Bank Overdraft Policies Have Improved, But Not Enough To Protect Most Consumers

Over the years, banks across the country have modified their policies regarding overdraft fees to comply with federal regulations — including requiring consumers to opt-in to the costly protection. Despite this, account holders spend nearly $32 billion each year on the fees. And according to a new report, that likely won’t end anytime soon, as most large U.S. banks continue to charge high, sometimes exorbitant overdraft fees.

The Pew Charitable Trusts released two reports Tuesday highlighting the current state of large and small banks’ overdraft policies and how consumers could be better protected from the often costly fees.

According to the report “Consumers Need Protection From Excessive Overdraft Costs,” in 2015 U.S. banks with assets exceeding $1 billion reported bringing in $11.6 billion in overdraft and non-sufficient fee revenue.

The organization found that this revenue from service charges, including overdraft and insufficient fund fees, has more than doubled during the last three decades despite the company urging financial institutions to implement best practices that would decrease the costly fees imposed against customers.

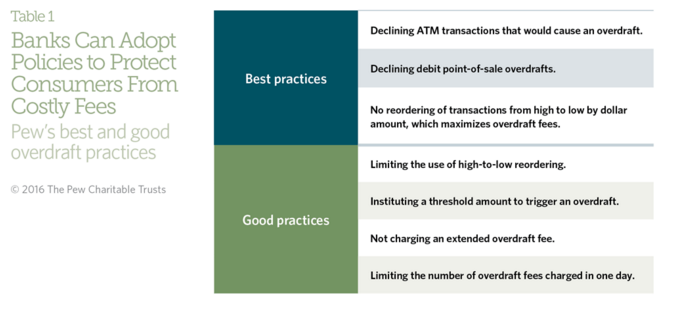

Back in 2013, Pew released a set of best practices, which are defined as those that are most effective in providing checking account holders with clear and concise disclosures about fees and terms; reducing the incidence of overdrafts; eliminating practices that maximize overdraft fees; and allowing consumers to choose the method by which they resolve a problem with their bank, rather than requiring pre-dispute binding arbitration.

While Pew notes that many large banks have implemented these practices, a significant portion have not.

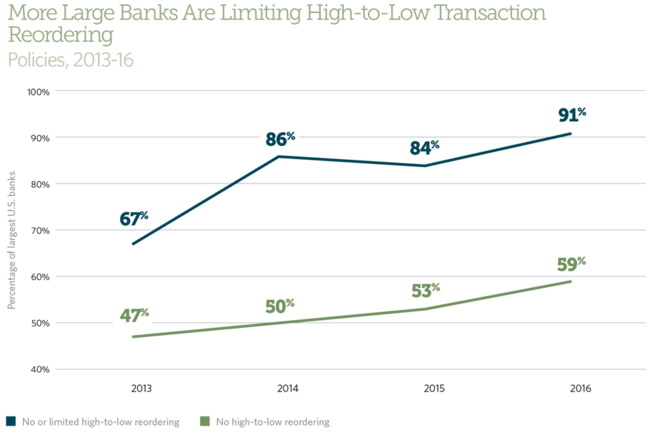

In an analysis of the 50 largest banks by deposit volume and revenue as reported to the Federal Deposition Insurance Corp., Pew found that nearly 40% of the financial institutions process transactions from largest to smallest by dollar amount, a process that can result in more overdrafts.

Additionally, 80% of the banks allow overdrafts on ATMs and debit point-of-sale transactions. This, despite Pew’s recommendation that banks can protect their customers from unexpected fees by simply declining these transactions at no cost to the consumer. In fact, it’s a practice Pew says most customers are in favor of: they would rather have a transaction declined than incur a $35 fee.

In a separate report — titled” How a Set of Small Banks Compares on Overdraft” — Pew examined the disclosures of 45 small banks, finding that the institutions often adhere to similar policies as their larger counterparts.

For example, the report found that many tend to offer fee-based overdraft programs with fees ranging from $28 to $36 per occurrence, which is just slightly lower than larger banks.

Additionally, the smaller banks often allow consumers to incur multiple fees per day. In fact, all 45 banks allowed customers to incur at least $90 in fees each day for any overdrafts the banks service under their programs.

The analysis found that only two banks disclosed that they reorder transactions from high to low by dollar amount, while the 43 remaining banks either don’t disclose policies or say they post transactions from low to high.

According to Pew, the findings from both reports “reinforce the need to end ‘unsafe, high-cost'” overdraft fee practices.

To do so, the organization says that banks should limit the size of overdraft fees; the frequency with which they can be incurred; or their overall cost.

“Consumers — especially those who are most financially vulnerable — need protections to help them avoid expensive overdraft fees and remain viable in the banking system,” Pew said in a statement.

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.