here’s a map supplied by the NFHA of the Indianapolis area that it claims shows that foreclosed properties in predominantly white neighborhoods are being maintained with more care:

(Click to see full-size)

And here is a photographic comparison of two houses in the Indianapolis area. First, there is this BofA-owned home in a predominantly African-American neighborhood. According to the NFHA survey, it had 13 deficiencies:

Then there is the home that NFHA claims is in a predominantly white neighborhood, which only had five deficiencies:

“Bank of America has known about these problems for more than four years, yet, sadly, they have chosen a path that continues to harm the health of people living in these communities,” said Shanna L. Smith, President and CEO of the NFHA in a statement. “Bank of America’s conduct sends a message that it does not care about the viability of the neighborhoods or the health of the residents in communities of color.”

A rep for BofA tells MLive.com that this is all just a matter of these properties being caught in a transitional phase between the former owner and the bank.

“It’s not that we’re perfect, but when somebody brings a property to our attention that fell through the cracks for one reason or another, we’re doing everything we can to take immediate action,” says the bank rep.

Earlier this year, Wells Fargo reached a $38.5 million settlement in a similar discrimination case brought by the NFHA.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.