Use Snowball Method Spreadsheet To Pay Off Debts

Do you have so many credit cards that you could sew a pair of pants from them? Confused as how to get rid of them? Try this handy Excel spreadsheet to generate a custom strategy for becoming debt-free.

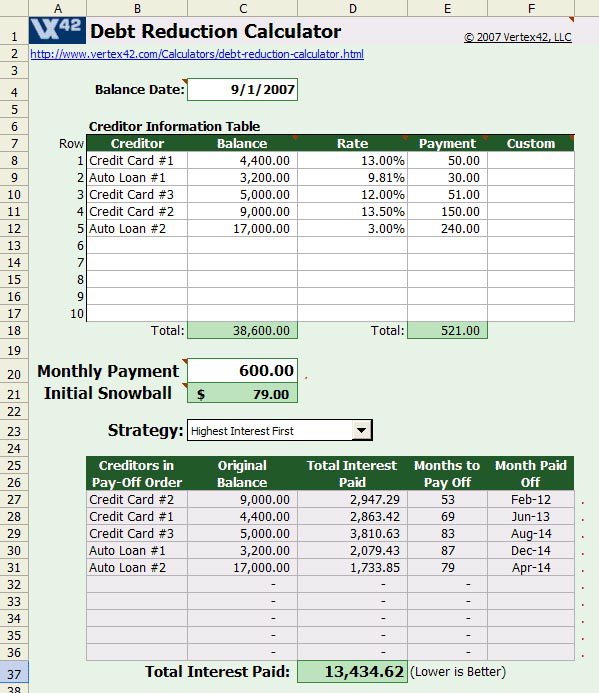

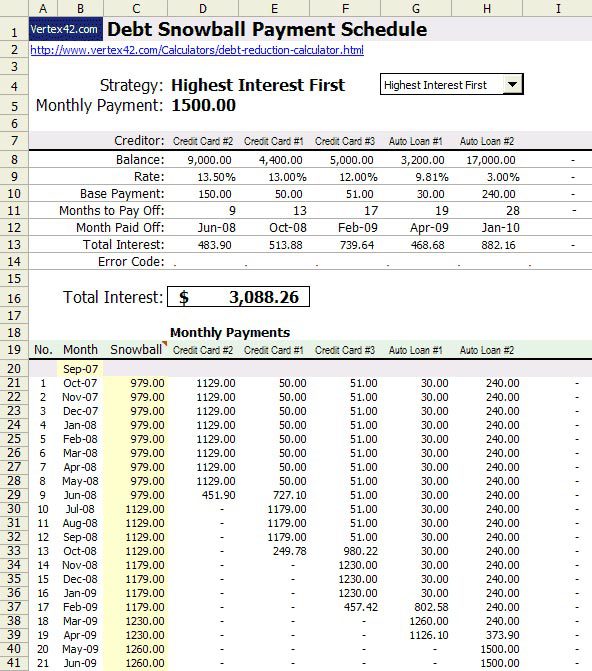

Just enter your credit cards, their balance, and interest rate. Then enter your required minimum monthly payments and the maximum possible amount you could put towards it, based on your budget. Select which style of repayment you want, such as snowball or highest interest first. The program then spits out an effective payoff strategy. It calculates how much interest and the total you’ll end up paying, and how long it will take to escape the shackles of debt.

If you’re carrying multiple balances, this is a great tool for getting started on, or optimizing, your personal debt payment plan.

Debt Reduction Snowball Calculator [vertex42] (Thanks to Matt!)

SCREENSHOTS:

Want more consumer news? Visit our parent organization, Consumer Reports, for the latest on scams, recalls, and other consumer issues.