Could Equifax have suffered a second data breach following the massive hack exposing the personal information of more than 145.5 million consumers? It’s possible, according to a security researcher who claims to have found a second, separate security vulnerability within the company. [More]

equifax

IRS Has Second Thoughts About Giving $7.2M Fraud-Prevention Contract To Equifax

By 10.13.17

What does it take for the Internal Revenue Service to realize that maybe, just maybe, it picked the wrong company to award a $7.25 million fraud-prevention contract? It wasn’t enough that Equifax’s network was so poorly prepared for a hack that a months-long cyber attack compromised the sensitive information of more than 140 million Americans. And then that same company may have served up malware to consumers visiting its publicly available website. Whatever the reason, the IRS has finally begun to realize Equifax might just be absolutely terrible at its job. [More]

Equifax Takes Part Of Its Website Offline Over Concerns About Malware

By 10.12.17

Following a report that its consumer-facing website may have been serving up malware to visitors, Equifax — the credit bureau that seems intent on finding every way possible to ruin your day — has pulled some of its web pages offline. [More]

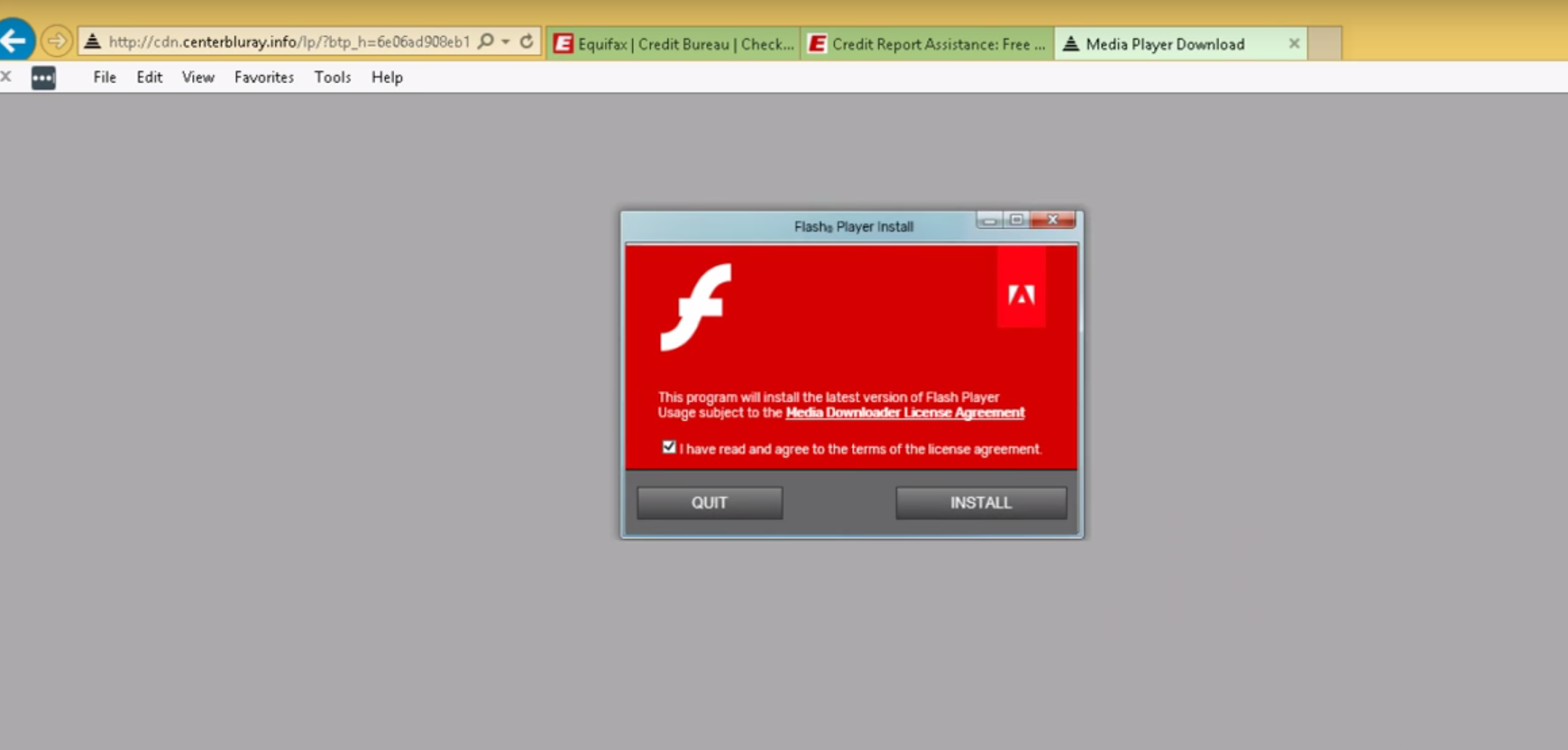

Equifax Website Reportedly Served Up Malware To Some Users

By 10.12.17

Update: Equifax has taken some pages temporarily offline following the report about malware. [More]

Equifax Security Failings Were Flagged By Wall Street Firm More Than A Year Ago

By 10.6.17

A company that supplies stock market indexes reportedly warned investors in August 2016 that Equifax, one of the nation’s three major credit bureaus, appeared to be ill-equipped to fight off a sophisticated cyber attack. Apparently Equifax didn’t get that warning; otherwise, hackers may have been prevented from accessing the sensitive financial information for more than 140 million Americans. [More]

Monopoly Guy’s Presence Dramatically Improves Senate Hearing

By 10.4.17

If you were probably watching this morning’s Senate hearing on the Equifax hack, you may have seen something out of the corner of your eye and asked, “Did I just see Rich Uncle Pennybags from Monopoly sitting behind the Equifax CEO?” Yes, yes you did. [More]

IRS Awards $7.25M Fraud-Prevention Contract To Equifax Despite Failure To Secure Consumers’ Data

By 10.4.17

This week, various members of Congress are verbally flogging Equifax over the recently revealed data breach that compromised the personal information of around 145 million people. Meanwhile, the folks down the road at the Internal Revenue Service apparently aren’t concerned about incompetence, awarding Equifax a multimillion-dollar contract for — sigh — fraud-prevention services. [More]

Equifax Says 2.5M More Customers Affected By Breach; Ex-CEO Apologizes To Congress

By 10.3.17

When 143 million people have already been affected by a massive data breach at one of the three major credit reporting agencies, what’s a few million more? That’s apparently the reality for Equifax, which upped its estimate of how many consumers were affected in the hack just hours before company executives were scheduled to discuss the incident with lawmakers. [More]

The Equifax Executive Who Oversaw Security Also Approved Last-Minute Stock Sales

By 10.2.17

Right before Equifax revealed that it had failed to secure the information of some 143 million Americans, some company executives sold off nearly $2 million in Equifax stock — a move that is currently under investigation. According to a new report, the Equifax executive who approved those stock sales is also the exec in charge of the company’s cybersecurity. [More]

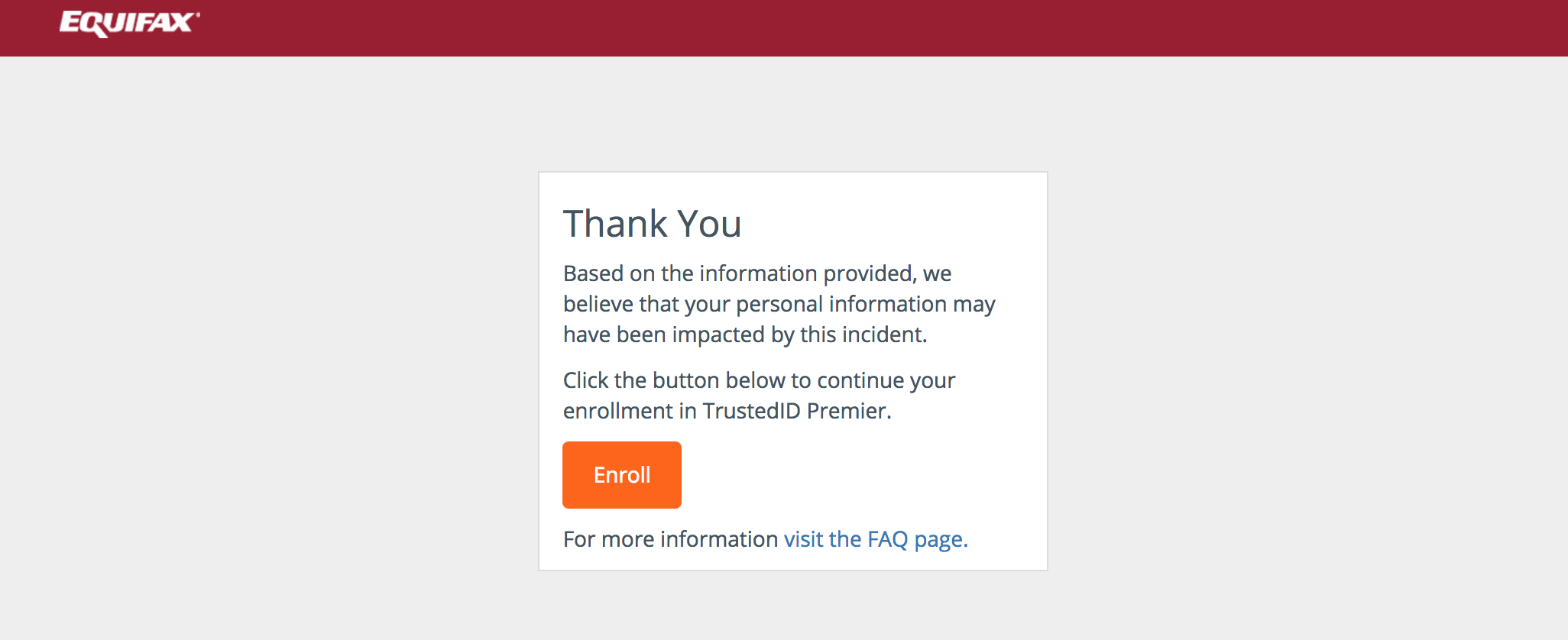

Equifax CEO Apologizes For Company’s Incompetence, Promises Vague (Possibly Pointless) Credit ‘Lock’ Service In 2018

By 9.28.17

The interim CEO for credit bureau Equifax is finally issuing a full-throated mea culpa for the massive data breach that compromised sensitive personal and financial information for about half of the adult U.S. population. In addition to extending the deadline for hack victims to freeze their credit free of charge or sign up for the company’s not terribly enticing anti-ID theft program, Equifax is also promising to offer something new: A way to “lock” your credit file (sort of, maybe, and only partially) for free (possibly). [More]

Equifax CEO Resigns Following Massive Data Breach

By 9.26.17

Among the items on that list of “Things a CEO Doesn’t Want on Their Resumé” is “Being the one in charge at the time of one of the biggest data breaches in U.S. history.” So perhaps it’s not a shock that Equifax CEO Richard Smith is stepping down only weeks after admitting that his credit bureau failed to secure the personal information of about half the U.S. adult population. [More]

Is Experian Letting Anyone Access Your Credit Freeze PIN?

By 9.21.17 — Updated: 9.22.17

UPDATE: Experian tells Consumerist that its authentication processes go farther than previously identified steps. The company regularly reviews its security practices and adjusts as needed.

Placing a credit freeze on your accounts following a hack or issue with identity theft is only effective if the credit reporting agency you’re working with doesn’t give ne’er-do-wells the ability to unfreeze the accounts by providing the same information that any good ID thief already knows about you. This is a lesson some victims of Equifax’s recent data breach are learning after freezing their accounts with fellow credit reporting agency Experian. [More]

Don’t Be Fooled By Fake Equifax Data Breach Information Sites

By 9.20.17

The Equifax breach, as we now all know, is completely terrible: Roughly 143 million customers in the U.S. had their personal data compromised. Concerned consumers are, naturally, looking for information — but fake sites or scams are everywhere. [More]

In Wake Of Equifax Hack, New York Wants Assurances From Experian, TransUnion

By 9.19.17

The Equifax data breach compromised personal information for some 143 million Americans, but there are still two other major credit bureaus — Experian and TransUnion — whose digital vaults are filled with the same sensitive info. New York’s top prosecutor is now asking these companies to explain how they won’t be the next source of a massive consumer data leak. [More]

Two Equifax Execs Exit Company Following Massive Data Breach

By 9.18.17

The full extent of Equifax’s recently revealed, massive data breach isn’t known yet — although 143 million US customers and tens of millions of others globally are thought to be affected — but top executives are already having to answer for the debacle, with two Equifax officers making a sudden exit. [More]

States Call On Equifax To Halt Marketing Of Its Paid Credit Monitoring Service

By 9.15.17

If you’re one of the 140 million or so people affected by Equifax’s failure to keep its data secure, the credit bureau is offering free access to its TrustedID credit monitoring service (though we don’t recommend you enroll in it). At the same time, the company is continuing to charge everyone else for access to TrustedID, and some consumers affected by the breach are inadvertently paying for a service they can get for free. That’s why dozens of state attorneys general are asking Equifax to stop trying to sell TrustedID for the time-being. [More]

Let’s Not Forget That Equifax Hackers Also Stole 200K Credit Card Numbers

By 9.14.17

We’re constantly learning new things about the massive Equifax data breach, including its actual cause, that it affected people all over the world, and that the Federal Trade Commission is investigating. Let’s back up, though, and remember something important: Along with the millions of Social Security and driver’s license numbers, 200,000 customer credit card numbers were taken too. [More]

If Someone Calls You From Equifax To Verify Your Account, It’s A Scam

By 9.14.17

Now that Equifax is part of the mass public consciousness for failing to secure sensitive financial and personal information for about half of the adult U.S. population, soulless scammers are trying to prey on this heightened awareness by blasting out fake calls to people, asking them to verify their account information. [More]